GSTPAM News Bulletin October 2024

CIRCULAR FOR RENEWAL OF MEMBERSHIP/SUBSCRIPTION CHARGES FOR THE F.Y. 2024-25

Dear Members,

RENEWAL OF MEMBERSHIP FOR F.Y. 2024-25

The Membership Fees for the year 2024-25 are due for renewal on 01.04.2024. We appreciate your Continuing support and participation in the activities of our Association.

The timely Renewal of Membership will enable themembers to continuously receive the updates on various activities of GSTPAM along with the GSTReview, News Bulletin, Circulars, Messages, Webinars and online access to the website www.gstpam.org. The Life Members only need to renew the subscription charges for the GST Review. The members can also avail the benefit of discount by paying advance for subsequent two years membership fees /subscriptioncharges.

The Membership Renewal Fees received after 30th April, 2024 will be subject to approval of the Managing Committee. If the Renewal fees for a particular year are not paid, then the member is liable to pay Admission Fees again for Renewal in the subsequent year.

Delayed Renewal Members will be provided Pre Renewal GST Review subject to availability upon payment of such additional courier charges.

The details of Membership/Subscription Fees are given below for your ready reference

|

Type of Membership |

Membership Fees incl. GST |

Admission Fees Incl.GST |

Subscription Charges for GST Review |

Total |

|

New Membership Application |

||||

|

Donor Member |

24,780.00 |

– |

600.00 |

25,380.00 |

|

Patron Member |

17,700.00 |

– |

600.00 |

18,300.00 |

|

Life Member |

11,800.00 |

944.00 |

600.00 |

13,344.00 |

|

Life Member (Conversion from Ordinary) |

11,800.00 |

590.00 |

600.00 |

12,990.00 |

|

Ordinary Local Member |

1,770.00 |

590.00 |

– |

2,365.00 |

|

Ordinary Outstation Member |

1,475.00 |

590.00 |

– |

2,065.00 |

|

Student Member |

590.00 |

590.00 |

– |

1,180.00 |

New Membership Application (Firm/LLP)

|

Ordinary Local Member |

1,770.00 |

944.00 |

0 |

2,174.00 |

|

Ordinary Outstation Member |

1,475.00 |

944.00 |

0 |

2,419.00 |

|

Patron Member |

17,700.00 |

0 |

600.00 |

18,300.00 |

|

Donor Member |

24,780.00 |

0 |

600.00 |

25,380.00 |

Advance Membership/ Subscription charges for subsequent two years 2025-26& 2026-27 (Non-Refundable)

|

Ordinary Local Member |

3,186.00 |

– | – |

3,186.00 |

|

Ordinary Outstation Member |

2,665.00 |

– | – |

2,665.00 |

|

Life Member (Individual/Firm/LLP) |

0 |

– |

1200.00 |

1,200.00 |

|

Patron Member |

0 |

– |

1200.00 |

1,200.00 |

|

Donor Member |

0 |

– |

1200.00 |

1,200.00 |

Subscription for GST Review for F.Y. 2024-25 by Non-Members

|

Subscription fees for GSTR |

– | – |

1000.00 |

1,000.00 |

Advance Membership / Subscription charges for subsequent two years 2025-26& 2026-27 (Non-Refundable)

|

Subscription Fees -GSTR |

0 |

– |

2000.00 2,000.00 |

Modes of Payment:-

|

Cheque |

A/c Payee Cheque drawn in favor of “The Goods & Services Tax Practitioners’ Association of Maharashtra” payable at Mumbai. |

|

NEFT Details |

The Goods & Services Tax Practitioners’ Association of Maharashtra Bank of India, Mazgaon Branch Current Account No. 007020100001816, IFSC Code – BKID0000070.Online generated transaction Acknowledgement should be sent by email on [email protected] along with membership and payment details Members are requested to send their physical form to the association for Approval, Issuance and Office record. |

|

Cash |

Renewal form along with requisite amount will be accepted between 10.30 a.m. and 5.30 p.m. on all working days except Saturday at our Office at Mazgaon Library – Mazgoan: 1stFloor, 104, GST Bhavan, Mazgaon, Mumbai – 400 010 Or Bandra Library – GST Bhavan, Ground Floor, A Wing, Bandra Kurla Complex, Bandra (East), Mumbai – 400 051. Or Mazgaon Tower- 8 & 9, Mazgaon Tower, 21, Mhatar Pakhadi Road, Mazgaon, Mumbai – 400 010. |

|

Identity (New Members) |

New Members should provide the following as Identity Proof : PAN, Aadhar Card, Constitution Document. Address Proof(any one) : Electricity Bill / Passport/ Aadhar Card / Driving License/ Voter id/ Ration Card along with Membership Form |

|

Identity Card (For Renewals) |

Ordinary Local/Outstation Members should provide Two Photographs along with the Renewal Form for issue of I- cards. |

|

Online Payment Link |

Members can make online payment on our website www.gstpam.org. Members are requested to download Members Renewal form from website.Update the latest details in the form, scan it and mail at email [email protected] Payment Link : https://www.gstpam.org/online/renew-membership.php If you are login first time? Click here for create your password |

We value your continuation of the membership and look forward to your renewal to this effect.

Dated:- 19.07.2024

Jatin Chheda

Rahul Thakar

Hon. Jt.Secretary

Guidance Cell Email ID for queriesMembers can send their queries at [email protected] |

ORDER FORM FOR GSTPAM REFERENCER 2024-25

(Members are requested to take out the photocopy of the Order Form for booking)

To

The Convenor,

GSTPAM Referencer Committee

The Goods & Services Tax Practitioners’ Association of Maharashtra

Room No. 8 & 9, Mazgaon Tower, Mhatar Pakhadi Road,

Mazgaon, Mumbai – 400 010

Dear Sir,

Please book my/our order of GSTPAM Referencer for the year 2024-25 as given below.

|

Sr. |

Particulars |

Price per copy if booked prior to 15th July 2024 |

Price per copy if booked after to 15th July 2024 |

Qty |

Total RS. |

|

1 |

GSTPAM Referencer 2024-25 Part I & II (GST, VAT & Allied Law Referencer & Updated GST Rate schedules). |

700 |

750 |

||

|

2 |

Courier Charges (For Outstation members only) (per set) |

130 |

130 |

||

|

3 |

Courier Charges (For Local members only) (per set) |

100 |

100 |

Note:

-

Referencer will be published in Part I & II (for GST, VAT & Allied Laws Referencer & Updated GST rate schedules).

-

Applicants requiring more than 5 copies of the Referencer are required to give a request on their letter head along with the order form. Tax Practitioner’s Associations can place order in bulk quantity by making request on their letterhead signed by the Association’s President and Secretary.

-

Applicants will be issued receipt at the time of placing of their order. Applicants are requested to bring receipt at the time of taking the delivery of the Referencer. No delivery of the Referencer shall be given, unless the receipt for payment is submitted at the counter. If the receipt for payment is lost, than no delivery of the Referencer shall be given.

The payment for the above order of………………………………………………………………………… (Rupees in words) is made herewith by Cash /Card /Cheque /Demand Draft No. ……………dated ……………………………drawn on……………………………………………… Bank…………………………… Branch, Mumbai.

Signature …………………………….

Membership Number………………………………………… Address.………………………………………………………

Name ……………………………………… ………………………………………………………………………………

……………………………………………… ………………………………………………………………………………

Office Tel No………………………………………… Residence Tel No……………………………………………………………

E-mail: …………………………………………………… Mobile No.………………………………………………………………

PROVISIONAL RECEIPT

Received with thanks payment of. ………………… from…………………………… vide Cash /Card /Cheque /NEFT/Demand Draft No. …………………………. Date…………………………… drawn on………………………………………………… Bank …………………………………… Branch, Mumbai.

Signature ……………………………

Date…………………………………. Name of staff of GSTPAM……………………

Note:

-

Please fill in all the details in the above form and send the same to the GSTPAM’s office at Tower or at Mazgaon library along with requisite payment.

-

For Direct Deposit / NEFT payment – Bank of India, Mazgaon – Account No. 007020100001817, IFSC Code – BKID0000070. Acknowledgement of the same should be sent by email: [email protected] along with duly filled form.

-

Online Payment Link : https://www.gstpam.org/online/purchase-publication.php

-

Please mention your name and membership number on the reverse side of the Cheque / Demand Draft.

-

The counter timings are from 10.30 a.m. to 5.30 p.m. on Monday to Friday.

-

The Cheque / DD should be drawn in the name of “THE GOODS AND SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

|

Topics |

|

CHAPTER – I |

|

• Basic Concepts of GST |

|

• Time and Value of Supply of Goods and Services |

|

• Input Tax Credits |

|

• Determination of Nature of Supply |

|

• Registration under GST |

|

• Returns |

|

• Payment of Taxes, Interest ,Penalties & Other levies |

|

• Refunds |

|

CHAPTER – II |

|

• Demand & Recovery |

|

• Assessements and Audit Under GST |

|

• Liability to pay in Certain Cases |

|

• Inspections, Search, Seziure and Arrest |

|

• Advance Ruling Provisions |

|

• Appeals Provisions |

|

• Offences and Penalties |

|

• E-way Bill |

|

• E-Invoice |

|

• AAR Referncer 23-24 |

|

• Input Service Distributor & Cross-Charge |

|

• TDS/TCS Provisions |

|

• GST Composition Scheme |

|

• Reverse Charge Mechanism |

|

• Anti-Profiteering Provisions |

|

CHAPTER – III |

|

• GST Rates of Taxable Goods |

|

• GST Rates for Taxable Services |

|

• Index of Exempted Goods |

|

• Index of Notified Exempted Services |

|

• Index of Notified Goods under RCM |

|

• Index of Notified Services under RCM |

|

CHAPTER – IV |

|

• Gist of Important Judgments of the Tribunals, High Courts and Supreme Court |

|

• Central Sales Tax Act, 1956 |

|

• Maharashtra State Tax on Professions Trades, Callings & Employments Act, |

|

• The Maharashtra Stamp Act, 1958 |

|

• Maharashtra State Budget Highlights 2024-2025 |

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA INTENSIVE STUDY COURSE CIRCULAR FOR THE YEAR 2024-25

In the rapidly changing field of Goods & Services Tax (GST), where new updates, amendments, notifications and

circulars are a constant, staying informed is essential. The complexity of GST requires the tax professionals to

continually refresh and deepen our understanding to apply the law effectively.

Our association’s Intensive Study Circle is an esteemed platform designed to help members navigate these

challenges. Through in-depth discussions and interactive sessions, participants gain critical insights and practical

knowledge that are indispensable in today’s dynamic professional landscape.

We are excited to launch the 2024-25 session on Wednesday, September 4, 2024. We invite you to join this highly

anticipated event, where we will explore various facets of GST law, sharing expertise and practical solutions to real-

world issues.

The intensive study circle is designed for maximum interaction wherein, a participant member can opt for or an

expert speaker acts as a group leader and leads the discussion on the latest issues arising out of the assigned topic

and some of the top eminent faculty and senior in the profession acts as a monitor and guide through out the

st rd th duration of the session. The meetings will be generally arranged on 1 , 3 or 5 Friday of the month, during 04.30

p.m. to 7.00 p.m. on virtual mode. There are around 15 meetings in the Intensive Study Circle.

The inaugural meeting of the Intensive Study Circle shall be held on Wednesday, 04-09-2024 between 04.30 p.m. to

7.00 p.m. Virtual mode on the subject “ISD (Input Service Distribution) vs CC (Cross Charge). ISD Mechanism

made compulsory from 1 Apr 2025 under GST – Indepth Analysis “. The topic will be lead by Adv. Monarch Bhatt

under the Chairmanship of CA Vikram Mehta. Please note all other sessions will be carried out on virtual platform.

The Intensive Study Circle Meeting Fee is fixed at Rs. 1,650/- including GST for Members and 1850/- including

GST for Non members. You are requested to enroll at the earliest to avoid disappointment. Kindly use photocopy

of the Enrolment form printed here in below. Also write your email address and mobile number for better

communication.

Member interested to act as group leader should inform by filling up the option in the Form of “I wish to be a group

leader for the subject” and are requested to contact the Convenor/s on Cell No. 98211 21433

/9224386682/9821441740 /9892512345

Note :

-

GST lectures will be in form of group discussion, which will be helpful to study the new law.

-

If the materials are received 3 days earlier to the date of meeting, the same will be circulated through mails to the participants.

-

Participants are requested to discuss only the points related to the particular topic of the meeting and to come prepared for the subject, which will be helpful for the discussion.

ENROLMENT FORM FOR INTENSIVE STUDY CIRCLE MEETINGS FOR THE YEAR 2024- 25

To

The Convenor,

GSTPAM Referencer Committee

The Goods & Services Tax Practitioners’ Association of Maharashtra

Room No. 8 & 9, Mazgaon Tower, Mhatar Pakhadi Road,

Mazgaon, Mumbai – 400 010

Dear Sir,

Please book my/our order of GSTPAM Referencer for the year 2024-25 as given below.

To, Convener,

Intensive Study Course

The GSTPAM, Mazgaon, Mumbai – 400 010.

Dear Sir,

Please enroll me as a participant for the Intensive Study Course for the year 2023-24. The Registration fees of

Rs.1,650/-

(for members) / and

Rs.1,850/-

(for non-members) 18% Including GST is enclosed herewith by Cash /DD / Cheque No.

……………dated ……………………………drawn on………………………………………………

Particulars of Member/Participant :

Name:

Educational Qualification:

Address for Communication:

Telephone No. Office :

Res.

Email ID :

Mob. No,

GSTPAM Membership No:

GSTIN (if Applicable):

I also wish to be a group leader for the subject of and suitable available date will be :

I would like to attend the Meeting (Please Tick only one option)

The Physical mode will be continued only if majority participants opt for the Physical Mode Signature

Note :-

-

Please issue the Cheque in favour of ''The Goods & Services Tax Practitioners' Association of Maharashtra'' (FULL NAME IS REQUIRED TO BE STATED ON THE CHEQUE AS PER RBI DIRECTION).

-

For NEFT payment – Bank of India, Mazgaon- Account No. 007020100001816, IFSC – BKID0000070. Acknowledgement generated through online transaction should be emailed on [email protected] along with Enrolment Form and payment details.

-

Online Payment Link: https://www.gstpam.org/online/event-registration.php

-

Outstation members are requested to make payment online payment.

-

The enrollment form along with payment proof should be submitted at Room No. 104, Vikrikar Bhavan, Mazgaon, Mumbai – 400010.

-

Kindly carry the receipt of payment to attend the Lecture.

-

The Association reserves the right to change and alter the schedule if required.

Dear Members,

We are happy to announce that “2nd Batch of Beginners’ Certication Course on GSTi n

ગુજરાતી language”will commence on 18th of November 2024 in Virtual mode.

Details of Coaching Class are as under

Virtual : Zoom Platform

Enrollment Fee : Rs.1,240/- (Inclusive GST) for all participants

Salient Features of the Coaching Class

-

The object of the Coaching Class is to train and groom the new entrants or would be entrants in GST in Gujarati Language. Our well known seniors not only teach what is written in the books but also share the essence of their professional experience which they have gained over the years. This can be of enormous help and use to the new entrants. Here, students not only get knowledge but also wisdom by interacting with the seniors.

તમામ સ ો તમામ સંબંિધત િવષયોને આવરી લેતા ગુજરાતી ભાષામાં હશે. સ ો અનુભવી ેિ ટશનરો ારા હાથ ધરવામાં આવશે. અહીં, િવ ાથ ઓ િસિનયસ{ સાથે વાતચીત કરીને મા ાન જ નહીં પરંતુ સમજ પણ મેળવે છે.

-

Our expert and experienced faculties will cover all important aspects of the respective topics with guidance on legal and practical aspects.

અમારા િન ણાત અને અનુભવી િશ કો સંબંિધત િવષયોના તમામ મહ વપૂણ{ પાસાઓને કાયદાકીય અને યવહા પાસાઓ પર માગ{દશ{ન સાથે આવરી લેશે.

-

With more than 7 years of GST implementation, the classes will help the participants to solve their doubts and understand the nuances of the law.

GST અમલીકરણના 7 વષ{થી વધુ સમય સાથે, વગ સહભાગીઓને તેમની શંકાઓ દૂર કરવામાં અને કાયદાના સૂ મ ભેદ સમજવામાં મદદ કરશે.

-

The classes would be conducted, having “Twenty Five” Coaching Sessions of one and a half hour each. Also, the participants would be given case studies for the practical experience.

આયોિજત વગ માં યેક દોઢ કલાકના "પચીસ" કોિચંગ સ ો હશે. ઉપરાંત, સહભાગીઓને યવહા અનુભવ માટે કેસ ટડી આપવામાં આવશે.

The “Coaching Class” of our Association is one of the best places where the subject

of GST can be learnt in Gujarati language. This being the second year, we are excited to have the participants onboard and have interaction in native language. You are, therefore, requested to enroll yourself or send your juniors and/or staff members without fail and enroll them at the earliest to avoid disappointment.

The enrollment form can be obtained from the Mazgaon Library or can be downloaded from GSTPAM’s website at www.gstpam.org

Thanking you,

Yours faithfully,

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

ENROLMENT FORM FOR

2nd BATCH OF BEGINNERS’ CERTIFICATION COURSE ON GST IN GUJRATI COACHING CLASSES

|

Virtual |

: – |

Zoom Platform |

|

Enrolment Fee |

: |

Rs.1,240/-(Inclusive18%GST) for all participants. |

|

Date |

: |

Monday, 18th November,2024 onwards |

Name of the participant

………………………………………………………………………………………………….. GSTPAM Membership Number……………………..

GSTTIN of Member……………………………………

Professional/Student………………………. Address

……………………………………………………………………………………………………..

……………………….Telephone:(O)………………..……………..®………………………..

E-mail Mobile No.

……………………….…………………………

Amount: Rs. ……………………………………. Cheque No. ………………………… Bank……………………………………………… Branch ……..…………………..

Dated………………………

Participant Details:

E-mail …………………………………………… Mobile No.………………………… WhatsApp No. …………………………………….

Signature …………………….

Note :-

-

Please issue the Cheque in favour of “The Goods &Services Tax Practitioners Association of Maharashtra” (FULL NAME IS REQUIRED TO BE STATED ON THE CHEQUE AS PER RBI DIRECTION).

-

For NEFT payment – Bank of India, Mazgaon- Account No. 007020100001816, IFSC – BKID0000070. Acknowledgement generated through online transaction should be emailed on [email protected] along with Enrolment Form and payment details.

-

Online Payment Link: https://www.gstpam.org/online/event-registration.php

-

Outstation members are requested to make payment online payment.

-

The enrollment form along with payment proof should be submitted at Room No. 104, GST Bhavan, Mazgaon, Mumbai – 400010.

-

Kindly carry the receipt of payment to attend the Lecture.

SUMMARY OF RECENT ADVANCE RULINGS UNDER GST

Compiled by

CA Aditya Surte

-

Meaning and applicability – Electronic Commerce Operator

Applicant provides services for facilitating business transactions through the "Yatri Sathi" App by way of providing a platform to connect actual suppliers (cab drivers) and recipients (passengers intending to use the driver's service). Although applicant owns, operates, and manages the platform, its role is limited to facilitating connection between customers seeking transportation services and drivers willing to provide these services. App merely facilitates sharing of information between drivers and customers, allowing them to connect for transportation services. Applicant's role ends on such connection and effectively does not have any control over subsequent business activities as App platform does not collect consideration and has no control over actual provision of service by the service provider.

Applicant qualifies to be an Electronic Commerce Operator in terms of section 2(45) of CGST Act. However, since supply of services is not made through applicant, but such supply is independent in nature, applicant is not the person liable for discharge of tax liability under section 9(5) of CGST Act.

(West Bengal Authority for Advance Rulings vide Order No. 11/WBAAR/2024-25, decided on 10/09/2024 in the case of Natural Language Technology Research)

-

Classification – Car seat covers

AAR ruled that original car seat covers which are manufactured and designed to permanently fit over raw foam seat of vehicles by OEMs as well as seat manufacturers who further sell to OEMs and are sold with vehicle as an essential and integral part of seat is classifiable under HSN 8708 and GST is liable to pay at 28%.

In appeal, AAAR held that seat cover is nothing but an accessory, which is generally bought by customer for protection and comfort. Seat covers are "extras" that act directly on seats of motor vehicles, adding to style to the interior of motor vehicle, protecting seats from wear and tear. Thus, seat covers are fit to be defined as 'accessories'. Further, on test of sole use/principal use, seat covers merit classification under 8708 as they are only usable and used for vehicles and not of general use.

(Andhra Pradesh Appellate Authority for Advance Rulings vide Order No. ORDER/AAAR/AP/03 (GST)/2024, decided on 26/04/2024 in the case of Saddles International Automotive & Aviation Interiors Pvt. Ltd.)

-

Levy of GST – Penalties for violation of laws and liquidated damages

Penalties imposed for violation of laws cannot be regarded as consideration charged by Government or a Local Authority for tolerating violation of laws. Therefore, penalty, late fees, penal interest, fine etc. levied and collected by applicant for contravention or violations of various laws administered by the applicant for purpose of maintaining discipline and deterrence in regulatee banks, non-banking financial institutes and other institutes are not in nature of a consideration for an activity, hence, such penalties would not constitute a supply

applicant for contravention or violations of various laws administered by the applicant for purpose of maintaining discipline and deterrence in regulatee banks, non-banking financial institutes and other institutes are not in nature of a consideration for an activity, hence, such penalties would not constitute a supply of service.

Penalty of nature for non-performance or under-performance as per contractual agreement by applicant- assessee with third party vendors is in the nature of liquidated damages and amount is paid only to compensate for injury, loss or damage suffered by applicant due to breach of contract. Hence, it does not constitute supply of service and GST is not leviable.

(Maharashtra Authority for Advance Rulings vide Order No. GST-ARA-117 of 2023-24/2024-25/B-53, decided on 31/07/2024 in the case of Reserve Bank of India)

-

Exemption – Pure services to Local Authority

Applicant is providing service of selling of space for advertisement in newspaper and other print media and has provided such services to Pune Municipal Corporation (PMC) and Pimpri Chinchwad Municipal Corporation (PCMC).

-

Said supply by the applicant is supply of pure services as envisaged in Sr. No. 3 of Notification No. 12/2017- Central Tax (Rate).

-

PMC and PCMC are municipal corporations constituted under the Maharashtra Municipal Corporations Act, 1949 and they satisfy definition of a “Local Authority” as per sec. 2(69) of CGST Act.

-

Since as per Circular No. 199/09/2016-Service Tax, advertisement content pertains to functions of education (including primary and secondary schools) and health and sanitation (including hospitals, primary health centres, and dispensaries), and as said pure services are provided to municipal corporations, which are classified as a local authority u/s 2(69), they are exempt from tax under Sl. No. 3 of Notification 12/2017-Central Tax (Rate).

(Maharashtra Authority for Advance Rulings vide Order No. GST-ARA-10 of 2022/2024-25/B-49, decided on 24/07/2024 in the case of Lokmat Media Pvt. Ltd.)

-

-

Classification – Garbage Tipper Vehicle

Vehicle is designed for specific garbage application i.e. garbage disposal keeping in view requirements of National Green Tribunal for supply to Municipal Corporations, Panchayats, etc. As per certificate issued by Automotive Research Association of India (ARAI), it is goods carrier. Applicant admitted that it can be used for transportation of goods. Thus, said vehicle would get covered under Heading No. 8704 90 90 and rate of tax applicable shall be 28 per cent under Sr. No. 166 of Schedule IV of CGST Rates notified by Notification No. 1/2017-CGST Tax (Rate).

(Maharashtra Authority for Advance Rulings vide Order No. GST-ARA-83/2020-21/B-112/Mumbai, decided on 01/12/2022 in the case of Tata Motors Ltd.)

-

ITC eligibility – Rotary parking system

Appellant is providing taxable service falling under category of 'Renting of Immovable Property Service' falling under SAC 997212. Appellant had applied for advance ruling seeking a ruling on admissibility of ITC on 'Rotary Parking System' falling under HSN code 8428. AAR ruled that ITC was not admissible on 'Rotary Parking System' desired to be installed by appellant.

AAAR held that 'Rotary parking system' installed and commissioned at premises of appellant amounts to construction of an immovable property, whereby, ITC on purchase of 'rotary parking system' becomes ineligible u/s 17(5)(d). Ttherefore, ruling pronounced by AAR upheld and appeal dismissed.

(Tamil Nade Appellate Authority for Advance Rulings vide Order No. AAAR/9/2024 & A.R. Appeal No. 04 of 2024, decided on 21/08/2024 in the case of Arthanarisamy Senthil Maharaj)

If you lose faith, you lose all

– Eleanor Roosevelt

GIST OF TRIBUNAL JUDGEMENTS (VAT)

Compiled by

CA Rupa Gami

-

M/s Regal Wines in Vat S.A. No. 120 of 2024 decided on 02/05/2024

First appeal was dismissed for non-attendance and non-prosecution. And therefore, second appeal was preferred. All documents were submitted on 16.04.2021 and the appellant was informed that a reminder would be issued. However, no reminder was issued and the order was passed. It was observed by the Hon'ble Tribunal that the first appeal order was passed on 30.09.2021 and the appeal was filed on 01.04.2024 after a period of three and a half years. That no ground was taken about condonation of delay. Although the appellant was aware that his matter was pending in first appeal proceedings, he had not taken any follow-up about the appeal. Appeal was allowed after imposing costs

(Petitioner represented by Dhaval Talati)

-

M/s Cummins Generator Technologies India Pvt. Ltd. in Vat S.A. No. 71 and 72 decided on 09/05/2024

ITC was denied in assessment. In first appeal some ITC was allowed. Second appeal was preferred. It was contended by the appellant that the ITC was disallowed for purchases of amount below Rs.5000/-, due to mismatch and some ITC was disallowed without giving reason. It was also contended that the Trade Circulars for allowing ITC claim were not followed. It was observed by the Hon'ble Tribunal that the appellant was a diligent dealer and although sufficient time was given to produce the documents, sometimes there can be a delay in gathering documents. Looking to the overall behavior and the appellant being a diligent one, it was necessary to grant time and a direction was given to the first appellate authority to consider the Circulars before disallowing ITC. Regarding ITC disallowed without specifying any reason, the Hon'ble Tribunal observed that it is the fundamental duty of the assessing/ Appellate authorities to provide proper reasons with sound legal backing based on which claims made by the appellant are to be denied. While disallowing ITC, the Trade Circulars should be properly followed.

(Petitioner represented by CA Omkar Deshpande)

-

M/s Rinku Steel Corporation in M.A. Nos. 91 and 92 of 2024 decided on 08/05/2024

Delay of 127 days in filing appeal due to the accountant being busy with day to day work and GST compliance. It was observed by the Tribunal that the assessment order and appeal order were passed ex parte. Costs were imposed at Rs.20000/- for each appeal and the delay condoned.

(Petitioner represented by Adv C.B. Thakar)

-

M/s Metro Steel Traders in M.A. No. 87 of 2024 decided on 10/05/2024

Delay in filing of appeal by 369 days. However, the appellant received the order in physical form only in Feb, 2024. Thereafter appeal was filed in time. The appellant relied on the Tribunal judgements in the case of Dex Win Polymers Pvt. Ltd. (M.A. No. 187 of 2013 in Vat App No.565 of 2013) dated 24.03.2014, Detection

Instruments (I) Pvt. Ltd. (M.A.No.206 of 2018 dated 30.07.2018) and Hon'ble Supreme Court judgement in the case of M.S.T. Katiji (66 STC 228(SC)). The Hon'ble Tribunal observed that looking to the fact that the order in physical form was received after a long time, the delay be condoned subject to cost of Rs.20000/-. (Petitioner represented by Adv. Rahul Thakar)

-

M/s R.K.Infraconstro Pvt. Ltd. in S.A. No. 33 of 2023 decided on 14/05/2024

The appeal is filed under Maharashtra State Tax on Profession, Trades, Callings and Employment Act, 1975 (PT Act). Penalty was levied for non-filing of returns for the F.Y.2021-22 of Rs.5000/- per default. The same was confirmed in first appeal. For appeal to be admitted as per Section 13(3) of the PT Act, full amount had to be paid or else as per the directions of the appellate authority not less than 25% of total amount had to be paid. It was contended by the appellant that the non-filing of returns was not a deliberate case of non-filing but it was due to technical problems faced at the time of uploading of returns. Since the registration was taken in 2021-22 whereas the liability started from 2019-20, for the first year, monthly returns were to be filed and the appellant was trying to file annual return and which was not being accepted. The Tribunal observed that although the levy of penalty was legal and proper, due to the difficulties faced by the appellant, penalty was to be reduced to Rs.5000/- from Rs. 60000/-.

(petitioner represented by C.A. A.B. Patil)

-

M/s Shriganesh Textile and Infrastructure India Pvt. Ltd. in M.A. Nos. 103 and 104 of 2023 decided on 12/06/2024

Delay of 846 days in filing of second appeal. The Applicant contended that the order was never served and considering non-service of order, there is no delay. On attachment of bank account, the applicant approached the Jt. Commr. at Nasik who issued certified copies of order. First appeal was filed. The appeal was dismissed for non-attendance. Thereafter the accountant who was looking into the matter has never received the order. The Hon'ble Tribunal held that since there was no specific proof of service of order, the delay be condoned. (petitioner represented by Adv Subhash Surte)

What you are is God’s gift to you, what you become is your gift to God.

INCOME TAX UPDATES

Compiled by

By Adv. Ajay Talreja

TDS Applicability on Reimbursement of Expenses

In a recent case, a professional service provider raised concerns about the applicability of TDS on the reimbursement of expenses incurred in connection with services rendered during a depot audit. Separate invoices were raised for out-of-pocket expenses, but despite this, TDS was deducted. The issue centered around whether these reimbursements should attract TDS, particularly in light of the provisions introduced by Section 194R of the Income Tax Act?

Observations

Before insertion of Sec. 194R

-

In the instant case, reimbursement of expenses has been made to a chartered account who has incurred expenses in the course of rendering professional services. In this connection, it is pertinent to refer Question No. 30 of CBDT Circular 715 dated 08-08-1995 where it has been clarified that sections 194C and 194J refer to any sum paid and therefore TDS u/s 194C and 194J is applicable on gross amount of bill including reimbursement of expenses.

-

However, in the instant case, separate invoice has been raised for out of pocket expenses. Various decisions has rendered wherein it has been held that no TDS shall be deducted in case of reimbursement of expenses for which separate bills were raised and the provisions of Section 40(a)(ia) is not applicable to such payments. In this regard, reference is drawn to decision of Hon'ble Delhi ITAT in the case of ITO –vs-. Dr. Willmar Schwabe India (P) ltd (2005) 3 SOT 71 (Del) wherein it has been held that reimbursement of out of pocket expenses for which bill was separately raised by consultant did not attract sec. 194J. Further, the CBDT Circular No. 715, dated 08-08-1995 was applicable only in the cases where bills are raised for the gross amount inclusive of professional fees as well as reimbursement of actual expenses.

-

Similar view has been taken in the following cases:

Zephyr Biomedicals -vs.- JCIT [2020] 122 taxmann.com 124 (Bombay HC), Om Satya Exim Pvt. Ltd –vs- ITO (ITA No.1335/Ahd/2010) dated 13-05-2011 ACIT -vs.- Grandprix Fab P. Ltd., (2010) 128 TTJ 60 (Del)

Representation on Incorrect Income Tax Return processing & TDS credit denial

The Karnataka State Chartered Accountants Association (R) (KSCAA) has submitted a representation to the Commissioner of Income Tax, CPC, Bengaluru, regarding issues with the processing of Income Tax Returns (ITR) under Section 143(1) for the Assessment Year 2024-25. The representation highlights that the Central Processing Centre (CPC) has unjustly denied proper TDS credit, leading to erroneous tax demands or reduced refunds despite accurate TDS credit claims in accordance with Section 199 and Section 37B of the Income Tax Act. The CPC has cited issues related to Form 26AS not matching TDS/TCS claims, resulting in discrepancies between reported and claimed credits. KSCAA

requests a review of the processing system to correct technical glitches and urges for system enhancements to facilitate effective online rectification. They also seek guidance on addressing such discrepancies and propose reprocessing of returns if necessary. The representation emphasizes the need for prompt corrective measures to address these issues and to provide clarity on procedures for resolving the discrepancies faced by taxpayers.

Cash payments permissible if assessee can justify necessity & genuineness: ITAT Indore

ITO Vs Ishan Township Pvt. Ltd. (ITAT Indore)

The case of ITO Vs Ishan Township Pvt. Ltd. (ITAT Indore) focuses on the disallowance of cash payments exceeding a certain limit under Section 40A(3) of the Income Tax Act. Section 40A(3) generally disallows such payments unless they meet the conditions outlined in Rule 6DD, which considers business expediency and the absence of banking facilities. According to the Supreme Court ruling in Attar Singh Gurumukh Singh vs. ITO, Section 40A(3) should not be interpreted in isolation but in conjunction with Rule 6DD, ensuring the provision does not hinder legitimate business transactions. If a taxpayer can prove that the payment was genuine and unavoidable, the disallowance should not apply. The ITAT Indore followed the Madhya Pradesh High Court ruling in CIT vs. Achal Alloys (P) Ltd., which holds that no disallowance is necessary if the genuineness of the payment is not in doubt and the payees insisted on cash payments. While the revenue cited decisions from the Madras and Karnataka High Courts that support disallowance, the ITAT Indore adhered to the jurisdictional ruling, emphasizing that cash payments are permissible if the assessee can justify the necessity and genuineness of the payment. This ruling reaffirms that disallowance under Section 40A(3) can be avoided when business expediency and practical constraints are demonstrated.

Key Finding of the ITAT Are summarised as follows:

-

Section 40A(3) prescribes disallowance for cash payment exceeding a particular limit. But then the proviso to section 40A(3) prescribes that no disallowance shall be made “in such cases and under such circumstances as may be prescribed, having regard to the nature and extent of banking facilities available, considerations of business expediency and other relevant factors”.

-

In Attar Singh Gurumukh Singh Vs. ITO (1991) 59 taxmann 11 (SC), the Hon'ble Supreme Court has observed that section 40A(3) must not read in isolation or to the exclusion of Rule 6DD and co-joint reading of this section and rule 6DD makes it clear that the provisions are not intended to restrict the business activities. Further the payments by crossed cheque or bank draft is insisted on to enable the assessing authority to ascertain whether the payment was genuine or it was out of income from disclosed sources. Thus, the Hon'ble Supreme Court has observed that the consideration of business expediency and other relevant factors are not excluded. The genuine and bona fide transactions are not taken out of the sweep of this section. It is open to the assessee to furnish to the satisfaction of the AO the circumstances under which the payment in the manner prescribed in section 40A(3) was not practicable or would have caused genuine difficulty.

-

Rule 6DD prescribes the circumstances for the purpose of aforesaid 2nd proviso to section 40A(3). In Harshila Chordia vs. ITO (2008) 298 ITR 349 (Raj HC) and in Anupam Tele Services vs. ITO (2014) 366 ITR 122 (Guj HC), it is observed that the exceptions contained in rule 6DD are not exhaustive and that the said rule must be interpreted liberally.

-

In CIT vs. Achal Alloys (P) Ltd. 218 ITR 46, the jurisdictional High Court of M.P. has held that if the genuineness of the payment was not exposed to any doubt and cash payments were made on the fulcrum that the payees insisted for cash payment, the disallowance is not attracted.

-

Even if Ld. DR has relied upon the judgment of Hon'ble Madras High court as well as Hon'ble Karnataka High court in revenue's favour, the decision of Hon'ble jurisdictional High Court of M.P. in Achal Alloys (supra) is binding on the ITAT functioning at Indore.

-

The ultimate conclusion is such that if the assessee is able to explain the genuineness of payment as well as the commercial expediency for making cash-payment, there cannot be any disallowance.

-

CBDT Revises Monetary Limits for Tax Income Tax Appeals

The Central Board of Direct Taxes (CBDT) issued Circular No. 09/2024 on September 17, 2024, revising the monetary limits for filing appeals by the Department in income tax cases. This amendment to Circular 5/2024 aims to reduce litigation and provide clarity to taxpayers. The new monetary thresholds are set at Rs. 60 lakh for appeals before the Income Tax Appellate Tribunal (ITAT), Rs. 2 crore for High Courts, and Rs. 5 crore for Supreme Court cases. Earlier the limit was Rs. 50 lakh for appeals before the Income Tax Appellate Tribunal (ITAT), Rs. 1 crore for High Courts, and Rs. 2 crore for Supreme Court cases. These limits will apply to all cases, including those related to TDS and TCS under the Income-tax Act, 1961. Exceptions to these limits, outlined in Circular 5/2024, allow for appeals based on the merits of the case regardless of the tax amount involved. The circular emphasizes that appeals should not be filed solely due to exceeding the monetary limits but rather on the merits of the case, to avoid unnecessary litigation. The new limits take effect immediately and apply to both new and pending appeals in the ITAT, High Courts, and Supreme Court. The CBDT aims to ensure better litigation management and reduce the burden on courts while providing greater certainty in income tax assessments.

Procedure for Filing Form-1 Under DTVSVS 2024

The Directorate of Income Tax (Systems), Bengaluru, under the Central Board of Direct Tax (CBDT), issued Notification No. 4 of 2024, outlining the procedure for filing declarations and undertakings in Form-1 under Rule 4 of The Direct Tax Vivad Se Vishwas Rules, 2024. Taxpayers filing declarations under the scheme must submit Form-1 electronically via the official e-Filing portal of the Income Tax Department. The form can be filed using a digital signature or an Electronic Verification Code (EVC), in accordance with section 140 of the Income Tax Act, 1961.

To file Form-1, taxpayers are required to log in to the e-Filing portal using their credentials, navigate to the relevant section for filing tax forms, and follow the specified procedure. The form includes various schedules that must be completed accurately with necessary validations. Once the form is completed, it can be submitted electronically, and an acknowledgment number is generated upon successful submission. The notification also provides detailed guidelines for viewing and downloading submitted forms. Submission of Form-1 through the e-Filing portal will be considered as compliance with the designated authority requirements under the Direct Tax Vivad Se Vishwas Scheme, 2024. The notification came into effect immediately on September 30, 2024.

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes****** New Delhi, 30th August, 2024

Press Release

CBDT rolls out e-DRS Scheme, 2022

In pursuance of section 245MA in the Income-tax Act, 1961 (hereinafter referred to as “the Act”), the Central Board of Direct Taxes (hereinafter referred to as “CBDT”) had notified the e-Dispute Resolution Scheme, 2022 (hereinafter referred to as “e-DRS”) with the aim to reduce litigation and provide relief to eligible taxpayers. Section 245MA of the Act also provides for the constitution of Dispute Resolution Committees (hereinafter referred to as “DRC”).

The e-DRS enables the taxpayer, who fulfils certain specified conditions as stipulated in section 245MA of the Act, to file an application electronically for dispute resolution to the DRC designated for the region of Principal Chief Commissioner of Income-tax having jurisdiction over the taxpayer. To this end, DRCs have been constituted in all 18 jurisdictional Pr. CCIT regions across the country. The list of such DRCs along with their e-mail addresses is available on

https://www.incometax.gov.in/iec/foportal/help/all-topics/statutory-forms/filestatutoryform/popular-form/form-34-BC

As per e-DRS, a taxpayer can opt for e-Dispute Resolution against the 'specified order' as defined in clause (b) of the Explanation to section 245MA of the Act, which includes an order in which the aggregate sum of variations proposed or made does not exceed Rs.10 lakh and returned income for the relevant assessment year does not exceed Rs. 50 lakh. Further, such order should not be based on search/surveys or information received under an agreement referred to under section 90 or 90A of the Act.

According to e-DRS, a DRC may make modification to the variations in the specified order and decide to grant reduction/waiver of penalty and prosecution in accordance with the provision of rule 44DAC of the Income-tax Rules, 1962 (hereinafter referred to as “the Rules”). The DRC is mandated to pass its order within six months from the end of month in which application for dispute resolution is admitted by it.

The application for e-DRS is to be filed in Form No. 34BC referred in rule 44DAB of the Rules, on the e-filing portal of the Income Tax Department, within one month from the date of receipt of specified order. In cases where appeal has already been filed and is pending before the Commissioner of Income-tax (Appeals), the application for e-DRS, is to be filed on or before 30.09.2024. In cases where the specified order has been passed on or before 31.08.2024 and the time for filing appeal against such order before CIT (Appeals) has not lapsed, the application for dispute resolution can be filed on or before 30.09.2024.

The Tax Payer can access e-DRS module by login on income tax portalhttps://eportal.incometax.gov.in. Login to your account using PAN / TAN as user ID ->Go to Dashboard ->e-File ->Income Tax Forms ->File Income Tax Forms -> under tab `Persons not dependent on any source of Income (Source of Income not relevant)> Dispute Resolution Committee in Certain Cases (Form 34BC) -> Fill Form No. 34BC -> Review the details -> E-Verify the Form No. 34BC using Aadhar OTP, EVC or DSC.

This is another initiative by the Government towards minimizing litigation.

In faith there is enough light for those who want to believe and enough shadows to blind those who don’t.

PARAMERTERS TO FOLLOW UP BEFORE INVESTING IN STOCK……

Compiled by

By Mr. Tushar P. Joshi

As stock market is booming everyone is blindly diverting their funds to buy the Various Stocks. It may be on someone's reference or recommendations.

Once should ideally study and check Various Principles of the Company before investing their hard-earned money. Many public issues are floating in the market and usually oversubscribed. People feel they will get the allotment and also the share price also will be much higher than the subscribed.

But sometime it may happen the share price may open with lower than the base price. Once should not be worried about the same if fundamentals of the company are excellent.

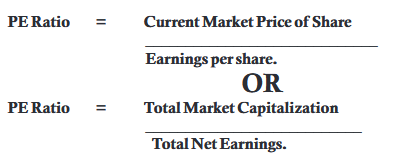

Ideally we should check the P/E Ratio of the stock, which is one of the parameter to check company's performance. This will help in understanding the market price at which a stock is available and justifies the performance.

This will also help to check whether the stock price is overpriced or underpriced. The PE Ratio helps to compare the market price of a share with its earnings i.e. it is the price investor is ready to pay for every rupee that the share earns. This means how much premium he/she is willing to pay. So if the PE Ratio is 25 i.e. 25x this means investor is willing to invest 25/- for every Rs. 1/- that share earns.

For easy understanding I will share the formula.

If the PE Ratio is high it means the stock is overvalued because the market price is higher relative to its earnings or it's a high growth company that is likely to perform excellent in future.

And the low PE Ratio indicates that it's an undervalued company because it's available at low price compare to its intrinsic value.

Thus PE Ratio helps to know stock's Value relative to its peers in the industry or the benchmark. Thus before investing in any company one can study the above ratio.

Faith does not eliminate questions. But faith knows where to take them.

– Elisabeth Elliot

Our members have an option to subscribe to our monthly academic magazine, “GST Review”, which is one of the oldest monthly publications on indirect tax laws in the Country. You get access to indepth articles, analysis and updates on all aspects of indirect tax laws by veteran experts. Latest notifications and circulars are also printed in the same for the benefit of the subscribers.

For the benefit of our readers we are reproducing the index of the topics covered in the last month. Subscription form is available in this News bulletin. Please take this opportunity and become our member and subscribe to the GST Review.

Contents Vol. 7 No. 1 |Mumbai| September, 2024 GST Review JOIN GSTPAM AS A MEMBER

| Topic | Writer | Page No. |

|---|---|---|

| Part – I | ||

| Editorial | Mayur R. Parekh | 5 |

| From the President | Mahesh Madkholkar | 7 |

| GST Updates | Deepali Mehta | 10 |

| Solving Challenges in the Levy and Collection of GST on Virtual Digital Assets (Cryptoassets) in India | Ratan Samal & Manohar Samal | 16 |

| Corruption: Not Inevitable or Acceptable | Kishor Lulla | 23 |

| Mandatory Registration under Section 24(vii) of the CGST Act: A Clarion Call for Agents and Brokers | Amit Lulla | 24 |

| Can GST registration be cancelled when the taxpayer is operating from additional place of business instead of the principal place of business? | Pranav Mehta | 25 |

| रजिस्टर्ड आपणहीन एक कर लागण्याची शक्यता – सर्वोच्च न्यायालयाचा निर्णय | Kishor Lulla | 27 |

| Updates on Real Estate (Regulations & Development) Act, 2016 | Ashwin Shah | 30 |

| Service Tax Updates | Vasudev Mehta | 32 |

| Income Tax Update – Highlights on Recent Amendments | Sonakshi Jhunjhunwala & Sunil Jhunjhunwala | 36 |

| Do You Know? | Moti B. Totlani | 40 |

| Replies to Queries | Deepak Thakkar & Ronak Thakkar | 42 |

| Speaker’s Forum | D. J. Ruparelia & Ashish Ruparelia | 44 |

| Association News | Jatiin N. Chheda & Rahul Thakar | 67 |

| Part – II | ||

| From the Courts | Dhaval Talati | 74 |

| Gist of Advance Rulings | Ashit Shah | 81 |

| Part – III | ||

| Recent Amendments – Notifications/Trade Circulars | ||

| CGST Notification and Circulars | ||

| Circular No. 230/24/2024-GST, New Delhi, dated the 10th September, 2024 |

85 | |

| Circular No. 231/25/2024-GST, New Delhi, dated the 10th September, 2024 |

88 | |

| Circular No. 232/26/2024-GST, New Delhi, dated the 10th September, 2024 |

91 | |

| Circular No. 233/27/2024-GST, New Delhi, dated the 10th September, 2024 |

93 | |

| Instruction No. 02/2024-GST, New Delhi, dated the 12th August 2024 | 95 | |

| Instruction No. 03/2024-GST, New Delhi, Dated 14th August, 2024. | 100 | |

| Advisory for furnishing bank account details before filing GSTR-1/IFF – Notification No. 38/2023 – Central Tax New Delhi, the 4th August, 2023 |

100 | |

| Advisory on Reporting of supplies to un-registered dealers in GSTR1/GSTR 5 | 101 | |

| Advisory for Biometric-Based Aadhaar Authentication and Document Verification for GST Registration Applicants of Bihar, Delhi, Karnataka and Punjab |

101 | |

| Introduction of RCM Liability/ITC Statement | 102 | |

| Invoice Management System | 103 | |

| Announcements Announcement For New Membership, Renewal of Membership & Subscription For Year 2024-25 |

Page 73 | |