1. Background

In terms of section 68 of the Central Goods and Services Tax Act, 2017 (hereinafter referred as CGST Act) read with rule 138 of the Central Goods and Service Tax (CGST) Rules 2017 (here in after referred as CGST Rule), E-Way Bill is a document to be carried by the person in charge of conveyance along with the goods and need to be generated electronically from the E-Way Bill Portal. The objective is quick and easy movement of goods across India without any hindrance.

2. Effective date of applicability of e-Way Bill

|

Effective date |

|

Inter-state movement of Goods |

|

|

For all the States and Union territories |

1st April, 2018 |

|

Intra-State movement of goods |

|

|

For Andhra Pradesh, Gujarat, Kerala, Telangana and Uttar Pradesh |

15th April, 2018 |

|

For Bihar, Haryana, Himachal Pradesh, Jharkhand, Tripura and Uttarakhand |

20th April, 2018 |

|

For Arunachal Pradesh, Madhya Pradesh, Meghalaya, Pondicherry and Sikkim |

25th April, 2018 |

|

For Nagaland |

1st May, 2018 |

|

For Rajasthan |

20th May, 2018 |

|

For Maharashtra, Andaman & Nicobar, Chandigarh, Dadra & Nagar Haveli, Daman & Diu, Lakshadweep and Manipur |

25th May, 2018 |

|

For Chhattisgarh, Goa, Jammu & Kashmir, Odisha, Punjab and Mizoram |

1st June, 2018 |

|

For Delhi |

16th June, 2018 |

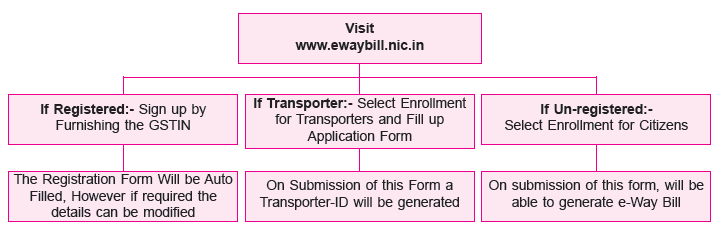

3. Registration on the e-Way Bill system

3.1. The registration mechanism for the GST taxpayers for the e-Way Bill system is a simple process. The GST registered person can register on the e-Way Bill portal by visiting at www.ewaybill.nic.in and create his user credentials to use the system. GST registered person can be a supplier, recipient, transporter, e-commerce operator or courier agency. In case the transporter is small operator and not registered under the GST, then this system provides the mechanism to enroll and create his user credentials to operate on this system.

Note: if the Registered person transports the good in his own/hired vehicle, such person need not be registered as a transporter.

4. Various way to generate e-Way Bill

- Using web base system

- Using SMS base facility

- Using Android App

- Bulk generation facility

- Using site-to-site integration facility

- Using Goods and Service Tax suvidha provider

5. When should e-Way Bill be issued? [Rule 138(1)]

5.1. Registered person who causes movement of goods of consignment value exceeding ₹ fifty thousand shall generate e-Way Bill—

- In relation to a supply (Sale, Transfer, supply to distinct person, Related person, Principal to agent or vice versa, etc.); or

- For reasons other than supply (for demo, repairing, job work, one branch to another branch within the State, etc.); or

- Due to inward supply from an unregistered person,

e-Way bill shall be generated through Form EWB-01. This form has two parts as “PART A” this contains information w.r.t. goods in movement and “Part B” which contains details of Vehicle and/or Transporter. E-Way Bill will be generated only after filling Part A and Part B both. Its needs to be generated before commencement of such movement and a unique number will be generated on the said portal.

5.2. For following specified Goods, the e-Way Bill needs to be generated mandatorily even if the value of the consignment of Goods is less than ₹ 50,000: Proviso to [Rule138(1)]

- Where goods are sent for job workby a principal located in one State or Union territory to a job worker located in any other State or Union territory.

- Where handicraft goodsare transported from one State or Union territory to another State or Union territory by a person who has been exempted from the requirement of obtaining registration.

Value: To check the applicability of the e-Way Bill, consignment value is to be determined as per Section 15 of CGST Act and includes GST applicable. It means It is the value of the goods declared in invoice, a bill of challan or a delivery challan, as the case may be, issued in respect of the said consignment and also include Central tax, State or Union territory tax, Integrated tax and Cess charged, if any. But, it will not include value of exempt supply of goods, where the invoice is issued in respect of both exempt and taxable supply. It will also not include value of freight charges for the movement charged by transporter.

6. Who is liable to issue e-Way bill [Rule 138 (1), (2), (2A), (3)]

6.1. In the light of the Rule 138 (1), (2), (2A) and (3) here, we are providing the following table including all the possible cases

|

Transaction |

Recipient |

Supplier |

Transportation mode |

Transporter |

EWB-01

Part A |

EWB-01

Part B |

|

Intra / Inter State |

Registered/ |

Registered |

By Road, through a Transporter |

Registered |

Registered Person who is causing movement |

See note 1 below* |

|

Intra / Inter State |

Registered /unregistered |

Registered |

By Road, through a Transporter |

Unregistered |

As Above |

See note 1 below* |

|

Intra / Inter State |

Registered/ |

Registered |

By Hired or Owned Vehicle or through Public Conveyance |

— |

Registered Person – who hired or owned vehicle for transportation

Or

– who is making movement of goods

|

Same as Part A |

|

Intra / Inter State |

Registered / unregistered |

Registered |

By Air/Train/ Vessel |

— |

Registered Person who is making movement |

Same as Part A |

|

Intra State |

Registered |

Unregis-tered |

By Road, through a Transporter |

Registered |

Registered Recipient |

See Note 1 Below* |

|

Intra State |

Registered |

Unregistered |

By Road, through a Transporter |

Unregistered |

As Above |

As Above |

|

Intra State |

Registered |

Unregistered |

By Hired/ Owned Vehicle / Public Conveyance |

— |

Registered Recipient |

Registered Recipient |

|

Intra State |

Registered |

Unregistered |

By Air/Train/Vessel |

— |

Registered Recipient |

Registered Recipient |

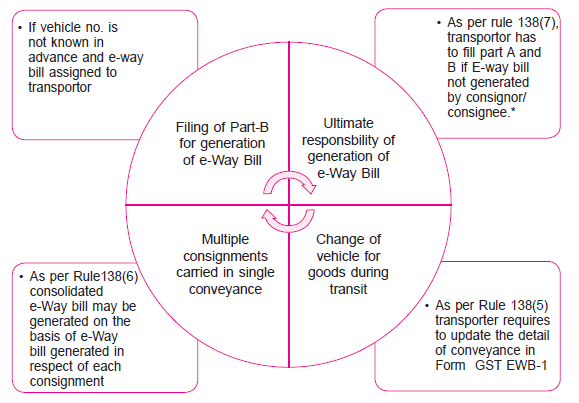

*Note 1: Filling of Part B is important as without Part B filling EWB no. cannot be generated. First responsibility to fill Part B also lies with the person who has filled Part A. However as provided in sub-rule 3, if person filling Part A has not provided with details of vehicle which will finally carry the consignment, he can mention the GSTIN of Registered Transporter or Transporter ID of Unregistered Transporter. In that case transporter has to provide details of vehicle in Part B and finally has to generate EWB no.

6.2. Important points to be noted

- However Rule 138(1)(2)(3) cast first liability of e-Way Bill on registered person who causes movement (as explained above in table), it may be noted that in case both registered party (supplier and recipient), practically

e-Way bill can be generated by any one of them.

- If the goods to be transported are supplied through an e-commerce operatoror a courier agency, then on authorization received from consignor such person may also furnished the information in Part A of FORM GST EWB-01.

- Sub-rule 2A creates specific liability of registered person to generate e-Way Bill in case goods are transported by railways or by air or vessel. In case of railways or by air or vessel, detail in Part B of e-Way Bill can be furnished after the movements of goods begin. In case of railway, e-Way Bill required to be furnished at the time of delivery of goods.

- First Proviso of Rule 138(3) provides an option to Registered Person or the Transporter to generate the e-Way Bill even if value of consignment is

< ₹ 50,000.

- Third Proviso of Rule 138(3) and (5) provides relaxation for not to furnish details of conveyance in Part B of form GST EWB-01, if the goods are transported for a distance of up to fifty kilometerswithin the State or Union territory from the place of business of the consignor to the place of business of the transporter for further transportation or from place of business of the transporter to the place of business of consignee.

- No e-Way bill is required for movement of goods up to a distance of 20 Km. from the place of business of consignor to a weighbridge for weighment or from the weighbridge back to the place of business of consignor, within the same State, subject to the condition that the movement of goods is accompanied by a delivery challan issued.

7. Role of Transporter in E Way Bill

* As per Rule 138(7) Where consignor or consignee has not generated e-Way bill and the value of consignment carried in a conveyance exceed ₹ 50,000/-, the transporter in respect of inter-State supply has to require to generate e-Way bill. However provision of this rule will be notified from later date. Therefore, at present there is no requirement to generate e-Way Bill where an individual consignment value is less than ₹ 50,000/-, even if the transporter is carrying goods of more than ₹ 50,000/- in a single conveyance.

7.1. Change of transporter before or during the movement of goods: [Rule 138(5A)] Often a transporter needs to be changed at last moment or amongst the transporters assignment of load to another transporter (or subcontracting) is very common. This sub-rule can be analysed in two parts –

Before updation of vehicle details in Part B:

e-Way bill can be assigned to another transporter either by person who furnished Part A or Transporter.

After updation of vehicle details in Part B: This covers another practical situation, a transporter may require to be changed during transit. This can be done however only by transporter whom it was last assigned before updation of vehicle details in Part B.

7.2. E-Way Bill in case of transshipment / multi model transportation

The consignment of one e-Way Bill has to be moved in multiple vehicle after moving to transshipment place.

For example, an e-Way Bill is generated and needs to be moved from A to C. Here, the consignment moves from A to B via Rail or bigger vehicle. Now, it is not possible to move the consignment from B to C in

the same mode of transportation due to unavailability of that mode or may be due to hilly region where big vehicles cannot be used. In such cases, the consignment needs to be moved in multiple smaller vehicles.

Steps to be followed as follow:

- First generate the e-Way Bill with source and destination as per the document/invoice.

- Carry out the first leg of movement of the consignment up to the transshipment.

- Choose the ‘Change to Multi-vehicle’ option and update the e-Way Bill for multi-vehicle movement. Here, the total quantity of the consignment and movement from and to place for the multiple vehicles requirement has to be entered.

- Now, when the consignment has been loaded to the smaller vehicle, update the ‘Part-B’ of the e-Way Bill with the vehicle number, along with the quantity loaded, and move the consignment.

- Step No. 4 may be repeated till total quantity is loaded and moved. The system will not allow the quantity to be shipped in multiple vehicles more than what has been declared while marking the e-Way bill for multi-vehicle.

8. Validity period of e-Way Bill [Rule-138(10)]

|

Time Allowed |

Normal Cargo |

Over the Dimensional Cargo* |

|

1 day |

Up to 100 Km. |

Up to 20 Km. |

|

1 additional day |

For every 100 Km. or part thereof thereafter |

For every 20 km. or part thereof thereafter |

Note:

★ Over Dimensional Cargo means a cargo carried as a single indivisible unit and which exceeds the dimensional limits prescribed in Rule 93 of the Central Motor Vehicle Rules 1989 made under the Motor Vehicles Act, 1988.

- Period of validity shall be counted from the date at which the e-Way bill has been generated and each day shall be counted as the period expiring at midnight of the day immediately following the date of generation of e-Way bill. e.g.

e-Way bill generated on June 1, 2018 for a distance of 520 Km, so first 100 Km = 1 day and for another 400 Km = 4 days (1 day each for every additional 100 Km) and for balance 20 Km = 1 day (100 Km or part thereof). Total validity period is 6 days. Now 1st day will be counted till the midnight of 2nd June. Therefore 6 days validity will end on June 07, 2018.

- In case of circumstances of an exceptional nature including transshipment, the goods cannot be transported within the validity period of the e-Way Bill, the transporter may extend validity periodof e-Way Bill after updating the details in Part B of FORM GST EWB-01.

8.1. Cancellation of e-Way Bill [Rule 138(9)]: Where an e-Way Bill has been generated, but:

- Goods are either not transported at all or

- Are not transported as per the details furnished in the e-Way Bill

E-Way Bill may be cancelled within 24 hours of generation of the e-Way bill. However an E-way bill cannot be cancelled if it has been verified in transit in accordance with the provisions of Rule 138B.

8.2. Acceptance or Rejection of e-Way Bill [Rule 138(11), (12)]: Sub-rule 11 provide that the details of e-Way Bill generated shall be made available to the

- Supplier, if registered, where the information in Part A of FORM GST EWB-01 has been furnished by the recipient or the transporter; or

- recipient, if registered, where the information in Part A of FORM GST EWB-01 has been furnished by the supplier or the transporter,

Either of the party to whom information is made available as per above sub-rule has to communicate his acceptance or rejection within 72 hours of:

- Details being made available to him on the common portal, or

- The time of delivery of goods

whichever is earlier.

If such acceptance or rejection has not been communicated within the above specified period, it shall be deemed that he has accepted the said details.

9. No e-Way bill required to be generated [Rule 138(14)]

|

a. |

Where the goods being transported are specified in Annexure (Refer Note 2); |

|

b. |

Where the goods are being transported by a non-motorised conveyance; |

|

c. |

Where the goods are being transported from the customs port, airport, air cargo complex and land customs station to an inland container depot or a container freight station for clearance by Customs; |

|

d. |

In respect of movement of goods within such areas as are notified under clause (d) of sub-rule (14) of rule 138 of the State or Union territory Goods and Services Tax Rules in that particular State or Union territory; |

|

e. |

Where the goods, other than de-oiled cake, being transported, are specified in the Schedule appended to notification No. 2/2017- Central tax (Rate) dated the 28th June, 2017. |

|

f. |

Where the goods being transported are alcoholic liquor for human consumption, petroleum crude, high speed diesel, motor spirit (commonly known as petrol), natural gas or aviation turbine fuel; |

|

g. |

Where the supply of goods being transported is treated as no supply under Schedule III of the Act; |

|

h. |

Where the goods are being transported— (i) Under customs bond from an inland container depot or a container freight station to a customs port, airport, air cargo complex and land customs station, or from one customs station or customs port to another customs station or customs port, or (ii) under customs supervision or under customs seal;

|

|

i. |

Where the goods being transported are transit cargo from or to Nepal or Bhutan; |

|

j. |

Where the goods being transported are exempt from tax . |

|

k. |

Any movement of goods caused by defence formation under Ministry of Defence as a consignor or consignee; |

|

l. |

Where the consignor of goods is the Central Government, Government of any State or a local authority for transport of goods by rail; |

|

m. |

Where empty cargo containers are being transported; and |

|

n. |

Where the goods are being transported upto a distance of twenty kilometers from the place of the business of the consignor to a weighbridge for weighment or from the weighbridge back to the place of the business of the said consignor subject to the condition that the movement of goods is accompanied by a delivery challan. |

|

o. |

Where empty cylinders for packing of liquefied petroleum gas are being moved for reasons other than supply. (Inserted by N/No.26/2018- Central Tax, effective from 13th June, 2018) |

9.1. E-way bill is not required to be generated for the intra-State movement of goods in the State of Maharashtra on or after the 1st July 2018, when the movement of the goods commences and terminates within the area and for the purpose stated as below

|

Goods |

Condition |

Hank, Yarn, Fabric and Garments

(Irrespective of Consignment Value) |

Where the goods mentioned in corresponding column are transported for a distance of up to 50 Km. within the State of Maharashtra for the purpose of job work only. |

|

Other goods, if the Consignment value does not exceeding ₹ 1 Lakh |

Where the movement commences and terminates within the State of Maharashtra. |

9.2. NOTE 2: ANNEXURE [(See Rule 138(14)]

|

S. No. |

Description of Goods |

|

1. |

Liquefied petroleum gas for supply to household and non-domestic exempted category (NDEC) customers |

|

2. |

Kerosene oil sold under PDS |

|

3. |

Postal baggage transported by Department of Posts |

|

4. |

Natural or cultured pearls and precious or semi-precious stones; precious metals and metals clad with precious metal |

|

5. |

Jewellery, goldsmiths‘ and silversmiths‘ wares and other articles |

|

6. |

Currency |

|

7. |

Used personal and household effects |

|

8. |

Coral, unworked (0508) and worked coral (9601) |

10. Mandatory to carry the following document by person–in-charge of conveyance [Rule 138A] read with Rule 55A of CGST Rules.

10.1. The person in charge of conveyance shall carry:

- The invoice, bill of supply or delivery challan, as the case may be; and

- Copy of e-Way Bill or the e-Way number, either physically or mapped to a Radio Frequency Identification Device (RFID).

10.2. Concept of invoice reference number

‘’A registered person may obtain an invoice Reference Number from the common portal by uploading, on the said portal, a tax invoice issued by him in FORM GST INV-1 and produce the same for verification by the proper officer in lieu of the tax invoice and such number shall be valid for a period of thirty days from the date of uploading.”

This is an additional option given to registered person in case of taxable supply where a Tax invoice is issued. Using this option an IRN can be generated by filing form GST INV-1 on portal. However after generating, IRN will be valid for 30 days.

This will facilitate in two ways:

- Information for e-Way Bill generation under Part A of Form EWB-01 shall be auto populated.

- No need to carry physical copy of Tax invoice during transit only IRN will be sufficient.

11. Verification and inspections

11.1. Verification of documents and conveyances [Rule 138B]

- Can be carried out by Commissioner or an officer as appointed by him on this behalf to intercept any conveyance to verify e-Way Bill.

- RFID readers shall be installed at the place of verification. Verification of vehicles shall be done through this device reader where e-Way Bill has been mapped with the said device.

- The physical verification of conveyances shall be carried out by the proper officer as authorised in this behalf.

11.2. Inspection and verification of goods [Rule 138C]

- A summary report of every inspection of goods in transit shall be recorded online by the proper officer in Part A of FORM GST EWB– 03 within twenty four hours of inspectionand the final report in Part B of FORM GST EWB - 03 shall be recorded within three daysof the inspection. Provided that such period of three day may be extended for a further period not exceeding three days on sufficient cause being shown.

Note:

- Physical Verification done during transit at one place in the State or in any other State, no further physical verification can be carried out in the State unless in case where evasion of tax is suspected.

- Where the goods are intercepted or detained for a period exceeding 30 minutes, the transporter may upload information in FORM GST EWB- 04. As the online facility to upload Form GST EWB-04 yet to be activated, same can be filed manually also.

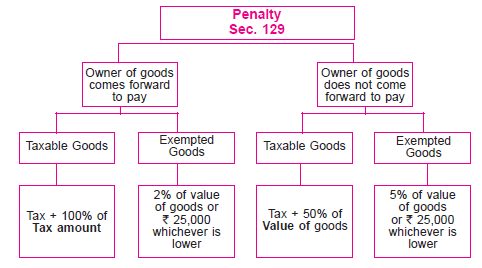

12. Offence and penalty

12.1. Below penal provisions may get attracted for not complying with e-Way Bill rules:

- Section 122(1) : Where a taxable person who-

issues any invoice or bill without supply of goods or services or both in violation of the provisions of this Act or the rules made thereunder;

Transports any taxable goods without the cover of documents as may be specified in this behalf

He shall be liable to pay a penalty of ten thousand rupees or an amount equivalent to the tax evaded, whichever is higher.

- Section 129(1): Where any goods transported or stored in the contravention of provision of this Act and Rule then such goods and conveyance, and documents relating to such goods and conveyance liable to detention and seizure. And shall be released on payment of taxes and penalties as follow:-

13. Miscellaneous

13.1. What has to be done by the transporter if consignee refuses to take goods or rejects the goods for any reason?

There is a chance that consignee or recipient may reject to take the delivery consignment due to various reasons. Under such circumstances, the transporter can get one more e-Way Bill generated with the help of supplier or recipient by indicating supply as ‘Sales Return’ with relevant documents, return the goods to the supplier as per his agreement with him.

13.2. How to handle “Bill to” - “Ship to” invoice in e-Way Bill system?

Sometimes, the taxpayer raises the bill to somebody and sends the consignment to somebody else as per the business requirements. There is a provision in the e-Way Bill system to handle this situation, called as ‘Bill to’ and ‘Ship to’.

In the e-Way Bill form, there are two portions under ‘TO’ section. In the left hand side - ‘Billing To’ GSTIN and trade name is entered and an the right hand side - ‘Ship to’ address of the destination of the movement is entered. The other details are entered as per the invoice. In case Ship to State is different from Bill to State, the tax components are entered as per the billing State party. That is, if the Bill to location is inter-State for the supplier, IGST is entered and if the Bill to Party location is intra-State for the supplier, the SGST and CGST are entered irrespective of movement of goods whether movement happened within State or outside the State.

13.3. How to handle “Bill from” - “Dispatch from” invoice in e-Way Bill system?

Sometimes, the supplier prepares the bill from his business premises to consignee, but moves the consignment from some others’ premises to the consignee as per the business requirements. This is known as ‘Billing From’ and ‘Dispatching From’. e-Way Bill system has provision for this. In the e-way bill form, there are two portions under ‘FROM’ section. In the left hand side - ‘Bill From’ supplier’s GSTIN and trade name are entered and in the right hand side -‘Dispatch From’, address of the dispatching place is entered. The other details are entered as per the invoice. In case Bill FROM location State is different from the State of Dispatch the Tax components are entered as per the State (Bill From). That is, if the billing party is inter-State for the supplier, IGST is entered and if the billing party is intra-State for the supplier, the SGST and CGST are entered irrespective of movement of goods whether movement happened within State or outside the State.

13.4. How to generate e-Way Bill, if the goods of one invoice is being moved in multiple vehicles simultaneously?

Where the goods are being transported in a semi knocked down (SKD) or completely knocked down (CKD) condition, the EWB shall be generated as follows:

- Supplier shall issue the complete invoice before dispatch of the first consignment;

- Supplier shall issue a delivery challan for each of the subsequent consignments, giving reference of the invoice;

- Each consignment shall be accompanied by copies of the corresponding delivery challan along with a duly certified copy of the invoice; and

- Original copy of the invoice shall be sent along with the last consignment.

13.5. Is e-Way Bill required for movement of used personal and household effects valuing more than ₹ 50,000?

Rule 138(14) lists goods and circumstances of movement, in respect of which requirement to generate e-Way Bill is excluded. As used personal and household effects are specifically covered by Annexure to Rule 138(14). Therefore, no e-Way Bill is required.

13.6. Is HSN Code required to be furnished in EWB-01 PART-01? If turnover was below 1.5 Crore in preceding year still is it required to be mentioned?

According to the Notification No. 03/2018, it states that any taxpayer having turnover in preceding financial year up to ₹ 5 crores is required to mention 2 digits of HSN Code and for taxpayer with turnover in Preceding Financial year exceeding ₹ 5 crore is required to mention 4 digits.

In this notification, they have not given any relaxation to the taxpayers with turnover up to ₹ 1.5 crore which was given in monthly returns and invoice rules.

Therefore HSN code is required to be furnished in EWB-01 PART-01.

13.7. How to calculate distance if goods are sent for export or received in case of import?

- In case of export-From the premises of consignor where the goods are loaded for movement, to the customs port or airport or customs bonded warehouse, where the goods are kept or export clearance.

- In case of import: From the customs port or airport or customs bonded warehouse as the case may be, to the premises of consignee.

13.8. How to register on e-Way Bill portal if transporter is registered in multiple State or Union territory on GST portal?

As per Rule 58(1A) of CGST Rule, 2017 for the purpose of e-Way bill, a transporter registered in multiple States or union territory having the same PAN number, may apply for a unique common enrolment number by submitting the details in FORM GST ENR-02 using any one of his GSTIN numbers. Where the said transporter has obtained a unique common number, he shall not be eligible to use any of GSTIN numbers for the purpose of said e-Way Bill Rules.

Back to Top

|