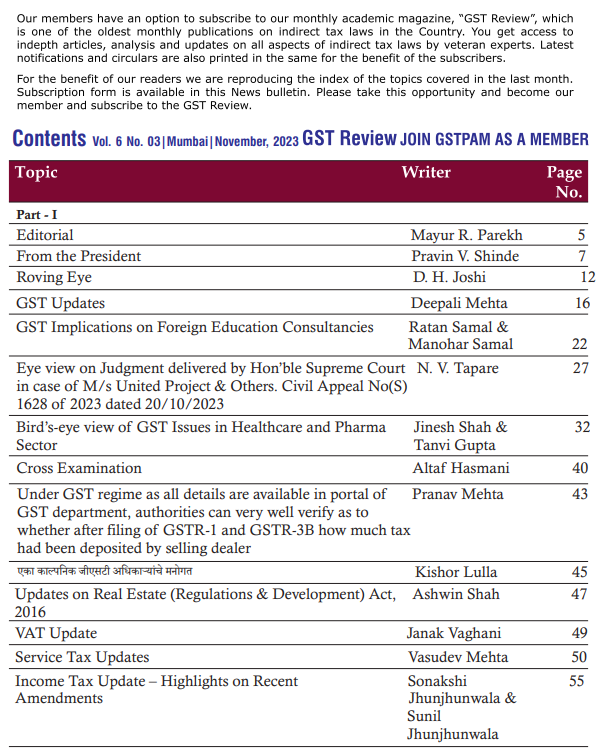

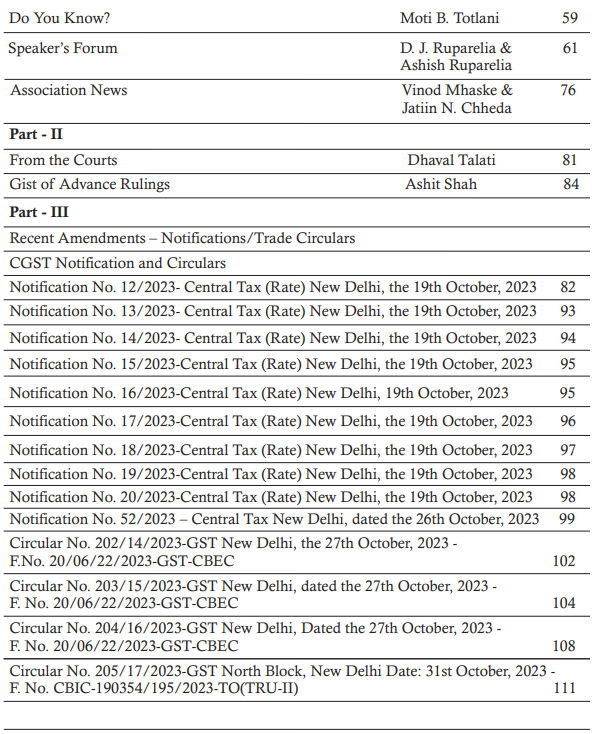

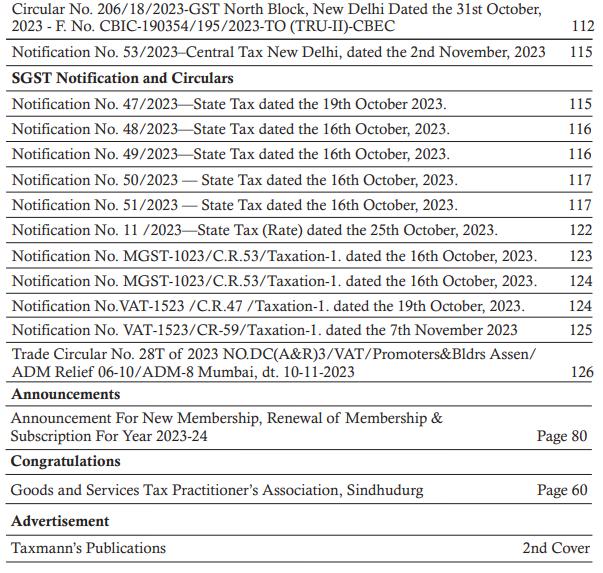

GSTPAM News Bulletin December 2023

CIRCULAR FOR RENEWAL OF MEMBERSHIP/SUBSCRIPTION CHARGES FOR THE F.Y. 2023-24

Dear Members,

RENEWAL OF MEMBERSHIP FOR F.Y. 2023-24

The Membership Fees for the year 2023-24 are due for renewal on 01.04.2023. We appreciate your Continuing support and participation in the activities of our Association.

The timely Renewal of Membership will enable the members to continuously receive the updates on various activities of GSTPAM along with the GSTReview, News Bulletin, Circulars, Messages, Webinars and online access to the website www.gstpam.org. The Life Members only need to renew the subscription charges for the GST Review. The members can also avail the benefit of discount by paying advance for subsequent two years membership fees /subscriptioncharges.

The Membership Renewal Fees received after 30th April, 2023 will be subject to approval of the Managing Committee. If the Renewal fees for a particular year are not paid, then the member is liable to pay Admission Fees again for Renewal in the subsequent year.

Delayed Renewal Members will be provided Pre Renewal GST Review subject to availability upon payment of such additional courier charges.

The details of Membership/Subscription Fees are given below for your ready reference

| Type of Membership | Membership Fees incl. GST | Admission Fees Incl.GST | Subscription Charges for GST Review | Total |

|

New Membership Application |

||||

| Donor Member | 24,780.00 | – | 600.00 | 25,380.00 |

| Patron Member | 17,700.00 | – | 600.00 | 18,300.00 |

| Life Member | 11,800.00 | 944.00 | 600.00 | 13,344.00 |

| Life Member (Conversion from Ordinary) | 11,800.00 | 590.00 | 600.00 | 12,990.00 |

| Ordinary Local Member | 1,770.00 | 590.00 | – | 2,365.00 |

| Ordinary Outstation Member | 1,475.00 | 590.00 | – | 2,065.00 |

New Membership Application (Firm/LLP)

| Ordinary Local Member | 1,770.00 | 944.00 | 0 | 2,174.00 |

| Ordinary Outstation Member | 1,475.00 | 944.00 | 0 | 2,419.00 |

| Patron Member | 17,700.00 | 0 | 600.00 | 18,300.00 |

| Donor Member | 24,780.00 | 0 | 600.00 | 25,380.00 |

Advance Membership/ Subscription charges for subsequent two years 2024-25& 2025-26 (Non-Refundable)

| Ordinary Local Member | 3,186.00 | – | – | 3,186.00 |

| Ordinary Outstation Member | 2,665.00 | – | – | 2,665.00 |

| Life Member (Individual/Firm/LLP) | 0 | – | 1200.00 | 1,200.00 |

| Patron Member | 0 | – | 1200.00 | 1,200.00 |

| Donor Member | 0 | – | 1200.00 | 1,200.00 |

Subscription for GST Review for F.Y. 2023-24 by Non-Members

| Subscription fees for GSTR | – | – |

1000.00 |

1,000.00 |

Advance Membership / Subscription charges for subsequent two years 2024-25& 2025-26 (Non-Refundable)

| Subscription Fees -GSTR | 0 | – | 2000.00 2,000.00 |

Modes of Payment:-

| Cheque | A/c Payee Cheque drawn in favor of “The Goods & Services Tax Practitioners’ Association of Maharashtra” payable at Mumbai. |

| NEFT Details | The Goods & Services Tax Practitioners’ Association of Maharashtra

Bank of India, Mazgaon Branch Current Account No. 007020100001816, IFSC Code – BKID0000070. Online generated transaction Acknowledgement should be sent by email on [email protected] along with membership and payment details Members are requested to send their physical form to the association for Approval, Issuance and Office record. |

| Cash | Renewal form along with requisite amount will be accepted between 10.30 a.m. and 5.30 p.m. on all working days except Saturday at our Office at

Mazgaon Library – Mazgoan: 1stFloor, 104, GST Bhavan, Mazgaon, Mumbai – 400 010 Or Bandra Library – GST Bhavan, Ground Floor, A Wing, BandraKurla Complex, Bandra (East), Mumbai – 400 051. Or Mazgaon Tower – 8 & 9, Mazgaon Tower, 21, MhatarPakhadi Road, Mazgaon, Mumbai – 400 010. |

| Identity

(New Members) |

New Members should provide the following as Identity Proof : PAN, Aadhar Card, Constitution Document.

Address Proof(any one) : Electricity Bill / Passport/ Aadhar Card / Driving License/ Voter id/ Ration Card along with Membership Form |

| Identity Card (For Renewals) | Ordinary Local/Outstation Members should provide Two Photographs along with the Renewal Form for issue of I- cards. |

| Online Payment Link | Members can make online payment on our website www.gstpam.org. Members are requested to download Members Renewal form from website.Update the latest details in the form, scan it and mail at email [email protected]

Payment Link : https://www.gstpam.org/online/renew-membership.php If you are login first time? Click here for create your password |

We value your continuation of the membership and look forward to your renewal to this effect.

Dated:- 21.07.2023

Vinod Mhaske

Jatin Chheda

Hon. Jt.Secretary

|

Guidance Cell Email ID for queries Members can send their queries at [email protected] |

ORDER FORM FOR GSTPAM REFERENCER 2023-24

(Members are requested to take out the photocopy of the Order Form for booking)

For Office use only

| Date | Receipt No. | Coupon No. | Amount |

To

The Convenor,

GSTPAM Referencer Committee

The Goods & Services Tax Practitioners’ Association of Maharashtra

Room No. 8 & 9, Mazgaon Tower, Mhatar Pakhadi Road,

Mazgaon,

Mumbai

Dear Sir,

Please book my/our order of GSTPAM Referencer for the year 2023-24 as given below.

| Sr. | Particulars | Price per copy if booked prior to 15th July 2023 | Price per copy if booked afterto 15th July 2023 | Qty | Total RS. |

| 1 | GSTPAM Referencer 2023-24 Part I & II

(GST, VAT & Allied Law Referencer & Updated GST Rate schedules). |

700 | 750 | ||

| 2 | Courier Charges (For Outstation members only) (per set) | 130 | 130 | ||

| 3 | Courier Charges (For Local members only) (per set) | 100 | 100 |

Note :

- Referencer will be published in Part I & II (for GST, VAT & Allied Laws Referencer & Updated GST rate schedules).

- Applicants requiring more than 5 copies of the Referencer are required to give a request on their letter head along with the order form. Tax Practitioner’s Associations can place order in bulk quantity by making request on their letterhead signed by the Association’s President and Secretary.

- Applicants will be issued receipt at the time of placing of their order. Applicants are requested to bring receipt at the time of taking the delivery of the Referencer. No delivery of the Referencer shall be given, unless the receipt for payment is submitted at the counter. If the receipt for payment is lost, than no delivery of the Referencer shall be given.

The payment for the above order of……………………………………………………………………….… (Rupees in words) is made herewith by Cash /Card /Cheque /Demand Draft No. ………….……dated ……….……. drawn on……………………………………………… Bank Branch, Mumbai.

Signature …………………………….

Membership Number………………………….. Address.…………………………………………………

Name ……………………………………… …………………………………………………………………

……………………………………………… …………………………………………………………………

Office Tel No…………………………………… Residence Tel No………………………………………

E-mail: …………………………………………. Mobile No.…………………………………………….

PROVISIONAL RECEIPT

Received with thanks payment of. ………………… from………………… vide Cash /Card /Cheque /NEFT/Demand Draft No. …………………………. Date ………………. drawn on…………………………………………………Bank ……………… Branch, Mumbai.

Signature ……………………………

Date…………………………………. Name of staff of GSTPAM……………………

Note:

- Please fill in all the details in the above form and send the same to the GSTPAM’s office at Tower or at Mazgaon library along with requisite payment. For Direct Deposit / NEFT payment –

- Bank of India, Mazgaon – Account No. 007020100001817, IFSC Code – BKID0000070. Acknowledgement of the same should be sent by email: [email protected] along with duly filled form.

- Please mention your name and membership number on the reverse side of the Cheque / Demand Draft.

- The counter timings are from 10.30 a.m. to 5.30 p.m. on Monday to Friday.

- The Cheque / DD should be drawn in the name of “THE GOODS AND SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

48th RESIDENTIAL REFRESHER COURSE

Hotel Novotel, At Visakhapatnam

Thursday 29th February, 2024 to Sunday 3rd March,2024

The Residential Refresher Course Committee is pleased to announce its 48th Residential Refresher Course (RRC) on GST at Visakhapatnam, the port city and Industrial Centre in the State of Andhra Pradesh on the Bay of Bengal. The City is famous for its Port, Beautiful Beaches, caves, ancient Buddhist sites and the eastern ghats as well as wild life sanctuaries. It is also know as Vizag and nick named as the “City of Destiny” and the “Jewel of the East Course”.

The object of RRC is to share the essence of professional experience and expertise of the faculties they have gained over the years and where members can study in afresh at mosphere and rejuvenate.

The topics selected for RRC will cover an in-depth and practical understanding of GST Law and the challenges faced in the GST Era. In addition, the Delegates can seek views from seniors on issues they face regarding the interpretation of the law and practical difficulties. These topics are of immense importance and will help professionals/Delegates handling Indirect Tax Matters.

Along with studies, we have planned to visit various tourist places such as local sightseeing in Visakhapatnam which Includes Submarine Museum, Air Craft Museum, Kailasagiri. Simhachalam Temple, Beautifull beaches and many more.

Dates: Thursday 29th February, 2024 to Sunday 3rd March, 2024.

Venue: Hotel Novotel Varun Beach

Dr NTR Beach Rd, Krishna Nagar, Visakhapatnam, Andhra Pradesh 530002 The RRC includes 3 Nights–4 Days accommodation on double occupancy basis and the course material. The Package will start from Lunch on 29th February, 2024 and end with breakfast on 3rd March, 2024.The Paper at the RRC are as under:

| Paper | Topics | Paper Writer | Chairman |

| Paper 1 | Cross Border Transactions – Export,Import, Bond Transfer, Out to Out Transactions | CA Deepali Mehta | Eminent Faculty |

| Paper 2 | Interest, Penalties and offences under GST | CA Aloke Singh | Eminent Faculty |

| Paper 3 | Insights and How to deal with various Parameters of ASMT-10 | Adv. Amol Mane | Eminent Faculty |

| Brains’ Trust Session | Eminent Faculties |

The enrollment Fees are as under:

| Enrollment Fees | Amount | GST18% | Total | |

|

DELEGATE FEES FOR MEMBERS |

||||

| 1 | Fees Paid on or Before 14/12/2023 | Rs.19,500/- | Rs.3,510/- | Rs.23,010/- |

| 2 | Fees Paid After 15/12/2023 | Rs.21,000/- | Rs.3,780/- | Rs.24,780/- |

| 2 | Child rates (With Extra Bed)

*Age 6-12 years Sharing room with parents |

Rs.11,000/- | Rs.1,980/- | Rs.12,980/- |

|

DELEGATE FEES FOR NON- MEMBERS |

||||

| 1 | Fees Paid on or Before 14/12/2023 | Rs.21,000/- | Rs.3,780/- | Rs.24,780/- |

| 2 | Fees Paid After 15/12/2023 | Rs.22,500/- | Rs.4,050/- | Rs.26,550/- |

| 2 | Child rates (With Extra Bed)

*Age 6-12 years Sharing room with parents |

Rs.11,000/- | Rs.1,980/- | Rs.12,980/- |

Notes:-

- In case of cancellation, the refund will be at the discretion of the RRC Committee, the same shall be refunded after completion of event.

- Hotel Check-in Time is 02.00 PM, and Check out Time is 12.00 PM. Early Check-In and Late Checkout will be subject to availability.

- Delegates joining late or leaving early in RRC should inform the Convenor / Office Bearers well in advance.

- All delegates are requested to carry their AADHAR, Driving License, Election Card, and Passport for Photo & Address identification (Any Two) for Train or Air Travel. In addition, members are requested to send a Xerox copy of his/her photo ID with address proof along with Enrollment Form.

- Delegates are advised to carry their medical kit with them.

- Room Service and items other than provided for in the Hotel package will have to be paid Directly in Cash separately by the Delegates to the hotel.

- Tea/Coffeemakers are placed for consumption in all the rooms.

- Delegates are strictly requested to deposit room keys at the reception counter on leaving.

- Please carry our water bottles during Sightseeing Program.

- Members are requested to keep their Identity Cards Compulsory during all Sightseeing programs.

- Allotment of Room shall be at the sole discretion of the RRC Committee only. Any changes required in the program will be at the sole discretion of the RRC Committee.

- We request all Delegates to get themselves fully vaccinated as per the directions of the Government of India and carry their copies of their final certificates as issued.

- Members who enroll for RRC have to renew their Membership for the year 2023-24 before registering for the event; otherwise, they will be treated as Non-Member.

We Wish You All Good Luck in Study at RRC

The Goods &Services Tax Practitioners’ Association of Maharashtra

| Pravin V. Shinde

President |

Sachin Gandhi

Chairman |

Dilip Nathani

Convenor |

Premal Gandhi & Ajay Talreja

Jt. Convenor |

| 9821482020 | 9821121433 | 9324383636/ 9820013469 |

Suggested Train Details from Mumbai to Visakhapatnam on 28th February, 2024

| From | To | Train

Number |

NAME | Departure

Time |

Arrival

Time |

| LTT

Mumbai |

Visakhapatnam | 18520 | Visakhapatnam Express | 6:55

(Wednesday) |

10:40

(Thursday) |

Train Details from Visakhapatnam to Mumbai on 3rd March, 2024.

| From | To | Train

Number |

NAME | Departure

Time |

Arrival

Time |

| Visakhapatnam | LTT Mumbai | 22847 | Vskp Ltt S F | 8:20 AM

(Sunday) |

1:00 PM

(Monday) |

| Visakhapatnam | LTT Mumbai | 18519 | Vskp Ltt Express | 11:20 PM

(Sunday) |

4:15 AM

(Tue) |

Suggested Flight Details from Mumbai to Visakhapatnam on 29th February, 2024.

| From | To | Flight Number | Airline

Name |

Departure

Time |

Arrival

Time |

| Mumbai | Visakhapatnam | 6E 5107, 6E 581

(Via Chennai) |

Indigo Airlines | 7:00 | 11:45 |

| Mumbai | Visakhapatnam | 6E 5246, 6E 879

( Via Hyderabad) |

Indigo Airlines | 8:00 | 11:50 |

| Mumbai | Visakhapatnam | 6E 5352, 6E 6336

(Via Bengaluru) |

Indigo Airlines | 6:05 | 13:55 |

| Mumbai | Visakhapatnam | 6E 5296, 6E 6336

(Via Bengaluru) |

Indigo Airlines | 7:30 | 13:55 |

Suggested Flight Details from Visakhapatnam to Mumbai on 3rdMarch, 2024.

| From | To | Flight Number | Airline

Name |

Departure

Time |

Arrival

Time |

| Visakhapatnam | Mumbai | AI 654 | Air India | 15:50 | 18:05 |

| Visakhapatnam | Mumbai | 6E 5247 | Indigo | 15:10 | 17:15 |

| Visakhapatnam | Mumbai | I5 1529, I5 1782

(Via Bengaluru) |

Air Asia | 11:00 | 15:50 |

| Visakhapatnam | Mumbai | 6E 5309, 6E 5255

(Via Bengaluru) |

Indigo | 14:35 | 19:50 |

ENROLMENT FORM for

48th RESIDENTIAL REFRESHER COURSE Hotel Novotel, At Visakhapatnam

Thursday 29th February, 2024 to Sunday 3rd March, 2024

To,

The Convenor,

Residential Refresher Course Committee,

The Goods and Services Tax Practitioners’ Association of Maharashtra,

8 & 9, Mazgaon Tower, 21, Mhatar Pakhadi Road,

Mazgaon, Mumbai-400 010.

Dear Sir,

Kindly enroll me /us as the delegate(s) for the 48 th RRC to be held Hotel Novotel, at Visakhapatnam between Thursday 29th February, 2024 to Sunday 3rd March, 2024. My relevant details are as under

* NAME ……………………………………………………………………………………… (Age:…….yrs.)

* ADDRESS………………………………………………………………………………………………………

……………………………………………………………………………………………………..

* GSTIN…………………………..………….…..………………………………………………………………..

* GSTPAM Membership No……………….…………………………………………………………………….

* Telephone (O)………………………………®……………………………………………………………………..

* Email:…………………………………………………………………………………………………………………………….

* Mobile……………………………………………………………………………………………………………………………

* Food preference Veg Non-veg

* Whether Jain food is required Yes No

* If joining with family, please fill in the following details:

- Name of Spouse:……………………………………………… (Age…………yrs.)

- Name of Child/Children: (i) ……………………………………(Age…………yrs.)(ii) ……………………………………(Age…………yrs.)

* My preference of Room Partner (in case of not accompanied by a family member)

………….………………………………………………………………………………………………….

(Signature)

Delegate Fees:

The fees include 3 Nights – 4 Days accommodation with the course material. The enrollment Fees are as under:

| Enrollment Fees | Amount | GST18% | Total | |

|

DELEGATE FEES FOR MEMBERS |

||||

| 1 | Fees Paid on or Before 14/12/2023 | Rs.19,500/- | Rs.3,510/- | Rs.23,010/- |

| 2 | Fees Paid After 15/12/2023 | Rs.21,000/- | Rs.3,780/- | Rs.24,780/- |

| 3 | Child rates (With Extra Bed)

*Age 6-12 years Sharing room with parents |

Rs.11,000/- | Rs.1,980/- | Rs.12,980/- |

|

DELEGATE FEES FOR NON- MEMBERS |

||||

| 1 | Fees Paid on or Before 14/12/2023 | Rs.21,000/- | Rs.3,780/- | Rs.24,780/- |

| 2 | Fees Paid After 15/12/2023 | Rs.22,500/- | Rs.4,050/- | Rs.26,550/- |

| 3 | Child rates (With Extra Bed)

*Age 6-12 years Sharing room with parents |

Rs.11,000/- | Rs.1,980/- | Rs.12,980/- |

Member means a member of The Goods and Services Tax Practitioners’ Association of Maharashtra along with his/her Spouse and Children only. A member who enrolls for RRC has to renew the Membership for 2023-2024 before enrolling for the event.

Details of Payment

Cheque/ D.D.No……..………………… Bank……………………..…………………………..……. Branch…………….……… Dated……………………… NEFT details ….………………………………….

Bank details of GSTPAM are as under:

Bank:- Bank of India

Name:- The Goods & Services Tax Practitioners’ Association of Maharashtra

Branch:- Mazgaon, Mumbai

A/c No. :- 007020100001816 – Current A/c

IFSC Code :- BKID0000070

Notes:-

- Acknowledgment generated through online transactions should be emailed to [email protected] along with Enrollment Form and payment details.

- Online Payment Link: https://www.gstpam.org/online/event-registration.php

- Please issue the Cheque in favour of ‘‘The Goods & Services Tax Practitioners’ Association of Maharashtra’’ (FULL NAME IS REQUIRED TO BE STATED ON THE CHEQUE AS PER RBI DIRECTION).

- Please tick/fill in the appropriate boxes.

- All delegates are requested to attach a xerox copy of his / her photo ID with addressproof.

- Booking for RRC will be accepted and confirmed only on payment of full delegate fees.

- Please attach your Travels details with the enrollment form and email to [email protected]

CIRCULAR FOR 41ST BATCH OF GST BEGINNERS COACHING CLASS FOR THE YEAR 2023-24

Dear Members,

We are happy to announce that “41st Batch of GST Beginners Coaching Classes” will commence on 15th January, 2024 in Hybrid mode.

Details of Coaching Class are as under

Virtual : Zoom Platform

Enrollment Fee : Rs.1950/- (Incl GST) for all participants

Salient Features of the Coaching Class:

- The object of the Coaching Class is to train and groom the new entrants or would be entrants in Indirect Taxes Practice particularly in GST in a very professional manner. Our well known seniors not only teach what is written in the books but also share the essence of their professional experience which they have gained over the years. This can be of enormous help and use to the new entrants. Here, students not only get knowledge but also wisdom by interacting with the seniors.

- Our expert faculties will provide notes on the respective topics.

- It has been now more than 6 years of implementation of GST, the classes will help the member and students to solve their doubt.

- The classes would be conducted, having “Twenty Four” Coaching Sessions. Also, the participants would be given case studies for the practical experience.

The “Coaching Class” of our Association is one of the best places where the subject of GST can be learnt in a very professional manner. Our Coaching Classes are so popular that apart from new entrants, many members who are not new, but whose craving for perpetual learning is very strong, enroll every year. You are, therefore, requested to enroll yourself or send your juniors and/or staff members without fail and enroll them at the earliest to avoid disappointment.

The enrollment form can be obtained from the Mazgaon Library or can be downloaded from GSTPAM’s website at www.gstpam.org

Thanking you,

Yours faithfully,

| Pravin V. Shinde | Jatin Chheda | Haresh Chhugani | Vivekanand Rao, Chaitanya Vaidya & |

| Ashwin Shivnani | |||

| President | Chairman | Convenor | Joint Convenors |

For further details, please visit www.gstpam.org or contact:

Mr. Jatin Chheda, Chairman & Hon. Jt. Secretary (Mob. No.: 9821669090)

Mr. Haresh Chhugani, Convenor ( Mob. No. 9820268035)

Mr. Ashwin Shivnani, Jt. Convenor ( Mob. No. 9819897488)

Mr. Vivekanand Rao, Jt. Convenor ( Mob. No. 9820036040)

Mr. Chaitanya Vaidya, Jt. Convenor ( Mob. No. 9511291003)

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

ENROLMENT FORM FOR

41st Batch of GST Beginners Coaching Classes

| Virtual | :– | Zoom Platform |

| Enrolment Fee | : | Rs. 1,950/- (Inclusive 18% GST) for all participants. |

| Date | : | Monday, 15th January, 2024, onwards |

Name of the participant

…………………………………………………………………………………………………………….

GSTPAM Membership Number……………………..

GSTTIN of Member……………………………………

Address

……………………………………………………………………………………………………………………..

Telephone: (O)………………..…………….. ® ………………………..

E-mail …………………………………………… Mobile No. ………………………..

Amount: Rs. ……………………………………. Cheque No. …………………………

Bank……………………………………………… Branch ……..…………………..

Dated………………………

Participant Details:

E-mail …………………………………………… Mobile No.…………………………

Whats app No. …………………………………….

Signature …………………….

Notes:

- Cheque/D.D. should be drawn in favour of the “The Goods & Services Tax Practitioners’ Association of Maharashtra” payable at Mumbai.

- The enrollment form along with Cheque / DD/ Cash should be submitted at Room No. 104, GST Bhavan , Mazgoan, Mumbai 400 010.

- Payment Link : https://www.gstpam.org/online/event-registration.php

- NEFT detail – Bank of India, Mazgaon Branch – Account No. 007020100001816, IFSC Code – BKID0000070

- Acknowledgement generated through online transaction should be emailed [email protected] along with Enrolment Form and payment details

- Participant’s Email id & Mobile No. shall be used for schedule communication

- Kindly carry the receipt of payment to attend the Coaching Class.

- The Association reserves the right to change and alter the schedule if required.

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

INTENSIVE STUDY COURSE CIRCULAR FOR THE YEAR 2023-24

Respected Members,

It is 7th year of the GST act is implemented. After implementation of GST, whole fraternity of Indirect Tax Practitioners and Trade are facing various challenges with regard to implementation, transition, interpretation, practical aspects, prescribed schedule rates, AAR, Department Audit, various notices related to ITC mismatch and so on.

We all are aware about the practical difficulties we are facing while applying the rules and procedures of the GST law and the frequent amendments to the law especially due to frequent lockdown. With the view to update our fellow members on the latest development in law and to discuss the practical issues arising there from, our association has been regularly conducting Intensive Study Course. This year the Intensive Study Course is designed to enable the members to study and discuss various issues on Indirect Tax Laws mainly on GST Law, as well as on profession tax, etc.

With the same enthusiasm to discuss mainly on various aspects of GST Law, We are starting our hybrid mode Intensive Study Course for the year 2023-24 from Friday, 15-12-2023 onwards.

The Intensive Study Course is such an academic activity of our association which is designed to facilitate the members to study and discuss various issues in group. At the intensive study Course, one of the members acts as a group leader and leads the discussion on issues of the relevant subject / topic and one of the seniors in the profession monitors the discussion. The meetings are generally arranged ON Hybrid mode on 1st, 3rd and 5th Friday of the month during 3.30 p.m. to 6.00 p.m. There are around 15-16 meetings will be arranged for the Intensive Study Circle.

1st The inaugural meeting of the Intensive Study Course is scheduled to be held on Friday, 15-12-2023 between 3.30 p.m. & 6.00 p.m. on hybrid mode on the subject “Issues and Intricacies in GSTR 9 / 9C along with implications on Notices by GST Department”. The topic will be lead by Group Leader CA Dharmen Shah and the Monitor of CA Mayur Parekh.

The group strength is restricted to a limited number of members to facilitate better interaction within the group. The Intensive Study Course Fee is fixed at Rs. 1,650/- including GST for Members and Rs. 1,850/- including GST for Non members. You are requested to enroll at the earliest to avoid disappointment. Kindly use photocopy of the Enrolment form printed here in below. Also write your email address and mobile number for better communication.

Member interested to act as group leader should inform by filling up the option in the Form of “I wish to be a group leader for the subject” and are requested to contact the Convener on the mobile numbers mentioned- on Cell No. 9224386682/9821441740 / 9892512345/9870008752

Note :

- The First Meeting of the ISC is proposed to be a HYBRID meeting. The members joining the ISC are requested to fill the attached form for selection of Only Physical Mode or Only Virtual Mode. The Physical mode will be continued only if majority participants opt for the Physical Mode. (Else only Virtual meetings shall be held no Hybrid Meeting shall be held)

- GST lectures will be in form of group discussion, which will be helpful to study the GST law.

- If the materials are received 3 days earlier to the date of meeting, the same will be circulated through mails to the participants.

- Participants are requested to discuss only the points related to the particular topic of the meeting and to come prepared for the subject, which will be helpful for the discussion.

| Pranav Kapadia

Chairman |

Hiral Shah

Convenor |

Sanjay Gajra

Jt.Convenor |

Sujoy Mehta

Jt.Convenor |

Bhavin Mehta

Jt.Convenor |

| 9224386682 | 9821441740 | 9892512345 | 9870008752 |

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

ENROLMENT FORM FOR INTENSIVE STUDY COURSE CIRCULAR FOR THE

YEAR 2023-24

To,

Convener,

Intensive Study Course

The GSTPAM, Mazgaon, Mumbai – 400 010.

Dear Sir,

Please enroll me as a participant for the Intensive Study Course for the year 2023-24. The Registration fees of Rs.1,650/- (for members) / and Rs.1,850/- (for non-members) 18% Including GST is enclosed herewith by Cash /DD / Cheque No._____________________dated__________________drawn on______________________________

Particulars of Member/Participant :

Name: _______________________________________________________

Educational Qualification: _____________________________________________

Address for Communication:____________________________________________

Telephone No. Office :___________________________________________ Res.________________________________

Email ID : _______________________________Mob. No,__________________________________________

GSTPAM Membership No:____________________________________________________________

GSTIN (if Applicable):___________________________________________________________________________

I also wish to be a group leader for the subject of_______________________________________ and suitable available date will be :_________________________________________

I would like to attend the Meeting (Please Tick only one option)

Only Physical Mode

Only Virtual ModeThe Physical mode will be continued only if majority participants opt for the Physical Mode

Signature _____________________

Note :-

- Please issue the Cheque in favour of ”The Goods & Services Tax Practitioners’ Association of Maharashtra” (FULL NAME IS REQUIRED TO BE STATED ON THE CHEQUE AS PER RBI DIRECTION).

- For NEFT payment – Bank of India, Mazgaon- Account No. 007020100001816, IFSC – BKID0000070. Acknowledgement generated through online transaction should be emailed on [email protected] along with Enrolment Form and payment details.

- Online Payment Link: https://www.gstpam.org/online/event-registration.php

- Outstation members are requested to make payment online payment.

- The enrollment form along with payment proof should be submitted at Room No. 104, Vikrikar Bhavan, Mazgaon, Mumbai – 400010.

- Kindly carry the receipt of payment to attend the Lecture.

- The Association reserves the right to change and alter the schedule if required.

GST, MVAT & ALLIED LAW UPDATESCompiled by Adv. Pravin Shinde |

|

|

Notification under Central Tax |

||

| Notification No. | Date of Issue | Subject |

| 54/2023-Central Tax | 17.11.2023 | Seeks to amend Notification No. 27/2022 dated 26.12.2022 to notify biometric-based Aadhaar authentication for GST registration in the State of Andhra Pradesh. |

|

Notification / Circular Under Maharashtra Goods and Services Tax Act, 2017 (MGST) |

||

| Notifcation / Trade Circular No | Date of Issue | Subject |

| Circular No.

205/17/2023- GST-26T of 2023 |

10.11.2023 | Clarification regarding GST rate on imitation zari thread or yarn |

| Circular No.

206/18/2023- GST-27T of 2023 |

10.11.2023 | Clarification regarding applicability of GST on certain services |

| Notification No.

12/2023— State Tax (Rate). |

23.11.2023 | Amendment in Notification No. 11/2017-State Tax (Rate) |

| Notification No.

13/2023— State Tax (Rate). |

23.11.2023 | Amendment in Notification No. 12/2017-State Tax (Rate) |

| Notification No.

14/2023— State Tax (Rate). |

23.11.2023 | Amendment in Notification No. 13/2017-State Tax (Rate) |

| Notification No.

15/2023— State Tax (Rate). |

23.11.2023 | Amendment in Notification No. 15/2017-State Tax (Rate) |

| Notification No.

16/2023— State Tax (Rate). |

23.11.2023 | Amendment in Notification No. 17/2017-State Tax (Rate) |

| Notification No.

52/2023 —State Tax |

24.11.2023 | Seeks to make amendments (Fourth Amendment, 2023) to the CGST Rules, 2017 |

| Notification No.

17/2023— State Tax (Rate). |

24.11.2023 | Amendment in Notification No. 01/2017-State Tax (Rate) |

| Notification No.

18/2023— State Tax (Rate). |

24.11.2023 | Amendment in Notification No. 02/2017-State Tax (Rate) |

| Notification No.

19/2023— State Tax (Rate). |

24.11.2023 | Amendment in Notification No. 04/2017-State Tax (Rate) |

| Notification No.

20/2023— State Tax (Rate). |

24.11.2023 | Amendment in Notification No. 05/2017-State Tax (Rate) |

|

Trade Circular under MVAT Act |

||

| Notification No. | Date of Issue | Subject |

| No. VAT-Trade Circular No. 28T OF 2023 |

10.11.2023 | Stay of recovery in the matter of Special Leave Petition filed by the Promoters and Builders Association and the Maharashtra Chamber of Housing Industry (MCHI) |

The best use of your money is to buy control of your Time.

– Brian Feroldi

| GIST OF TRIBUNAL JUDGEMENTS (VAT)

Compiled by CA Rupa Gami |

|

-

- M/s Jatin International in S.A. Nos. 456 to 458 of 2019 decided on 15/02/2023

Set off was disallowed on account of purchases from suspicious dealers, RC cancelled dealers, non- traceable dealers and excess set off claimed as per J-1 of E-704 filed by respective suppliers. First appeal was dismissed for non-attendance. Miscellaneous Application filed by the appellant for condonation of delay was allowed.The appellant had not made part payment while filing the second appeal by relying on the judgement of Bombay High Court, Nagpur Bench in the case of M/s Anshul Impex Pvt. Ltd. in Sales Tax Appeal No. 02/18 decided on 29/09/2018. The Revenue relied on the Bombay High Court judgement, Full Bench in the case of M/s United Projects in W.P. 2883 of 2018, where the Court has observed that the decision in the case of M/s Anshul Impex is not a good law. The Hon’ble Bombay High Court in its full bench decision in the case of M/s United Projects decided on 12/07/2022, had made it clear that the State Government is empowered to make provisions like section 26(6B) applicable retrospectively to pending proceedings. Hence the Hon’ble Tribunal dismissed the appeal for want of statutory payment. (Petitioner represented by Adv. Shri V.V. Guthe) - M/s Mahyco Monsanto Biotech (India) Vat Second Appeal No.110 of 2021 decided on 20/02/2023

The appellant is a joint venture company engaged in the business of developing and commercializing insect resistant hybrid planting seeds of cotton. The appellant has been granted license to use Monsanto technology. The said technology is being sub-licensed to various seed companies. On the application filed for DDQ, the Commissioner held that the transaction is liable to tax under the Lease Act. On appeal before the Tribunal, it was held that the Lease Act did not cover the entry. On reference application filed by the Department, the same is pending before the High Court.Also, the appellant applied for DDQ under Vat Act, where the Commissioner held the same to be liable to tax under MVAT Act with no prospective effect. The matter went before the Supreme Court where the SLP is pending with stay being granted against recovery of tax.Against the Assessment Order for another period, the first appeal was dismissed and the appellant has filed second appeal with no part payment as the Supreme Court had granted stay in the pending SLP. The Tribunal held that the part payment was mandatory and therefore till the contentious issue is decided by the higher forum, the present set of documents would remain in pending status and would not be termed as appeal. It would remain a petition.(Petitioner represented by Adv. Shri Mihir Mehta) - M/s Innovator Façade System Ltd. Vat Appeal Nos. 146 to 148 of 2018 decided on 21/02/2023

Assessment Order passed ex parte. In first appeal part payment demanded for full tax. The Assessment Order was passed prior to the coming into effect of amendment of section 26(6B) of MVAT Act. The Hon’ble Tribunal taking into account the guiding principle of the amended provision reduced the part payment to 10% of tax.(Petitioner represented by Adv. Shri. C.B. Thakar) - M/s Pooja Engineers. Vat Second Appeal No.116 of 2021 decided on 08/02/2023

The place of business of the appellant is a residential flat and he and his family is not residing in the said flat but at Delhi. The notice for final hearing sent by the first appellate authority was served by pasting and thus the appellant was not able to attend. The Hon’ble Tribunal held that as the appellant was ready to remain present with the books of accounts, an opportunity must be given to the appellant. Regard must be had for true administration of justice and justice should not be defeated by disposing the matter without considering the merit. It is the settled principle of law that the party must get sufficient opportunity to defend own rights. In order to decide the issue on merit, the order needs to be set aside and no prejudice would be caused to the respondent. The matter was remanded back.

(Petitioner represented by Adv. Shri. D. K. Bapat) - M/s Prijal Heat Exchangers Pvt. Ltd. Vat Second Appeal No. 20 of 2021 decided on 28/02/2023

The sales returns were disallowed in Assessment Order. It was contended by the appellant that the first appellate authority did not grant opportunity to the appellant to cross verify whether the buyers have claimed full set off in Annexure J2 during the course of appeal proceedings. However, the Jt. Commr. Insisted on producing debit notes of the buyers. The copies of J2 of the buyers were produced and it showed that the buyers had not claimed set off on goods returns. The appellant produced the document of Excise Invoice issued by the purchaser instead of debit notes but the same was not considered as a document prescribed under the MVAT Act. Since the appellant produced additional documents before the Hon’ble Tribunal to support his claim the matter was remanded to provide an opportunity to the appellant to produce all supporting documents before the first appellate authority.

(Petitioner represented by CA Shri R.P.Mody)

- M/s Jatin International in S.A. Nos. 456 to 458 of 2019 decided on 15/02/2023

Be not afraid of discomfort. If you can’t put yourself in a situation where you are uncomfortable, then you will never grow. You will never change. You’ll never learn.

– Jason Reynolds

INCOME TAX UPDATESCompiled By By Adv. Ajay Talreja |

|

Hemant Dinkar Kandlur Vs CIT (Bombay High Court)

The Bombay High Court has delivered a significant judgment in the case of Hemant Dinkar Kandlur vs. CIT, addressing the retrospective application of an amendment to Section 54F of the Income Tax Act, 1961.

This article provides an in-depth analysis of the case and its implications.

Detailed Analysis: The case revolves around a dispute concerning the applicability of Section 54F of the Income Tax Act. The petitioner, a Non-Resident Indian working in the USA, sold a residential property in India and invested the sale proceeds in the purchase of another residential property in the United States of America. He believed that his income was not taxable in India due to his NRI status and filed a return of income for Assessment Year 2014-15, showing NIL taxable income. However, the Centralized Processing Centre (CPC) processed his return and determined a tax refund due to him. It was during this process that it was discovered that the petitioner had sold a residential property in India and invested the capital gains in a property in the USA, exceeding the amount of Long Term Capital Gain (LTCG). The petitioner also deposited an amount greater than the LTCG into a Capital Gain Account Scheme (CGAS).

Upon realizing that he had misunderstood the tax provisions, the petitioner applied for a rectification of the return. Subsequently, he sought a revision of the intimation under Section 143(1) of the Act. He informed the tax authorities of his investment in a property in the USA and requested the release of funds deposited in the CGAS. However, the Commissioner of Income Tax (International Taxation)-3 rejected the petitioner’s claim, citing an amendment in Section 54(1) of the Act made by the Finance (No.2) Act of 2014. The amendment added the words “in India” to the provision, specifying that the new residential property should be situated in India to claim the deduction under Section 54 of the Act. The petitioner challenged this rejection, arguing that the amendment was prospective and did not apply to his case, which pertained to a transaction prior to the amendment. He cited various decisions to support his contention, emphasizing that the language of the pre-amended Section 54(F) of the Act did not impose any restriction on the location of the new property. The respondent, representing the tax authorities, contended that the petitioner’s revised return was filed beyond the due date and questioned the cost of the new property declared by the petitioner. Furthermore, it was argued that Section 54 of the Act could only be applied when the new property was purchased or constructed “in India.” The key legal argument centered on whether the amendment to Section 54(1) was clarificatory or substantive in nature. The respondent argued that it was clarificatory and had retrospective effect. However, the petitioner contended that the amendment was prospective and did not apply to transactions before its enactment.

The High Court examined the pre-amendment and post-amendment versions of Section 54(F) and concluded that the language of the pre-amendment provision was clear and unambiguous. It did not impose any geographical restrictions on the location of the new property. The insertion of the words “in India” in the amended provision came into effect from April 1, 2015,and was intended to apply prospectively to future periods. The court also considered the absence of a clear statement in the statute that the amendment was declaratory or clarificatory. Without such a statement, the amendment could not be considered merely clarificatory. Additionally , the court found that the amendment did not refer to Section 5(2) of the Act, making it clear that it was not a clarification of existing law. Conclusion: In a significant judgment, the Bombay High Court ruled that the amendment to Section 54(1) of the Income Tax Act, which added the words “in India,” was not retrospective in nature. The court held that the amendment applied prospectively and did not impose any geographical restrictions on the location of the new property for the purposes of claiming a deduction under Section 54 of the Act.

How to File Income Tax Appeal before CIT (A) with Case Study

Dear readers, as we all know, Income Tax department has started faceless assessment of all Scrutiny cases few years back. Use of technology in case of scrutiny cases gives us a comfort to give reply of all department queries at our convenience. But, this technology is becoming hurdle for senior citizens and those who are not technology savvy. Further, in case of faceless assessment, case is decided on the basis of documents produced and how effectively we convey our point to Income Tax department. In some cases, it is observed that, even after submitting requisite documents with Income tax officer, the officer does not consider that document while assessment proceedings and demand order will be passed against the assessee. Income Tax department has taken many steps to avoid such kind of error while doing faceless assessment but this process cannot be 100% error free as of now.

At a Glance A tax payer aggrieved by any of the orders passed by the Income tax authorities, which are specified as ‘appealable orders’ in the Income Tax Act, 1961, has a right to file an appeal before the Commissioner of Income Tax (Appeals). Taxpayers can file appeal against the orders of assessing officer before the CIT (A), having, jurisdiction over the taxpayer. Appeal before a CIT (A) can be filed only in the prescribed form number 35 and is to be accompanied by the proof of payment of prescribed appeal fee and original copy of the notice of demand issued by the assessing officer under section 156 and a copy of the order. Appeal filing is an online process which can be done after login into assessee account.

Here, to understand better, we will take a real case study, where Mr. A is a retired person, who is retired from PSU and get a corpus say Rs.75,00,000/- in the form of EPF, Gratuity, leave encashment etc and being senior citizen and unawareness of law, he does not file his ITR. Later, he received notice U/s 148A(a) and Section 148 of Income Tax Act, 1961. In response to this Mr. A Filed his ITR and provide documents that are available with him. One of the documents that are asked is Form 16 issued by employer but Mr. A is not able to provide the same because it is not provided by employer and he is not able to visit his employer office due to his age and health issues in Family. But he provided Salary slip issued by employer as documentary proof which shows all calculations but assessing officer ignore this evidence and raise a demand of Rs.8,00,000/-. Further, penalty proceedings are also initiated amounting to Rs.16,00,000/-

Here the mistakes did by Mr. A are: Non Filing of ITR even he has received such high value transaction Taking the case lightly and responding to notices by himself without knowledge of law Providing half evidences and not explaining the reason of providing less documents in comparison to as required by officer No objection raised on draft order issued by officer before passing of final assessment order Now, Mr. A has only 2 Choices, either pay Rs.24,00,000/- as demand or raise the issue before CIT(A) within the specified time period and following the specified process of appeal filing like Filing appeal in Form 35 online, pay the requisite appeal fees and submit the required documents along with Form 35. The most crucial part of Filing Form 35 is Facts of the case and Grounds of the appeal. Here, full focus required to find out the mistakes, if any committed by officer while drafting assessment order or not following the sequence of assessment proceedings. Further, we have to highlight the documents that are submitted by us or any other new evidence that we want to present that may change the case proceedings, which we have submitted with the officer but the same is not considered while doing assessment.

Drafting Facts of the case and Grounds of appeal requires analyzing skills and knowledge of law. This is very crucial point, here we have to highlight the mistake committed by officers and facts that are ignored, which if considered then fate of case will be different. For educational purpose, one point that can be used as Grounds of appeal is as follows: “The primary ground of appeal is the non-consideration of critical evidence submitted by the assessee during the assessment proceedings. The September 2017 salary slip (Showing Full & Final settlement of all dues of the assessee by the employer at the time of retirement), which meticulously outlines calculations related to exempt income under Section 10 and the deduction claimed under Section 80C, was inexplicably overlooked by the assessing officer. This oversight has resulted in an unjust and inflated demand” Above is an illustration of Grounds of appeal. There is not fixed format of Facts of the case and Grounds of of the appeal but the same must be drafted in professional language and must convey our view point to the appellant authority. Each case is unique and requires difference kinds of drafting skills.

Clarification with regard to trust audit reports issued by CBDT

The Central Board of Direct Taxes (CBDT), under the Ministry of Finance in India, plays a pivotal role in interpreting and implementing the Income-tax Act. In a recent development, CBDT has issued Circular No. 17/2023 on October 9, 2023, under Section 119 of the Income-tax Act, 1961. This circular provides crucial clarifications regarding trust audit reports for various entities, including funds, trusts, institutions, universities, educational institutions, hospitals, and medical institutions. Purpose of Audit Reports: The CBDT circular focuses on audit reports concerning funds, trusts, institutions, universities, educational institutions, hospitals, and medical institutions. These reports are required under specific sections of the Income-tax Act, namely clause (b) of the tenth proviso to clause (23C) of section 10, or sub-clause (ii) of clause (b) of sub-section (1) of section 12A of the Income-tax Act, 1961. Challenges in Reporting Substantial Contributions: The circular acknowledges that difficulties have arisen when providing details about individuals who have made ‘substantial contributions’ to the trust or institution. These contributions refer to any person whose total contribution up to the end of the relevant previous year exceeds fifty thousand rupees, as mentioned in section 13(3)(b) of the Income-tax Act.

Clarifications Provided: To address these challenges and streamline the reporting process, the CBDT has issued specific instructions for the assessment year 2023-24. These instructions pertain to Form No. 10B and Form No. 10BB, particularly in row 41 and row 28, respectively.

Details of Persons with Substantial Contributions: The circular allows for the inclusion of details of persons making substantial contributions to be given with respect to those individuals whose total contribution during the previous year exceeds fifty thousand rupees.

Relatives of Contributors: In cases where available, details of relatives of such contributors can be provided. Concerns with Substantial Interest: Furthermore, if applicable, details of concerns in which such contributors have substantial interest can also be provided.

This clarification aims to simplify the reporting process and ensure that accurate information is furnished in trust audit reports.

Conclusion: The CBDT’s Circular No. 17/2023 dated October 9, 2023, provides essential guidance regarding trust audit reports for various entities, including funds, trusts, institutions, universities, educational institutions, hospitals, and medical institutions. By addressing the challenges in reporting substantial contributions, relatives, and concerns, this circular aims to enhance transparency and compliance in the taxation process. Taxpayers, auditors, and institutions subject to these provisions should carefully review and implement these clarifications to ensure accurate reporting and adherence to tax regulations.

SECTION 4 OF THE INCOME-TAX ACT, 1961 – INCOME – CONCEPT OF REAL INCOMEFirm/partner, in case of : Where assessment in case of assessee, a partner in firm was sought to be reopened on ground that assessee had not offered ‘interest on capital’ and ‘remuneration’ alleged to have been received from partnership firm as income, however, perusal of partnership deed indicated that interest and remuneration was not to be paid to partners mandatorily there was no material on record to indicate that, assessee had actually received any interest on capital and remuneration from partnership firm, reopening was unjustified – Artiben Amishkumar Patel v. Income-tax Offcer – [2023] 225 (Gujarat)

SECTION 11 OF THE INCOME-TAX ACT, 1961 – CHARITABLE OR RELIGIOUS TRUST – EXEMPTION OF INCOME FROM PROPERTY HELD UNDERAccumulation of income : Where assessee-trust filed Form No. 10B alongwith original return and filed Form 10 belatedly alongwith revised return, since accumulated amount was deposited in bank as per provisions of section 11(5) and Form No. 10B certified amount of accumulation, substantial compliance of Form 10 would suffice and, therefore, assessee was to be granted benefit of exemption under section 11 -Sorthiya Ahir Gnatino Utaro v. ADIT (CPC) – [2023] 662 (Rajkot – Trib.)

You can accomplish by kindness what you cannot by force.

– Publilius Syrus

IMPACT ASSESSMENT & ITS FAQ.

By Adv. Hemant Gandhi & CA Premal Gandhi |

|

On January 22, 2021, the Ministry of Corporate Affairs amended the earlier CSR Rules of 2014 and notified the Companies (Corporate Social Responsibility Policy) Amendment Rules 2021, to make impact assessment mandatory for companies undertaking CSR activities and CSR expenditure above a specified threshold. The move aims to create accurate parameters in assessing the impact of CSR activities by shifting the focus from expenditure alone to impact assessment and improve the quality of CSR projects while enhancing accountability and transparency.

The answers to some of the most frequently asked questions (FAQs) about impact assessment:

Q1. What is the need for impact assessment?

Impact assessments help funders, grant-makers and companies to understand and evaluate the impact of their social investments in programmes and projects on their target beneficiaries or society. The findings of an assessment also help funders and companies to make evidence-based decisions in implementation and identify hurdles, allowing for programme continuity, scale, sustainability, efficiency, etc.

Q2. Do all companies need to conduct impact assessments?

According to the January 2021 amendment, impact assessment is mandatory for companies with a CSR budget of INR 10 crore or more in any fiscal year and all projects with outlays of INR 1 crore or more. These impact assessments must be undertaken by an independent agency.

However, it is suggested as best practise that impact assessment be undertaken for all projects as standard procedure,. Especially long-term projects.

Q3. According to the new amendment, when must companies undertake impact assessments?

At least one year after programme implementation is complete.

Q4. If a company has a multi-year project, should the impact assessment be carried out after completion of the project?

Yes. As per Rule No. 8, if companies have multi-year programmes (say 3 years), impact assessment needs to be conducted after completion of three years of the programme. Additionally, a follow up assessment needs to be conducted one year after the completion of the programme to better understand the programme’s after effects.

However, if programmes are renewed or scaled up after each financial year, they would be treated as individual single year programmes, and separate impact assessments should be taken up every year.

Q5. Who can conduct an impact assessment?

Companies or their CSR initiatives cannot conduct impact assessments (self assessment) on their own. An independent agency must be engaged for the assessment.

Q6. Is there a limit on the expense for undertaking impact assessment?

Yes, impact assessment related expenditure may be booked as a CSR expense as long as it does not exceed 5% of the total CSR spending or INR 50,00,000, whichever is less.

Q7. Is the limit applicable on the entire CSR budget or per project?

The limit is applicable on the total CSR budget of the financial year.

Q8. Will the cost for researchers/consultants/agencies be counted as part of the INR 50 lakh or 5% limit or can the spending be accounted for outside that?

Under the amended rules, “Administrative overheads” will now mean expenses incurred by the company for ‘general management and administration’ of Corporate Social Responsibility functions in the company but shall not include the expenses directly incurred for the designing, implementation, monitoring, and evaluation of a particular Corporate Social Responsibility project or programme.

Further, a Company undertaking impact assessment may book the expenditure towards Corporate Social Responsibility for that financial year, which shall not exceed five percent of the total CSR expenditure for that financial year or fifty lakh rupees, whichever is less.

Thus, in our opinion, cost for researchers/consulting is neither part of the INR 50 lakh cap, nor the 5% cap on Admin expenditure.

Q9. Can a project conduct impact assessment prior to completion of one year (short duration project) or should it wait for one year? If done earlier, would it be counted as part of the compliance?

The project should have completed at least one year. If it is an on-going project of three years, it would make sense to study impact only on completion of three years.

You will not be remembered for what you do or did once in a way, but for what you do and did all the time. Consistency is hallmark of greatness.

PROTECT YOUR HOME…Compiled By By Mr. Tushar P. Joshi |

|

Recently during Diwali due to Fire Cracker at many society incidents of fire took place.

Friends we invest our Life Time Saving in buying house but don’t care to protect it.

We are very optimistic and believe that “Nothing is going to happen to us”. Though a chance of incidents is very low but the severity of loss is huge.

It is observed that public memory is very short, once the disasters happen in few years they keep insurance on a back seat.

Excess use of Home automation in High Rise Buildings plus use of gadgets and appliances have increased the risk of fire, it may be due to short circuit. As increased use of Electronics load on power and ultimately lead to fire.

Many times we think we have sprinklers fitted so there is no issue, but we don’t understand that if sprinklers are activated due to fire and it damages Electronics and Furniture etc. to the large extent.

While insuring the property you have to insure the value of the structure and not the Market Value of the Property, calculate the cost of reconstruction.

For covering the contents it is advisable to prepare the list of items head wise along with the value i.e. Electronics items, Furniture, House hold appliances, etc. If you wish to cover the paintings or Antiques the Valuation report for the same is to be obtained from the certified valuer.

There are certain exclusions under which policy will not pay the claim amount like

- Deliberate Damage by the owner

- Any contents kept outside the house

- If it’s illegal or unauthorized construction and any demolition done as per the court order, or by local authorities.

- Many people give their 2nd house on Rent or Lease it is considered as commercial use so any claim under home insurance will not be entertained.

It is always, advisable to consult reputed advisor before taking any insurance. Which will help you in long run.

We become what we think about.

– Earl Nightingale

It is the work that matters, not the applause.

– Robert Falcon Scott

“Wishing our members a very HAPPY BIRTHDAY!!”

| Members Name | Date of Birth |

| Rathi Bimal V. | 14-December |

| Bade Kiran K | 14-December |

| Satra Dhaval Shantilal | 14-December |

| Bapat Ujwal S | 14-December |

| Sadhria Sham Sudhamchand | 14-December |

| Kenkre Gaurav Santosh | 15-December |

| Gadkari Kishor Shankarao | 16,December |

| Chudgar Abdulrazzq M. | 16-December |

| Desai Mitul Ramanlal | 16-December |

| Joshi Kailash Ramesh | 16-December |

| Sachdev Bharat Muljibhai | 17-December |

| Soni Alkesh Pukhraj | 17-December |

| Gupta Nayan Aman | 18-December |

| Sejpal Nehal Amrutlal | 19-December |

| Dhure Prajakta M | 20,December |

| Mujawar Nihal Ahamed | 20-December |

| Doshi Bhalesh Bhupatlal | 21-December |

| Ahmed Waseem Akhtar Jameel | 21-December |

| Sakhalkar Ramesh Ashok | 22-December |

| Shah Kamlesh Ratilal | 23-December |

| Chavan Omkar Prakash | 23-December |

| Shah Haresh N | 24-December |

| Sarang Ashok Chandrakant | 24-December |

| Maideo Vikas Mohan | 24-December |

| Chavan Anil Ramrao | 24-December |

| Singhal Narendra K | 24-December |

| Kshatriya Pradip D | 25-December |

| Tanna Rasik Amritlal | 26-December |

| Ajmera Nishit Kirtikant | 26-December |

| Apte Dilip Chandrakant | 26-December |

| Chokhani Sushil H | 27-December |

| Dhumal Rajendra Dagadu | 27-December |

| Gandhi Karan Kishor | 27-December |

| Thakar Chandrakant B | 28-December |

| Sabharanjak Nikhil Diwakar | 28-December |

| Karani Chintan Keshavji | 28-December |

| Anthony John Rajshekhar | 29-December |

| Dhanak Vijay M | 29-December |

| Atre Charudatta P. | 29-December |

| Shah Paunil Sunil | 29-December |

| Dandekar Sunil Yashwant | 30-December |

| Godbole Sameer Jagannath | 30-December |

| Jain Rakesh Ratilal | 30-December |

| Naik Jasmin Pranubhai | 31-December |

| Mithbavkar Sanjay Govind | 31-December |

| Ponnaiah Murugan | 31-December |

| Bedekar Dinar Suhas | 31-December |

| Narayankar Ganesh Kaluji | 31-December |

| Ellie Karlton Anthony | 31-December |

| Chhallani Mahavirchand L | 01- January |

| Khandelwal Vijay | 01- January |

| Doshi Rajesh H | 01- January |

| Gupta Ramchandra Chunnilal | 01- January |

| Amate Sanjay B | 01- January |

| Khan Shaukatali Nazeer | 01- January |

| Padoor Ajaykumar Balan | 01- January |

| Nikam Rajendra K | 01- January |

| Baig Naushad Vaish. | 01- January |

| Kadam Sudarshan Sadashiv | 01- January |

| Mohite Umesh Mohanrao | 01- January |

| Pandey Santosh Lalmani | 01- January |

| Chopra Sushil Jasraj | 01- January |

| Gandhi Sachin Ramesh | 01- January |

| Kubadia Bhavik A | 01- January |

| Shaikh Mohammad Raiyanabul Faiz | 01- January |

| Jain Mukeshkumar Jaswantraj | 02- January |

| Shirsat Rajesh Ramakant | 02- January |

| Solanki Kashyap Phoolchand | 02- January |

| Agrawal Tarun Ratan | 02- January |

| Kothari Dipesh Balchand | 02- January |

| Soman Bipin Sanjay | 02- January |

| Kukreja Rajesh Gulabsingh | 03- January |

| Barchha Prital M. | 03- January |

| Gala Dinesh Nanjibhai | 04- January |

| Rathi Girish Jethalal | 04- January |

| Dubbewar Ashok Bhaskarrao | 04- January |

| Shah Sejal Manish | 04- January |

| Anajwala S. A. | 05- January |

| Nayak Deepak Padmanabh | 05- January |

| Gole Rajaram Shankar | 05- January |

| Sapte C. D | 05- January |

| Mehta Bhavin Jatin | 05- January |

| Kawale Nagesh Chandrashekhar | 06- January |

| Shah Raman Shamjibhai | 06- January |

| Deshpande Ratnakar Dattatraya | 07- January |

| Kulkarni Abhay Bapurao | 07- January |

| Bhosale Kiran Anandrao | 07- January |

| Dedhia Avani Navin | 07- January |

| Bambaras S. V. | 08- January |

| Bargir Shafik Gulab | 08- January |

| Shah Kivant I | 08- January |

| Shaikh Moizahmed Noorahmed | 08- January |

| Mehta Ritesh Rajesh | 08- January |

| Kadam Mangesh Tulsidas | 08- January |

| Agarwal Rakesh Omprakash | 09- January |

OUR PUBLICATIONS AVAILABLE FOR SALE

| Sr. No. | Name | Price ₹ |

| 1 | FMCG & Pharmaceutical Industry – GST Issues & Challenges | 150/- |

| 2 | Transitional Provision | 50/- |

| 3 | 46th RRC Book | 175/- |

| 4 | Referencer 2022-23 | 375/- |

| 5 | Referencer 2023-24 | 750/- |

| 6 | Mega Full Day Seminar Booklet 2.7.2022 | 130/- |

| 7 | Half Day Seminar Booklet 17.11.2022 | 100/- |

| 8 | Maharashtra Goods & Service Tax Act along with Rules (MGST Bare Act) | 850/- |

| 9 | Short Publication GST practical guides (5 Book Series) | 555/- |

| 10 | 47th RRC Book | 250/- |

| 11 | Charitable Trusts | 300/- |

Payment Link for Publication on sales : https://www.gstpam.org/online/purchase-publication.php

GSTPAM News Bulletin Committee for Year 2023-24

Pradip Kapadia Chairman |

Aloke R. Singh Convenor |

Ashish Ruparelia Jt. Convenor |