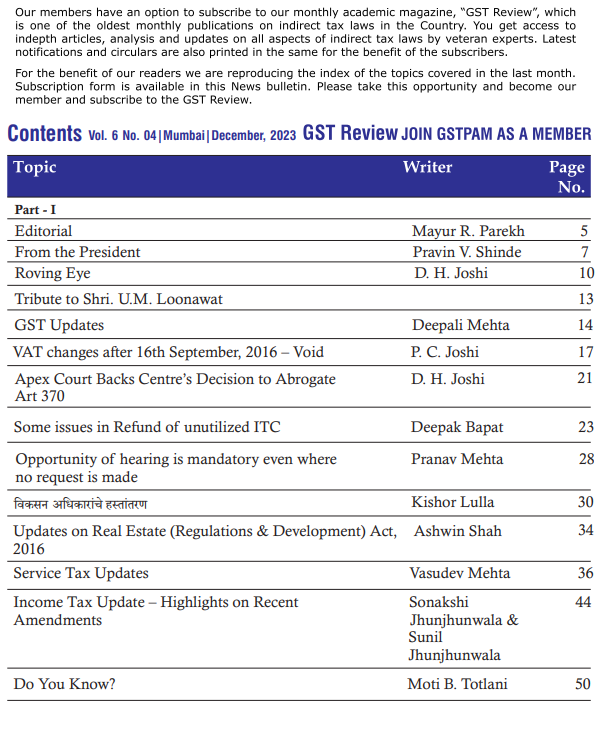

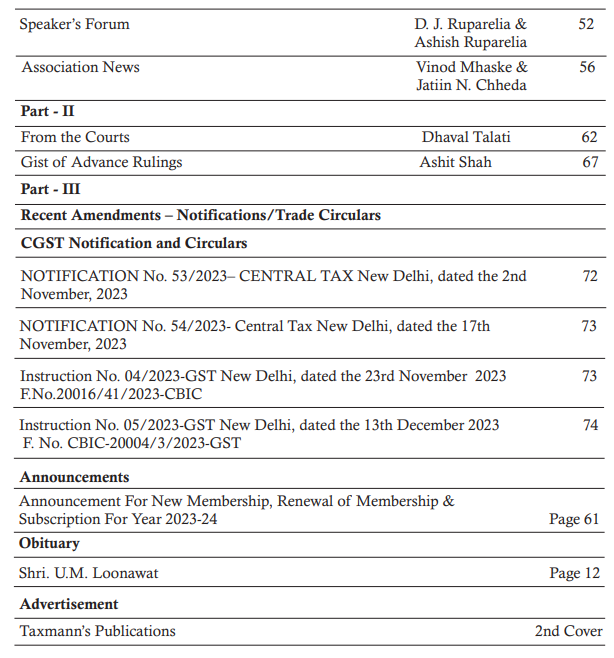

GSTPAM News Bulletin January 2024

CIRCULAR FOR RENEWAL OF MEMBERSHIP/SUBSCRIPTION CHARGES FOR THE F.Y. 2023-24

Dear Members,

RENEWAL OF MEMBERSHIP FOR F.Y. 2023-24

The Membership Fees for the year 2023-24 are due for renewal on 01.04.2023. We appreciate your Continuing support and participation in the activities of our Association.

The timely Renewal of Membership will enable the members to continuously receive the updates on various activities of GSTPAM along with the GSTReview, News Bulletin, Circulars, Messages, Webinars and online access to the website www.gstpam.org.The Life Members only need to renew the subscription charges for the GST Review. The members can also avail the benefit of discount by paying advance for subsequent two years membership fees /subscriptioncharges.

The Membership Renewal Fees received after 30th April, 2023 will be subject to approval of the Managing Committee. If the Renewal fees for a particular year are not paid, then the member is liable to pay Admission Fees again for Renewal in the subsequent year.

Delayed Renewal Members will be provided Pre Renewal GST Review subject to availability upon payment of such additional courier charges.

The details of Membership/Subscription Fees are given below for your ready reference

| Type of Membership | Membership Fees incl. GST | Admission Fees Incl.GST | Subscription Charges for GST Review | Total |

|

New Membership Application |

||||

| Donor Member | 24,780.00 | – | 600.00 | 25,380.00 |

| Patron Member | 17,700.00 | – | 600.00 | 18,300.00 |

| Life Member | 11,800.00 | 944.00 | 600.00 | 13,344.00 |

| Life Member (Conversion from Ordinary) | 11,800.00 | 590.00 | 600.00 | 12,990.00 |

| Ordinary Local Member | 1,770.00 | 590.00 | – | 2,365.00 |

| Ordinary Outstation Member | 1,475.00 | 590.00 | – | 2,065.00 |

New Membership Application (Firm/LLP)

| Ordinary Local Member | 1,770.00 | 944.00 | 0 | 2,174.00 |

| Ordinary Outstation Member | 1,475.00 | 944.00 | 0 | 2,419.00 |

| Patron Member | 17,700.00 | 0 | 600.00 | 18,300.00 |

| Donor Member | 24,780.00 | 0 | 600.00 | 25,380.00 |

Advance Membership/ Subscription charges for subsequent two years 2024-25& 2025-26 (Non-Refundable)

| Ordinary Local Member | 3,186.00 | – | – | 3,186.00 |

| Ordinary Outstation Member | 2,665.00 | – | – | 2,665.00 |

| Life Member (Individual/Firm/LLP) | 0 | – | 1200.00 | 1,200.00 |

| Patron Member | 0 | – | 1200.00 | 1,200.00 |

| Donor Member | 0 | – | 1200.00 | 1,200.00 |

Subscription for GST Review for F.Y. 2023-24 by Non-Members

| Subscription fees for GSTR | – | – | 1000.00 | 1,000.00 |

Advance Membership / Subscription charges for subsequent two years 2024-25& 2025-26 (Non-Refundable)

| Subscription Fees -GSTR | 0 | – | 2000.00 2,000.00 |

Modes of Payment:-

| Cheque | A/c Payee Cheque drawn in favor of “The Goods & Services Tax Practitioners’ Association of Maharashtra” payable at Mumbai. |

| NEFT Details | The Goods & Services Tax Practitioners’ Association of Maharashtra

Bank of India, Mazgaon Branch Current Account No. 007020100001816, IFSC Code – BKID0000070. Online generated transaction Acknowledgement should be sent by email on [email protected] along with membership and payment details Members are requested to send their physical form to the association for Approval, Issuance and Office record. |

| Cash | Renewal form along with requisite amount will be accepted between 10.30 a.m. and 5.30 p.m. on all working days except Saturday at our Office at

Mazgaon Library – Mazgoan: 1stFloor, 104, GST Bhavan, Mazgaon, Mumbai – 400 010 Or Bandra Library – GST Bhavan, Ground Floor, A Wing, Bandra Kurla Complex, Bandra (East), Mumbai – 400 051. Or Mazgaon Tower-8 & 9, Mazgaon Tower, 21, Mhatar Pakhadi Road, Mazgaon, Mumbai – 400 010. |

| Identity

(New Members) |

New Members should provide the following as Identity Proof : PAN, Aadhar Card, Constitution Document.

Address Proof(any one) : Electricity Bill / Passport/ Aadhar Card / Driving License/ Voter id/ Ration Card along with Membership Form |

| Identity Card (For Renewals) | Ordinary Local/Outstation Members should provide Two Photographs along with the Renewal Form for issue of I- cards. |

| Online Payment Link | Members can make online payment on our website www.gstpam.org. Members are requested to download Members Renewal form from website.Update the latest details in the form, scan it and mail at email [email protected]

Payment Link : https://www.gstpam.org/online/renew-membership.php If you are login first time? Click here for create your password |

We value your continuation of the membership and look forward to your renewal to this effect.

Dated:- 21.07.2023

Vinod Mhaske

Jatin Chheda

Hon. Jt.Secretary

|

Guidance Cell Email ID for queries Members can send their queries at [email protected] |

ORDER FORM FOR GSTPAM REFERENCER 2023-24

(Members are requested to take out the photocopy of the Order Form for booking)

To

The Convenor,

GSTPAM Referencer Committee

The Goods & Services Tax Practitioners’ Association of Maharashtra

Room No. 8 & 9, Mazgaon Tower, Mhatar Pakhadi Road,

Mazgaon,

Mumbai

Dear Sir,

Please book my/our order of GSTPAM Referencer for the year 2023-24 as given below.

| Sr. | Particulars | Price per copy if booked prior to 15th July 2023 | Price per copy if booked afterto 15th July 2023 | Qty | Total RS. |

| 1 | GSTPAM Referencer 2023-24 Part I & II

(GST, VAT & Allied Law Referencer & Updated GST Rate schedules). |

700 | 750 | ||

| 2 | Courier Charges (For Outstation members only) (per set) | 130 | 130 | ||

| 3 | Courier Charges (For Local members only) (per set) | 100 | 100 |

Note :

- Referencer will be published in Part I & II (for GST, VAT & Allied Laws Referencer & Updated GST rate schedules).

- Applicants requiring more than 5 copies of the Referencer are required to give a request on their letter head along with the order form. Tax Practitioner’s Associations can place order in bulk quantity by making request on their letterhead signed by the Association’s President and Secretary.

- Applicants will be issued receipt at the time of placing of their order. Applicants are requested to bring receipt at the time of taking the delivery of the Referencer. No delivery of the Referencer shall be given, unless the receipt for payment is submitted at the counter. If the receipt for payment is lost, than no delivery of the Referencer shall be given.

The payment for the above order of……………………………………………………………………….… (Rupees in words) is made herewith by Cash /Card /Cheque /Demand Draft No. ………….……dated ……….……. drawn on……………………………………………… Bank…………….. Branch, Mumbai.

Signature …………………………….

Membership Number………………………….. Address.…………………………………………………

Name ……………………………………… …………………………………………………………………

……………………………………………… …………………………………………………………………

Office Tel No…………………………………… Residence Tel No………………………………………

E-mail: …………………………………………. Mobile No.…………………………………………….

PROVISIONAL RECEIPT

Received with thanks payment of. ………………… from…………………………………… vide Cash /Card /Cheque /NEFT/Demand Draft No. …………………………. Date ………………. drawn on…………………………………………………Bank Branch, Mumbai.

Signature ……………………………

Date…………………………………. Name of staff of GSTPAM……………………

Note:

- * Please fill in all the details in the above form and send the same to the GSTPAM’s office at Tower or at Mazgaon library along with requisite payment. For Direct Deposit / NEFT payment –

- * Bank of India, Mazgaon – Account No. 007020100001817, IFSC Code – BKID0000070. Acknowledgement of the same should be sent by email: [email protected] along with duly filled form.

- * Please mention your name and membership number on the reverse side of the Cheque / Demand Draft.

- * The counter timings are from 10.30 a.m. to 5.30 p.m. on Monday to Friday.

- * The Cheque / DD should be drawn in the name of “THE GOODS AND SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

48th RESIDENTIAL REFRESHER COURSE

Hotel Novotel, At Visakhapatnam

Thursday 29th February, 2024 to Sunday 3rd March,2024

The Residential Refresher Course Committee is pleased to announce its 48th Residential Refresher Course (RRC) on GST at Visakhapatnam, the port city and Industrial Centre in the State of Andhra Pradesh on the Bay of Bengal. The City is famous for its Port, Beautiful Beaches, caves, ancient Buddhist sites and the eastern ghats as well as wild life sanctuaries. It is also know as Vizag and nick named as the “City of Destiny” and the “Jewel of the East Course”.

The object of RRC is to share the essence of professional experience and expertise of the faculties they have gained over the years and where members can study in afresh at mosphere and rejuvenate.

The topics selected for RRC will cover an in-depth and practical understanding of GST Law and the challenges faced in the GST Era. In addition, the Delegates can seek views from seniors on issues they face regarding the interpretation of the law and practical difficulties. These topics are of immense importance and will help professionals/Delegates handling Indirect Tax Matters.

Along with studies, we have planned to visit various tourist places such as local sightseeing in Visakhapatnam which Includes Submarine Museum, Air Craft Museum, Kailasagiri. Simhachalam Temple, Beautifull beaches and many more.

Dates: Thursday 29th February, 2024 to Sunday 3rd March, 2024.

Venue: Hotel Novotel Varun Beach

Dr NTR Beach Rd, Krishna Nagar, Visakhapatnam, Andhra Pradesh 530002 The RRC includes 3 Nights–4 Days accommodation on double occupancy basis and the course material. The Package will start from Lunch on 29th February, 2024 and end with breakfast on 3rd March, 2024.The Paper at the RRC are as under:

| Paper | Topics | Paper Writer | Chairman |

| Paper 1 | Cross Border Transactions – Export,Import, Bond Transfer, Out to Out Transactions | CA Deepali Mehta | Eminent Faculty |

| Paper 2 | Interest, Penalties and offences under GST | CA Aloke Singh | Eminent Faculty |

| Paper 3 | Insights and How to deal with various Parameters of ASMT-10 | Adv. Amol Mane | Eminent Faculty |

| Brains’ Trust Session | Eminent Faculties |

The enrollment Fees are as under:

| Enrollment Fees | Amount | GST18% |

Total |

|

|

DELEGATE FEES FOR MEMBERS |

||||

| 1 | Fees Paid on or Before 14/12/2023 | Rs.19,500/- | Rs.3,510/- | Rs.23,010/- |

| 2 | Fees Paid After 15/12/2023 | Rs.21,000/- | Rs.3,780/- | Rs.24,780/- |

| 2 | Child rates (With Extra Bed)

*Age 6-12 years Sharing room with parents |

Rs.11,000/- | Rs.1,980/- | Rs.12,980/- |

|

DELEGATE FEES FOR NON- MEMBERS |

||||

| 1 | Fees Paid on or Before 14/12/2023 | Rs.21,000/- | Rs.3,780/- | Rs.24,780/- |

| 2 | Fees Paid After 15/12/2023 | Rs.22,500/- | Rs.4,050/- | Rs.26,550/- |

| 2 | Child rates (With Extra Bed)

*Age 6-12 years Sharing room with parents |

Rs.11,000/- | Rs.1,980/- | Rs.12,980/- |

Notes:-

- In case of cancellation, the refund will be at the discretion of the RRC Committee, the same shall be refunded after completion of event.

- Hotel Check-in Time is 02.00 PM, and Check out Time is 12.00 PM. Early Check-In and Late Checkout will be subject to availability.

- Delegates joining late or leaving early in RRC should inform the Convenor / Office Bearers well in advance.

- All delegates are requested to carry their AADHAR, Driving License, Election Card, and Passport for Photo & Address identification (Any Two) for Train or Air Travel. In addition, members are requested to send a Xerox copy of his/her photo ID with address proof along with Enrollment Form.

- Delegates are advised to carry their medical kit with them.

- Room Service and items other than provided for in the Hotel package will have to be paid Directly in Cash separately by the Delegates to the hotel.

- Tea/Coffeemakers are placed for consumption in all the rooms.

- Delegates are strictly requested to deposit room keys at the reception counter on leaving.

- Please carry our water bottles during Sightseeing Program.

- Members are requested to keep their Identity Cards Compulsory during all Sightseeing programs.

- Allotment of Room shall be at the sole discretion of the RRC Committee only. Any changes required in the program will be at the sole discretion of the RRC Committee.

- We request all Delegates to get themselves fully vaccinated as per the directions of the Government of India and carry their copies of their final certificates as issued.

- Members who enroll for RRC have to renew their Membership for the year 2023-24 before registering for the event; otherwise, they will be treated as Non-Member.

We Wish You All Good Luck in Study at RRC

The Goods &Services Tax Practitioners’ Association of Maharashtra

| Pravin V. Shinde

President |

Sachin Gandhi

Chairman |

Dilip Nathani

Convenor |

Premal Gandhi & Ajay Talreja

Jt. Convenor |

| 9821482020 | 9821121433 | 9324383636/ 9820013469 |

Suggested Train Details from Mumbai to Visakhapatnam on 28th February, 2024

| From | To | Train

Number |

NAME | Departure

Time |

Arrival

Time |

| LTT

Mumbai |

Visakhapatnam | 18520 | Visakhapatnam Express | 6:55

(Wednesday) |

10:40

(Thursday) |

Train Details from Visakhapatnam to Mumbai on 3rd March, 2024.

| From | To | Train

Number |

NAME | Departure

Time |

Arrival

Time |

| Visakhapatnam | LTT Mumbai | 22847 | Vskp Ltt S F | 8:20 AM

(Sunday) |

1:00 PM

(Monday) |

| Visakhapatnam | LTT Mumbai | 18519 | Vskp Ltt Express | 11:20 PM

(Sunday) |

4:15 AM

(Tue) |

Suggested Flight Details from Mumbai to Visakhapatnam on 29th February, 2024.

| From | To | Flight Number | Airline

Name |

Departure

Time |

Arrival

Time |

| Mumbai | Visakhapatnam | 6E 5107, 6E 581

(Via Chennai) |

Indigo Airlines | 7:00 | 11:45 |

| Mumbai | Visakhapatnam | 6E 5246, 6E 879

( Via Hyderabad) |

Indigo Airlines | 8:00 | 11:50 |

| Mumbai | Visakhapatnam | 6E 5352, 6E 6336

(Via Bengaluru) |

Indigo Airlines | 6:05 | 13:55 |

| Mumbai | Visakhapatnam | 6E 5296, 6E 6336

(Via Bengaluru) |

Indigo Airlines | 7:30 | 13:55 |

Suggested Flight Details from Visakhapatnam to Mumbai on 3rd March, 2024.

| From | To | Flight Number | Airline

Name |

Departure

Time |

Arrival

Time |

| Visakhapatnam | Mumbai | AI 654 | Air India | 15:50 | 18:05 |

| Visakhapatnam | Mumbai | 6E 5247 | Indigo | 15:10 | 17:15 |

| Visakhapatnam | Mumbai | I5 1529, I5 1782

(Via Bengaluru) |

Air Asia | 11:00 | 15:50 |

| Visakhapatnam | Mumbai | 6E 5309, 6E 5255

(Via Bengaluru) |

Indigo | 14:35 | 19:50 |

ENROLMENT FORM for

48th RESIDENTIAL REFRESHER COURSE Hotel Novotel, At Visakhapatnam

Thursday 29th February, 2024 to Sunday 3rd March, 2024

To,

The Convenor,

Residential Refresher Course Committee,

The Goods and Services Tax Practitioners’ Association of Maharashtra,

8 & 9, Mazgaon Tower, 21, Mhatar Pakhadi Road,

Mazgaon, Mumbai-400 010.

Dear Sir,

Kindly enroll me /us as the delegate(s) for the 48 th RRC to be held Hotel Novotel, at Visakhapatnam between Thursday 29th February, 2024 to Sunday 3rd March, 2024. My relevant details are as under

- * NAME ……………………………………………………………………………………… (Age:…….yrs.)

- * ADDRESS……………………………………………………………………………………………………………………………………………………………………………………………………………..

- * GSTIN…………………………..………….…..………………………………………………………………..

- * GSTPAM Membership No……………….…………………………………………………………………….

- * Telephone (O)………………………………®……………………………………………………………………..

- * Email:…………………………………………………………………………………………………………………………….

- * Mobile……………………………………………………………………………………………………………………………

- * Food preference Veg Non-veg

- * Whether Jain food is required Yes No

- * If joining with family, please fill in the following details:

- Name of Spouse:……………………………………………… (Age……… yrs.)

- Name of Child/Children: (i) ……………………………………(Age………. yrs.)(ii) ……………………………………(Age …………………….yrs.)

- * My preference of Room Partner (in case of not accompanied by a family member)

………….………………………………………………………………………………………………….

(Signature)

Delegate Fees:

The fees include 3 Nights – 4 Days accommodation with the course material. The enrollment Fees are as under:

| Enrollment Fees | Amount | GST18% | Total | |

|

DELEGATE FEES FOR MEMBERS |

||||

| 1 | Fees Paid on or Before 14/12/2023 | Rs.19,500/- | Rs.3,510/- | Rs.23,010/- |

| 2 | Fees Paid After 15/12/2023 | Rs.21,000/- | Rs.3,780/- | Rs.24,780/- |

| 3 | Child rates (With Extra Bed)

*Age 6-12 years Sharing room with parents |

Rs.11,000/- | Rs.1,980/- | Rs.12,980/- |

|

DELEGATE FEES FOR NON- MEMBERS |

||||

| 1 | Fees Paid on or Before 14/12/2023 | Rs.21,000/- | Rs.3,780/- | Rs.24,780/- |

| 2 | Fees Paid After 15/12/2023 | Rs.22,500/- | Rs.4,050/- | Rs.26,550/- |

| 3 | Child rates (With Extra Bed)

*Age 6-12 years Sharing room with parents |

Rs.11,000/- | Rs.1,980/- | Rs.12,980/- |

Member means a member of The Goods and Services Tax Practitioners’ Association of Maharashtra along with his/her Spouse and Children only. A member who enrolls for RRC has to renew the Membership for 2023-2024 before enrolling for the event.

Details of Payment

Cheque/ D.D.No……..………………… Bank……………………..…………………………..……. Branch…………….……… Dated……………………… NEFT details ….………………………………….

Bank details of GSTPAM are as under:

Bank:- Bank of India

Name:- The Goods & Services Tax Practitioners’ Association of Maharashtra

Branch:- Mazgaon, Mumbai

A/c No. :- 007020100001816 – Current A/c

IFSC Code :- BKID0000070

Notes:-

- Acknowledgment generated through online transactions should be emailed to [email protected] along with Enrollment Form and payment details.

- Online Payment Link: https://www.gstpam.org/online/event-registration.php

- Please issue the Cheque in favour of ‘‘The Goods & Services Tax Practitioners’ Association of Maharashtra’’ (FULL NAME IS REQUIRED TO BE STATED ON THE CHEQUE AS PER RBI DIRECTION).

- Please tick/fill in the appropriate boxes.

- All delegates are requested to attach a xerox copy of his / her photo ID with addressproof.

- Booking for RRC will be accepted and confirmed only on payment of full delegate fees.

- Please attach your Travels details with the enrollment form and email to [email protected]

CIRCULAR FOR 41ST BATCH OF GST BEGINNERS COACHING CLASS FOR THE YEAR 2023-24

Dear Members,

We are happy to announce that “41st Batch of GST Beginners Coaching Classes” will commence on 15th January, 2024 in Hybrid mode.

Details of Coaching Class are as under

Virtual : Zoom Platform

Enrollment Fee : Rs.1950/- (Incl GST) for all participants

Salient Features of the Coaching Class:

- The object of the Coaching Class is to train and groom the new entrants or would be entrants in Indirect Taxes Practice particularly in GST in a very professional manner. Our well known seniors not only teach what is written in the books but also share the essence of their professional experience which they have gained over the years. This can be of enormous help and use to the new entrants. Here, students not only get knowledge but also wisdom by interacting with the seniors.

- Our expert faculties will provide notes on the respective topics.

- It has been now more than 6 years of implementation of GST, the classes will help the member and students to solve their doubt.

- The classes would be conducted, having “Twenty Four” Coaching Sessions. Also, the participants would be given case studies for the practical experience.

The “Coaching Class” of our Association is one of the best places where the subject of GST can be learnt in a very professional manner. Our Coaching Classes are so popular that apart from new entrants, many members who are not new, but whose craving for perpetual learning is very strong, enroll every year. You are, therefore, requested to enroll yourself or send your juniors and/or staff members without fail and enroll them at the earliest to avoid disappointment.

The enrollment form can be obtained from the Mazgaon Library or can be downloaded from GSTPAM’s website at www.gstpam.org

Thanking you,

Yours faithfully,

| Pravin V. Shinde | Jatin Chheda | Haresh Chhugani | Vivekanand Rao, Chaitanya Vaidya & |

| Ashwin Shivnani | |||

| President | Chairman | Convenor | Joint Convenors |

For further details, please visit www.gstpam.org or contact:

Mr. Jatin Chheda, Chairman & Hon. Jt. Secretary (Mob. No.: 9821669090)

Mr. Haresh Chhugani, Convenor ( Mob. No. 9820268035)

Mr. Ashwin Shivnani, Jt. Convenor ( Mob. No. 9819897488)

Mr. Vivekanand Rao, Jt. Convenor ( Mob. No. 9820036040)

Mr. Chaitanya Vaidya, Jt. Convenor ( Mob. No. 9511291003)

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

ENROLMENT FORM FOR

41st Batch of GST Beginners Coaching Classes

| Virtual | :– | Zoom Platform |

| Enrolment Fee | : | Rs. 1,950/- (Inclusive 18% GST) for all participants. |

| Date | : | Monday, 15th January, 2024, onwards |

Name of the participant

…………………………………………………………………………………………………………….

GSTPAM Membership Number……………………..

GSTTIN of Member……………………………………

Address

……………………………………………………………………………………………………………………..

Telephone: (O)………………..…………….. ® ………………………..

E-mail …………………………………………… Mobile No. ………………………..

Amount: Rs. ……………………………………. Cheque No. …………………………

Bank……………………………………………… Branch ……..…………………..

Dated………………………

Participant Details:

E-mail …………………………………………… Mobile No.…………………………

Whats app No. …………………………………….

Signature …………………….

Notes:

- Cheque/D.D. should be drawn in favour of the “The Goods & Services Tax Practitioners’ Association of Maharashtra” payable at Mumbai.

- The enrollment form along with Cheque / DD/ Cash should be submitted at Room No. 104, GST Bhavan , Mazgoan, Mumbai 400 010.

- Payment Link : https://www.gstpam.org/online/event-registration.php

- NEFT detail – Bank of India, Mazgaon Branch – Account No. 007020100001816, IFSC Code – BKID0000070

- Acknowledgement generated through online transaction should be emailed [email protected] along with Enrolment Form and payment details

- Participant’s Email id & Mobile No. shall be used for schedule communication

- Kindly carry the receipt of payment to attend the Coaching Class.

- The Association reserves the right to change and alter the schedule if required.

41st Batch of GST Beginners Coaching Classes

| Sr.

No. |

Day & Date | Session | Time | Topics | Speakers |

| 1 | Monday, 15/01/2024 | 2.00 To 2.30 | Innauguration Session | ||

| 1 | 2.30 To 4.00 | General concept of GST and legacy laws | Adv. Dinesh Tambde | ||

| 2 | 4.15 To 5.45 | Important Definitions under GST | Adv. Dinesh Tambde | ||

| 2 | Wednesday, 17/01/2024 | 3 | 2.30 To 4.00 | Over view of Registration under GST Act | CA Aalok Mehta |

| 4 | 4.15 To 5.45 | Levy and Scope of Supply under GST Act (including Exemptions under goods and Exemptions under services) | Adv. Parth Badheka | ||

| 3 | Thursday, 18/01/2024 | 5 | 2.30 To 4.00 | Time of Supply under GST | CA Hiral L. Shah |

| 6 | 4.15 To 5.45 | Value of Supply under GST | CA Raj Khona | ||

| 4 | Monday 22/01/2024 | 7 | 2.30 To 4.00 | Place of Supply of Goods under GST | Adv. Manohar Samal |

| 8 | 4.15 To 5.45 | Place of Supply of Services under GST | CA Aditya Khandelwal | ||

| 5 | Wednesday 24/01/2024 | 9 | 2.30 To 4.00 | Composite Supply and Mixed Supply | CA Aditya Seema Pradip |

| 10 | 4.15 To 5.45 | Input Tax Credit | CA Aditya Surte | ||

| 6 | Monday 29/01/2024 | 11 | 2.30 To 4.00 | Tax on Reverse Charge Mechanism basis | Mr. Balram Begari |

| 12 | 4.15 To 5.45 | Composition Schemes

(Including Taxation on Insurance Companies, Travels Agents and Forex Agents) |

Adv. Milind Bhonde | ||

| 7 | Wednesday 31/01/2024 | 13 | 2.30 To 4.00 | TDS / TCS & E-Commerce | Adv. Tanmay Mody |

| 14 | 4.15 To 5.45 | Type of Invoices, E Invoice, Credit / Debit Notes and Maintainance of Accounts | Mr. Swapnil Munot | ||

| 8 | Friday 02/02/2024 | 15 | 2.30 To 4.00 | Imports of goods and Import of services | CA R.Subramanian |

| 16 | 4.15 To 5.45 | E-Way Bill, Confiscation and detention of goods | Adv. Rahul C. Thakar | ||

| 9 | Monday 05/02/2024 | 17 | 2.30 To 4.00 | Zero Rated Supply (Export and SEZ) and other refunds | Miss. Devanshi Shah |

| 18 | 4.15 To 5.45 | Returns and Payment of tax and interest | CA Girish Kulkarni | ||

| 10 | Wednesday 07/02/2024 | 19 | 2.30 To 4.00 | Finalisation of Accounts | Shri. Sunil Joshi |

| 20 | 4.15 To 5.45 | Annual Return and Reconciliation (Form 9 & 9C) | GSTP Haresh Chhugani | ||

| 11 | Friday 09/02/2024 | 21 | 2.30 To 4.00 | Assessments, Business Audit, Penalties, Demand and Recovery of dues | CA Ashit Shah |

| 22 | 4.15 To 5.45 | Penal and Prosecution Provisions under GST | Adv. Ishan Patkar | ||

| 12 | Monday 12/02/2024 | 23 | 2.30 To 4.00 | Appeals and Advance Ruling | Adv. Pravin L. Jadhav |

| 24 | 4.15 To 5.45 | Overview of GST Website | GSTP Sachin Gandhi | ||

| 13 | Saturday 16/03/2024 | 25 | Moot Court |

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

INTENSIVE STUDY COURSE CIRCULAR FOR THE YEAR 2023-24

Respected Members,

It is 7th year of the GST act is implemented. After implementation of GST, whole fraternity of Indirect Tax Practitioners and Trade are facing various challenges with regard to implementation, transition, interpretation, practical aspects, prescribed schedule rates, AAR, Department Audit, various notices related to ITC mismatch and so on.

We all are aware about the practical difficulties we are facing while applying the rules and procedures of the GST law and the frequent amendments to the law especially due to frequent lockdown. With the view to update our fellow members on the latest development in law and to discuss the practical issues arising there from, our association has been regularly conducting Intensive Study Course. This year the Intensive Study Course is designed to enable the members to study and discuss various issues on Indirect Tax Laws mainly on GST Law, as well as on profession tax, etc.

With the same enthusiasm to discuss mainly on various aspects of GST Law, We are starting our hybrid mode Intensive Study Course for the year 2023-24 from Friday, 15-12-2023 onwards.

The Intensive Study Course is such an academic activity of our association which is designed to facilitate the members to study and discuss various issues in group. At the intensive study Course, one of the members acts as a group leader and leads the discussion on issues of the relevant subject / topic and one of the seniors in the profession monitors the discussion. The meetings are generally arranged ON Hybrid mode on 1st, 3rd and 5th Friday of the month during 3.30 p.m. to 6.00 p.m. There are around 15-16 meetings will be arranged for the Intensive Study Circle.

1st The inaugural meeting of the Intensive Study Course is scheduled to be held on Friday, 15-12-2023 between 3.30 p.m. & 6.00 p.m. on hybrid mode on the subject “Issues and Intricacies in GSTR 9 / 9C along with implications on Notices by GST Department”. The topic will be lead by Group Leader CA Dharmen Shah and the Monitor of CA Mayur Parekh.

The group strength is restricted to a limited number of members to facilitate better interaction within the group. The Intensive Study Course Fee is fixed at Rs. 1,650/- including GST for Members and Rs. 1,850/- including GST for Non members. You are requested to enroll at the earliest to avoid disappointment. Kindly use photocopy of the Enrolment form printed here in below. Also write your email address and mobile number for better communication.

Member interested to act as group leader should inform by filling up the option in the Form of “I wish to be a group leader for the subject” and are requested to contact the Convener on the mobile numbers mentioned- on Cell No. 9224386682/9821441740 / 9892512345/9870008752

Note :

- The First Meeting of the ISC is proposed to be a HYBRID meeting. The members joining the ISC are requested to fill the attached form for selection of Only Physical Mode or Only Virtual Mode. The Physical mode will be continued only if majority participants opt for the Physical Mode. (Else only Virtual meetings shall be held no Hybrid Meeting shall be held)

- GST lectures will be in form of group discussion, which will be helpful to study the GST law.

- If the materials are received 3 days earlier to the date of meeting, the same will be circulated through mails to the participants.

- Participants are requested to discuss only the points related to the particular topic of the meeting and to come prepared for the subject, which will be helpful for the discussion.

| Pranav Kapadia

Chairman |

Hiral Shah

Convenor |

Sanjay Gajra

Jt.Convenor |

Sujoy Mehta

Jt.Convenor |

Bhavin Mehta

Jt.Convenor |

| 9224386682 | 9821441740 | 9892512345 | 9870008752 |

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

ENROLMENT FORM FOR INTENSIVE STUDY COURSE CIRCULAR FOR THE

YEAR 2023-24

To,

Convener,

Intensive Study Course

The GSTPAM, Mazgaon, Mumbai – 400 010.

Dear Sir,

Please enroll me as a participant for the Intensive Study Course for the year 2023-24. The Registration fees of Rs.1,650/- (for members) / and Rs.1,850/- (for non-members) 18% Including GST is enclosed herewith by Cash /DD / Cheque No.____________dated__________drawn on_____________

Particulars of Member/Participant :

Name: _______________________________________

Educational Qualification: _______________________________________

Address for Communication: _______________________________________

Telephone No. Office :_______________________________________ Res. _______________________________________

Email ID :_______________________________________ Mob. No,____________________________

GSTPAM Membership No:___________________________________________________

GSTIN (if Applicable):______________________________________________________________

I also wish to be a group leader for the subject of ______________________________and suitable available date will be:____________________________________________

I would like to attend the Meeting (Please Tick only one option)

Only Physical Mode

Only Virtual ModeThe Physical mode will be continued only if majority participants opt for the Physical Mode

Signature _______________________

Note :-

- Please issue the Cheque in favour of ”The Goods & Services Tax Practitioners’ Association of Maharashtra” (FULL NAME IS REQUIRED TO BE STATED ON THE CHEQUE AS PER RBI DIRECTION).

- For NEFT payment – Bank of India, Mazgaon- Account No. 007020100001816, IFSC – BKID0000070. Acknowledgement generated through online transaction should be emailed on [email protected] along with Enrolment Form and payment details.

- Online Payment Link: https://www.gstpam.org/online/event-registration.php

- Outstation members are requested to make payment online payment.

- The enrollment form along with payment proof should be submitted at Room No. 104, Vikrikar Bhavan, Mazgaon, Mumbai – 400010.

- Kindly carry the receipt of payment to attend the Lecture.

- The Association reserves the right to change and alter the schedule if required.

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

ENROLMENT FORM FOR MEGA FULL DAY SEMINAR FOR THE 9 TH FEB. 2024

| Day & Date | Friday, 9th February, 2024 | |||

| Timing | 9.00 am to 5.00 pm | |||

| Topic | Recent Developments on ITC | CA Rajiv Luthia | ||

| GST implementations on discounts, incentives, warranties, etc | CA Aditya Surte

Chairman : CA Rajat Talati |

|||

| RCM on govt services including transfer of

leasehold rights, mining, BMC charges, MIDC, ROC, etc. |

CA Girish Kulkarni

Chairman : CA Deepak Thakkar |

|||

| GST litigation, concept & disputed areas | Adv. Monarch Bhatt

Chairman : Adv. Deepak Bapat |

|||

| Venue | The Mysore Association Auditorium, Near Maheshwari Udyan, Matunga (E), Mumbai-

400019. |

|||

| Enrollment Fees | Rs. 1829/- (including GST) for Members & Rs. 2006/- (including GST) for Non- Members |  |

||

Applicant Details:

| GSTPAM Membership No. : | |

| Name : | |

| Address : | |

| GSTIN of the Member : | |

| Mobile Number : | |

| Email id : | |

| Signature of Member : |

Note :-

- Please issue the Cheque in favour of ‘‘The Goods & Services Tax Practitioners’ Association of Maharashtra’’ (FULL NAME IS REQUIRED TO BE STATED ON THE CHEQUE AS PER RBI DIRECTION).

- For NEFT payment – Bank of India, Mazgaon- Account No. 007020100001816, IFSC – BKID0000070. Acknowledgement generated through online transaction should be emailed on [email protected] along with Enrolment Form and payment details.

- Online Payment Link: https://www.gstpam.org/online/event-registration.php Outstation members are requested to make payment online payment.

- The enrollment form along with payment proof should be submitted at Room No. 104, Vikrikar Bhavan, Mazgaon, Mumbai – 400010.

- Kindly carry the receipt of payment to attend the Lecture.

GST, MVAT & ALLIED LAW UPDATESCompiled by Adv. Pravin Shinde |

|

|

Notification under Central Tax |

||

| Notification No. | Date of Issue | Subject |

| 55/2023-Central Tax | 20.12.2023 | Extension of due date for filing of return in FORM GSTR-3B for the month of November, 2023 for the persons registered in certain districts of Tamil Nadu. |

| 56/2023-Central Tax | 28.12.2023 | Seeks to extend dates of specified compliances in exercise of powers under section 168A of CGST Act |

| 01/2024-Central Tax | 05.01.2024 | Extension of due date for filing of return in FORM GSTR-3B for the month of November, 2023 for the persons registered in certain districts of Tamil Nadu. |

| 02/2024-Central Tax | 05.01.2024 | Extension of due date for filing FORM GSTR-9 and FORM GSTR- 9C for the Financial Year 2022-23 for the persons registered in certain districts of Tamil Nadu. |

| 03/2024-Central Tax | 05.01.2024 | Seeks to rescind Notification No. 30/2023-CT dated 31 st July, 2023 |

| 04/2024-Central Tax | 05.01.2024 | Seeks to notify special procedure to be followed by a registered person engaged in manufacturing of certain goods. |

|

Notification under Central Tax (Rate) |

||

| Notification No. | Date of Issue | Subject |

| 01/2024-Central Tax (Rate) | 03.01.2024 | Seeks to amend Notification No 01/2017- Central Tax (Rate) dated 28.06.2017. |

|

Notification under Integrated Tax (Rate) |

||

| Notification No. | Date of Issue | Subject |

| Corrigendum | 05.01.2024 | Corrigendum to notification no 01/2024-Integrated Tax(Rate) dated 03.1.2024 |

| 01/2024-Integrated Tax (Rate) | 03.01.2024 | Seeks to amend Notification No 01/2017- Integrated Tax (Rate) dated 28.06.2017 |

|

Notification under Union Territory Tax (Rate) |

||

| Notification No. | Date of Issue | Subject |

| Corrigendum | 05.01.2024 | Corrigendum to notification no 01/2024-Integrated Tax(Rate) dated 03.1.2024 |

| 01/2024-Union Territory Tax (Rate) | 03.01.2024 | Seeks to amend Notification No 01/2017- Union Territory Tax (Rate) dated 28.06.2017. |

|

Notification / Circular Under Maharashtra Goods and Services Tax Act, 2017 (MGST) |

||

| Notification No. /

Trade Circular No |

Date of Issue | Subject |

| Notification No. 53/2023—State Tax | 28.11.2023 | Seeks to notify a special procedure for condonation of delay in filing of appeals against demand order passed untill 31st March 2023. |

| No. DC (A&R)/PWR/ JURIS-2012/2/ADM-8,

dated 11th December 2023. |

03.01.2024 | MVAT Territorial Jurisdiction to AC and STO (Mumbai) |

| MAHARASHTRA ACT NO. I OF 2024.

E.O. No.1 Dt. 03.01.2024 |

03.01.2024 | Maharashtra Goods & Services Tax (Second Amendment) Act, 2023. (Maharashtra Act No. I of 2024) (English) |

If you fail, never give up because FAIL means “First Attempt In Learning”. End is not the end, in fact END means “Effort Never Dies”. If you get No as an answer, remember N.O. means “Next Opportunity”. Be positive.

– Dr. APJ Abdul Kalam

| GIST OF TRIBUNAL JUDGEMENTS (VAT)

Compiled by CA Rupa Gami |

|

- Gaurav Agro Pipes in Rectification Application No. 05 of 2022 (in Vat Appeal No. 23 of 2016) decided on 19/12/2023

An appeal was filed before the Hon’ble Tribunal against the orders passed by Advance Ruling Authority under section 55(5) and (9) of the MVAT Act. The appeal was heard by the Second Bench, however due to difference of opinion between the two learned members, the question of law pertaining to section 55(5) was referred to the Larger Bench. The Larger Bench answered the question of law and and directed the proceedings of the appeal to be sent to the Second Bench for passing consequential orders. The issue regarding section 55(9) was taken by the Larger Bench but observed that the original Second Bench could adjudicate on the prayer under section 55(9) of the Act.The Second Bench while passing the order only considered the dispute under section 55(5) of the Act and did not adjudicate on the prayer under section 55(9) of the Act.The Learned Advocate for the petitioner submitted that the Hon’ble tribunal had fallen into error in not adjudicating the question under section 55(9) of the Act. The judgement of the co-ordinate bench of this Tribunal in the case of Ashish Enterprises was relied where it was held that it is the prerogative of the Commissioner to grant prospective effect to the order. The issue can be decided suo moto.The Hon’ble Tribunal held that “the principles of natural justice envisage that a mistake committed by the Tribunal in not noticing the facts involved in this appeal would attract the ancillary or incidental power of the Tribunal necessary to discharge its functions effectively for the purpose of doing justice between the parties and which are required to be complied with.”The Hon’ble Tribunal held it to be a fit case for granting prospective effect from the date of the Advance Ruling Order. (Petitioner represented by Adv. V. P, Patkar) - Pfizer Animal Pharma Pvt. Ltd. in Vat Second Appeal Nos. 60 and 61 of 2023 decided on 15/03/2023

The appeal is under CST Act where the appellant prays for grant of stay since an amount of 10% of tax has already been deposited. It is the appellant’s contention that the branch transfer turnover of the agent is included in his return and Form 704 which is incorrect. Therefore, the dispute is not relating to non- submission of Declaration Forms. That the provision of Section 26B(c) or (d) would be applicableThe Hon’ble Tribunal held that since the turnover of branch transfer was reflected in the returns, Form 704 and Balance Sheet, the same could not be now excluded. Also, the provisions of section 26(B) are mandatory in nature and therefore the appellant is required to deposit 100% of the tax as part payment. (Petitioner represented by Adv. V. P. Patkar) - Vinayak Trading Corporation in Vat second Appeal No. 284 of 2015 decided on 23/03/2023

The first appeal was dismissed for non-attendance. In second appeal it was submitted that the appellant was not given proper opportunity and the appeal was dismissed for non-payment. The Hon’ble tribunal held that the first appeal order was very short. Since the appeal was before the amendment ie. Section 26(B) of the MVAT Act, the appeal could not have been dismissed for the sole reason of no-payment of part payment, the first appeal authority should have made some comments about the assessment order on merits. The order was set aside and matter remanded to first appeal authority for fresh decision. (Petitioner represented by Adv. C.B.Thakar) - M/s Abbott Healthcare Pvt. Ltd. in Misc App No. 4 and 5 of 2022 in Vat Second Appeal No. 46 and 129 of 2020 decided on 08/03/2023

Miscellaneous Applications were filed by the Addl. Commr. on behalf of Revenue Department with a prayer that the Second Appeals be remanded to the assessing authority for working out the tax liability by treating the turnovers which escaped from the orders of assessment and first appeal orders as interstate sales.It was contended by the appellant that in the normal course, the assessment orders cannot be reviewed on account of bar of limitation and that the assessment cannot be reopened. The Hon’ble tribunal held that the powers conferred by section 26(5) cannot be ignored, that every appellate authority both in first and second appeal can in exercise of those powers confirm, reduce, enhance or annul the assessment. Relying on the Apex Court judgement in the case of Tel Utpadak Kendra (48 STC 248), the Hon’ble Tribunal held that the Tribunal has the power to make enhancement in the assessment, if it is found fit to do so. However, the matters cannot be remanded as the appeals were not yet heard finally for disposal and the issue of enhancement would be decided at the time of final hearing and disposal of appeals. (Petitioner represented by Adv. Sanjeev Sachdeva)

Learn everything that is good from others, but bring it in, and in your own way adsorb it; do not become others.

– Swami Vivekananda

INCOME TAX UPDATESCompiled By By Adv. Ajay Talreja |

|

Demystifying Form 10BD: A Guide to Tax-Exempt Donations

In the intricate world of income tax laws, the roles of both donors and recipients are paramount in upholding compliance and transparency. To streamline this process, the Income Tax Act introduces Form 10BD, a document of great significance to all parties involved. Charitable organizations and section 8 companies are mandated to annually furnish details of donations in Form 10BD. This article will unravel the complexities of Form 10 BD, i ts scope, applicability, and the crucial filing deadline.

What is Form 10BD of the Income Tax Act?

Form 10BD, a prescribed document under the Income Tax Act, primarily revolves around the reporting of transactions involving specific entities. These entities typically enjoy tax-exempt status or special tax treatment as defined by the law. The core purpose of this form is to meticulously monitor and scrutinize transactions between donors and recipients falling within these specified categories.

Applicability of Form 10BD: Form 10BD casts its net wide, encompassing both contributors and recipients engaged in transactions with entities qualified for tax exemptions or special tax treatment. This encompasses donations made to legally recognized nonprofit organizations, governmental bodies, and other entities that meet the stipulations laid out in the Income Tax Act. Donors are obliged to utilize Form 10BD when providing monetary or non-monetary contributions to these approved organizations. Simultaneously, recipients must adhere to Form 10BD when accepting grants or donations from such sources. This dual compliance ensures a thorough reporting process, guarding against any potential misapplication of tax- exempt funds. Exploring the

Responsibilities of Donors and Recipients:

Donors’ Responsibilities: Donors bear the responsibility of maintaining meticulous records of all their interactions with qualified entities. When contributing to a designated organization, they are mandated to complete Form 10BD, providing detailed information about their donation or grant. This includes recipient details, the donation’s magnitude, and its intended purpose.

Responsibilities of Recipients:

Recipients share the onus of complying with Form 10BD. After receiving gifts or grants from donors, they are obligated to verify the information contained within the form. It is imperative that recipients scrutinize the accuracy of the data provided and maintain their own records for future reference.

Understanding the Due Date for Filing Form 10BD: As with any tax-related document, the filing of Form 10BD must be completed within the stipulated timeframe. The filing deadline typically coincides with the final date for filing an income tax return for the relevant assessment year. For most taxpayers, this due date falls on or before the 31st of July, immediately following the conclusion of the financial year in which the transaction transpired. To evade penalties and potential legal repercussions, both contributors and recipients must proactively adhere to the filing date. The punctual completion of Form 10BD not only ensures compliance with the law but also underscores a commitment to transparent financial transactions.

Importance of Form 10BD Compliance: Compliance with Form 10BD extends beyond mere legal adherence. It champions transparency, accountability, and trust within the tax system. While recipients can demonstrate their commitment to abiding by the law, thereby enhancing their credibility and reputation, donors can leverage tax benefits on their charitable contributions.

Conclusion: The bedrock of maintaining accountability and transparency in transactions involving tax- exempt entities rests heavily on Form 10BD of the Income Tax Act. Both donors and recipients are duty- bound to grasp the significance of this form and fulfill their obligations by meticulously disclosing pertinent information. Timely compliance with Form 10BD not only fosters legal adherence but also fosters a culture of fairness and responsibility in financial transactions. By upholding these legal commitments, donors and beneficiaries collectively contribute to a tax system that benefits society as a whole.

Section 220(2) Does Not Allow Department to Levy Interest on Already Paid Tax

Catherine Thomas Vs Principal Chief Commissioner of Income Tax (Kerala High Court) Introduction: In a recent judgment by the Kerala High Court, the case of Catherine Thomas vs. Principal Chief Commissioner of Income Tax addressed the issue of whether Section 220(2) of the Income Tax Act has retrospective effect and the liability to pay interest on crystallized tax. The court’s decision clarifies the applicability of this section and its impact on tax payers.

Detailed Analysis: The petitioner in this case challenged a demand notice (P12) from the Income Tax Department, which directed them to pay interest on an income tax amount of Rs. 10,76,869. The tax amount had been determined finally through an order (Ext.P4) dated 10.01.2011, passed on the petitioner’s rectification application. The petitioner had already paid the entire tax amount on 27.01.2011, within 35 days from the date of the Ext.P4 order. The key issue revolved around the applicability of the 2nd proviso to Section 220(2) of the Income Tax Act, which had been inserted by the Finance Act of 2014. The petitioner argued that this provision was only applicable from 01.10.2014, and therefore, it could not be used to impose interest on a tax demand that had crystallized and been paid before that date.

The petitioner contended that their case should be governed by the unamended provision of Section 220 as it existed on 01.10.2014. Under this provision, the liability to pay interest arose only if the taxpayer failed to make the payment of the finally assessed amount within 35 days from the date of crystallization of the tax. In this case, the petitioner had paid the tax within 35 days from the date of the Ext.P4 order. The petitioner’s argument found support in a Supreme Court judgment in the case of Vikrant Tyres Ltd vs. First Income Tax Officer. The Supreme Court held that Section 220(2) of the Income Tax Act would apply only when, after receiving a notice of demand under Section 156, the taxpayer continued to default in the payment of tax. Interest would be levied only if the taxpayer defaulted in paying the tax assessed 35 days after the notice of demand under Section 156.

The Kerala High Court concurred with the petitioner’s position. It recognized that the 2nd proviso to Section 220(2) introduced by the Finance Act of 2014 had prospective operation and was not retrospective. Therefore, it could not be used to impose interest on tax that had already been paid. The court set aside the impugned notice (P12).

Conclusion: The Kerala High Court’s judgment in Catherine Thomas vs. Principal Chief Commissioner of Income Tax clarifies that Section 220(2) of the Income Tax Act has no retrospective effect and cannot be applied to impose interest on tax demands that had crystallized and been paid before 01.10.2014. This decision provides important guidance for taxpayers and tax authorities regarding the applicability of this section and the timing of interest liability in income tax cases.

Trust Taxation: Recent Case Laws

- SAE India vs Income tax officer and Income tax officer vs SAE India ( Chennai ITAT) Issue:Whether principle of Mutuality applies? How corpus donation can be taxed? How far general public utility as defined under Section 2(15) would impact the functioning of organisation Facts: Assessee-Trust with main object of holding technical meetings, workshops, seminars and other educational programs to encourage the profession of mobility engineering claimed exemption under Section 11 which was denied by the Revenue on the premise that Assessee’s main object is general public utility and since the gross receipts from GPU is in excess of prescribed limit as per Section 2(15), exemption under Section 11 cannot be allowed;Revenue also taxed Assessee’s ‘corpus donation’ of Rs.12.55 Lac received towards Magazine Fund while rejecting Form 10 on the premise that once the benefit of exemption under Section 11 is denied, any income part of corpus of trust is part of total income; CIT(A) partly allowed Assessee’s appeal. But there is no clarity as to whether the funds received are utilised for the purpose it meant.Provision: The principle of mutuality is clear is that income received such be utilised for the purpose sought after. 2(15) of the Act is clear that advancement of general public utility can be done but business receipts cannot exceed 20% of total sum. Conclusion: Assessee failed to file any evidences to prove its arguments that it is a mutual benefit society; Accordingly, set aside CIT(A) order and remits back to AO with a direction to consider the issues pertaining to mutuality, computation of taxable income and taxability of ‘corpus donations receipts towards Magazine Fund afresh in view of Section 2(15) and SC ruling in Ahmedabad Urban Development Authority.

- Secundrabad Club vs CIT (Supreme court) Issue: Whether money received for club from members(individual corporate) would be taxable and if money is invested in fixed deposit would concept of doctrine of mutuality would apply? Facts: The assessee is a club which has received money from members but invested in fixed deposit and money collected were not merely used for members but even some commercial substance was involved.Provision:As per Act the principle of mutuality applies only if fund are utilised for the purpose meant. If used for commercial activities the doctrine of mutuality ceases. Conclusion: It was held in Supreme court that by depositing funds in bank the first condition for the claim of mutuality is not satisfied”; SC states that when funds are deposited with banks, identicality between the contributors to the common fund and the participators in it which is a sine qua non for the application of the principle of mutuality would get ruptured, hence interest income is taxable. This ruling distinguishes from other club ruling but the litigation in the other cases were different. I would like to add upon that if only money is received from Members and utilised for purpose of club or say a room rent given on rent and money received is utilised only for the same then principle of mutuality hold good.

- ACIT vs M/S Financial Inclusion trust (Delhi ITAT)Issue: Whether corpus specific contribution by way of capital receipt is taxable.Facts: Assessee, an unregistered trust under Section 12AA received Rs.44.25 Cr towards corpus donation grant from Bandhan-Konnagar trust (donor trust) being registered under Section 12A and declared it as ‘capital receipt’ in the return of income; Revenue treated the corpus donation grant as income of the Assessee on the premise that Assessee is not eligible for exemption under Section 11(1)(d) since it is not registered under Section 12A; CIT(A) allowed.

Provision: Only a trust registered under 12A for which corpus donation is taxable for those otherwise not registered under 12A the corpus donation happens to be not taxable. Conclusion: Corpus specific voluntary contributions are outside the scope of taxation in case of an unregistered Trust under Section 12 or 12A since their nature is capital; Accordingly, upholds CIT(A) and dismisses Revenue’s appeal.

Tax Authorities cannot step into shoes of businessmen to determine business purpose expenditure Serco India Pvt. Ltd. Vs ACIT (ITAT Delhi)

Held: Assessee-company was a subsidiary of Serco Group PLC, UK and was established as a captive service center with an objective to provide IT and IT enabled services to Serco Group. It filed its return of income declaring loss of Rs. 5,68,34,642/- which was processed u/s 143(1). The assessment was completed u/s 143(3) wherein addition u/s 68 of Rs. 11,73,19,373/- was made on account of difference between the opening balance andclosing balance of sundry creditors, and ad-hoc disallowance of Rs. 4,43,77,875/- was also made on account of 20% of net ‘other expenses’ of Rs. 22,18,89,377/-debited in profit & loss account. Assessee company preferred an appeal before CIT(A), who had decided the appeal wherein CIT(A) had confirmed the addition u/s 68 of Rs. 11,73,19,373/- and enhanced the disallowance out of expenses at Rs. 10,18,44,938/- as against disallowance of Rs. 4,43,77,875/-made by AO. Assessee contended that CIT(A) was not justified in making disallowance of total non-operating and non-allocated expenses of Rs. 10,18,44,938/-without properly considering the documents furnished during appellate proceedings before him. It was maintaining regular books of accounts Transfer Pricing Report was also accepted by the TPO, the Arm’s Length Price (ALP) declared by assessee observing in order that ‘no adverse inference was drawn in respect of the International and Specified Domestic Transactions undertaken by assessee during the F.Y. 201213. Thus, the expenses debited to Profit & Loss Account were genuine expenses incurred wholly and exclusively for the purpose of business. It was held that an organization incurred both operating expenses as well as non-operating expenses for running the business. There were certain expenses which were not allocable to a particular activity. Non-allocable expenses even for a management consultancy providing company were costs that could not be directly attributed to specific projects or client engagements and therefore could not be allocated on a project-by-project basis. These expenses were more general in nature and were incurred to support the overall operations of the company rather than any particular client work. CIT(A) was not justified in allowing only ‘operating expenses’ allocable to the segment of rendering management consultancy services and direct expenses on sub-letting and disallowing all the non-operating and non-allocable expenses incurred by assessee company. CIT(A) was not justified in disallowing non- operating non-allocated expenses and expenses incurred for exploring new business in the line of Maintenance and Operations of Transportation by assessee. Assessee had incurred expenses for preparing technical and financial bids for obtaining contracts for Maintenance and Operation of BRT buses in Indore. Further, assessee had also participated in bid for Maintenance and Operation of Chennai Metro Rail. Assessee was successful in getting one contract during the year related to Indore BRT Bus Operations and Maintenance of 50 buses for an initial period of six years. It was also a trite law that Income Tax Authorities could not step into the shoes of the businessmen to determine as to how much expenditure should have been incurred for the purpose of business. CIT(A) was not justified in disallowing total non-operating and non- allocable personnel expenses of Rs. 4,85,98,973/-. It wa also evident from the fact that trade payables as on 31.03.2015 were of Rs. 33,85,497/- only, as shown in the Audited Balance Sheet of the assessee company for F.Y. 201415 which was nominal (PB Volume-2 Page 852). This fact also established that the sundry creditors (trade payables) were subsequently paid and were genuine. Hence, no addition was called for u/s 68 of Rs. 11,73,19,373/- on account of unexplained increase in sundry creditors in the books of account during the previous year. Therefore, the disallowance of Rs. 10,18,44,938/- out of the expenses and addition u/s 68 of Rs. 11,73,19,373/- made on account of difference in opening balance and closing balance of sundry creditors was hereby deleted.

Assessment Order/Addition Unsustainable if Solely based on AIR Information

Bona Sera Hospitality Pvt. Ltd Vs DCIT (ITAT Mumbai) Introduction: The case of Bona Sera Hospitality Pvt. Ltd vs. DCIT came before the Income Tax Appellate Tribunal (ITAT) in Mumbai. The appeal was against the order of the Commissioner of Income Tax (Appeals) [CIT(A)] for the assessment year 2011-12, dated March 24, 2023.

Detailed Analysis: The primary contention of the assessee was the CIT(A)’s partial allowance of the appeal, directing the Assessing Officer (AO) to verify additions of Rs.1,91,956/- and Rs.4,74,558/-. Additionally, the assessee disputed the non-deletion of Rs.3,67,773/-, the amount that couldn’t be reconciled. The AO, relying on the AIR information and finding discrepancies in the 26AS statement, directed the assessee to reconcile the income. Despite reconciling a significant portion, a mismatch of Rs.8,42,331/- remained, leading to an addition of Rs.10,34,287/- by the AO. The CIT(A) partially allowed the appeal, directing the deletion of Rs.6,66,514/-. The assessee argued that reconciling 1100 out of approximately 1200 items was a substantial effort, and the remaining discrepancy was due to unintentional mistakes, urging against additional tax.

The appellant highlighted its substantial revenue, the nature of its business, and the difficulty in reconciling all entries. The tribunal observed the detailed reconciliation efforts made by the assessee and noted that the revenue declared far exceeded the amount mentioned in the AIR information. It emphasized that additions solely based on AIR information, without full details and when the declared receipts exceed AIR amounts, are not legally sustainable. The tribunal cited precedents, including the Bangalore Bench’s decisions, emphasizing the need for the AO to prove the receipt of income when disputed by the assessee. It noted that the percentage of unreconciled items to the revenue was negligible (0.3376%), directing the deletion of the addition of Rs.3,67,773/-.

Different depreciation rates under companies & Income Tax Act- A hassle need to be removed – A suggestion

Introduction: – Depreciation on assets e.g., building, machinery, furniture and vehicle is claimed as expenses in accounts of every business entity as all these assets depreciate on daily basis due to various factors. Depreciation of a particular asset should be calculated on the basis of useful life of an asset. However, Companies Act, 2013 and Income Tax Act, 1961 have different rates of depreciation and different methods e.g., straight line method and WDV method. So, a company have different amounts of depreciation as per Companies Act and as per Income Tax Act. Further the company have to calculate Deferred tax assets / liability as per AS 22 to give a true and fair view of financial statements. Depreciation under Companies Act, 2013 is calculated on the basis of useful life of assets, while rate of depreciation as per Income Tax Act, 1961 are normally higher, it may be intentionally on part of the law makers to incentivize businesses

Our suggestions: – 1. Rates of depreciation under both the laws should be brought to same to avoid complications in the tax calculations and calculation of profit/ loss on sale of assets etc.

2. In lieu of incentive of higher depreciation to businesses, income tax rate may be brought down by 2 % in case of companies and 3% in case firms and individuals. However, manufacturing companies opting for tax rate u/s 115 BAB may continue be taxed @ 15% as it is already reasonably low.

3. Since, WDV as per Companies Act, 2013 would be more than under Income Tax Act, 1961, no depreciation should be allowed under Income Tax act, 1961 till WDV of both the acts come at same amount. However, for the sake of simplification total WDV of each act may be taken instead of each block of assets.

4. In following years depreciation as per books of accounts may be allowed under income taxes, so no adjustments in ITR will be required, no deferred tax liability needs to be calculated. The amount of Deferred Tax liability be recalculated every year till both WDV reaches same amount, which will also become zero in that year.

5. In most cases, it will take 3-5 years to reach both WDV at par, after which it will be hassle free ITR.

Benefits to revenue: –

- On one hand it will be a step towards ease of doing business and on other hand reducing income tax rates will enhance image of our tax system in business community in India and abroad.

- Moreover, in case of sale of depreciable assets sale price is reduced from WDV of block of assets, so revenue do not get the tax on sale of same, if the above proposal is accepted, exchequer will get its due share on every sale of assets.

Your best teacher is your last mistake.

– Dr. APJ Abdul Kalam

DGFT & CUSTOMS UPDATEBy CA. Ashit K. Shah |

|

1. Notifications issued under Customs Tariff:

| Notifications No | Remark | Date |

| 64/2023

– Customs

|

Basic Customs Duty (BCD) & Agricultural Infrastructure and Development Cess (AIDC) in respect of the imports of Yellow Peas covered under HSN 0713 10 10 when import into India from 8th December, 2023 to 31st March, 2024. | 07 -12 -2023 |

| 65/2023

– Customs |

Extend the benefit of Nil Agricultural Infrastructure and Development Cess (AIDC) on Lentils (Mosur) by amending N. No. 49/2021 up to 31st March, 2025. | 07 -12 -2023 |

| 66/2023

– Customs |

Certain conditions are substituted in the N. No. 22/2022 to enable Gold imports by valid Tariff Rate Quota (TRQ) holders under India UAE CEPA.

|

22 -12 -2023 |

| 94/2023

– Customs (NT) |

Amendment in the Sea Cargo Manifest and Transhipment Regulations, 2018 | 28 -12 -2023 |

|

15/2023 – Customs (ADD) |

Anit Dumping Duty (ADD) on “Industrial Laser Machines, used for cutting, marking, or welding”, falling under the tariff item 8456 84561100, 84569090, 84798199, 85152190, 85158090 and 90132000, originating in, or exported from China PR and imported into India, for a period of 5 years from the date of Notification, which will be payable in Indian Currency.

|

22 -12 -2023 |

| 16/2023

– Customs (ADD) |

Anit Dumping Duty (ADD) on “Gypsum Board / Tiles with lamination at least on one side”, falling under chapter 68, originating in, or exported from China PR and Oman and imported into India, for a period of 5 years from the date of Notification, which will be payable in Indian Currency. | 26 -12 -2023 |

| 17/2023

– Customs (ADD) |

Anit Dumping Duty (ADD) on “Wheel Loaders”, falling under tariff item 84295900 and 84295100, originating in, or exported from China PR and imported into India, for a period of 5 years from the date of Notification, which will be payable in Indian Currency. Wheel Loaders are defined in the notification and certain specification of wheel loaders are excluded from the scope of levy. | 27 -12 -2023 |

| 18/2023

– Customs |

Anit Dumping Duty (ADD) on “Electrogalvanized Steel”, falling under 29-12-2023 tariff item 7209, 7210, 7211, 7212, 7225 and 7226, originating in, or exported from Korea RP, Japan and Singapore and imported into India, vide N. No. 29/2022 – Customs (ADD). Now amendment in notification carried out to include change in the name of the product. | 29-12-2023 |

2. Notifications under DGFT:

| Notifications No | Remark | Date |

| 54/2023 | Extension in “Free” Import Policy of Urad [Beans of the SPP Vigna Mungo (L.) Hepper] [ITC(HS) 0713 31 10] and Tur/Pigeon Peas (Cajanus Cajan) [ITC(HS) 0713 60 00] under ITC (HS) 2022, Schedule – I (Import Policy) till 31.03.2025. | 28 -12 -2023 |

| 53/2023 | Notification No. 31/2023 dated 11.09. 2023 is amended. Export of Food Supplements containing botanicals under above mentioned ITC HS Codes intended for human or animal consumption to European Union and United Kingdom will require issuance of official certificate by EIC/EIA or SHEFIXIL. | 28 -12 -2023 |

| 52/2023 | Existing notification No. 27/2015-2020 dated 17th August 2022 is amended to the extent that export of Rice (Basmati and Non-Basmati) to EU member states and other European Countries namely Iceland, Liechtenstein, Norway, Switzerland and United Kingdom only will require Certificate of Inspection from EIA/EIC. Export to remaining European countries will not require Certificate of Inspection by Export Inspection Council / Export Inspection Agency for export from the date of this notification for a period of six months. | 12 -12 -2023 |

| 51/2023 | Export prohibition of de-oiled rice bran under ITC HS Code 2306 and under any other HS code is extended till March 31, 2024. | 08 -12 -2023 |

You cannot change your future, but, you can change your habits, and surely your habits will change your future.

– Dr. APJ Abdul Kalam

FOR EDUCATIONAL INSTITUTIONSCompiled By By Adv. Hemant Gandhi & CA Premal Gandhi |

|

While the Educational Institutions are facing a lot of heat in the aftermath of the Supreme Court Judgment in the case New Noble Educational Society, (2022) 143 Taxmann.Com 276 (SC) on the activities being carried on by these institutions from time to time.

The assessee trust running multiple colleges for higher education filed an application for exemption under section10(23C) (vi). The CIT(E) denied it on the ground that the assessee could not be said to be existing ‘solely’ for educational purposes since it had multiple objects in its trust deed such as medical treatment for poor, giving scholarships, organising family planning centers, activities relating to public health etc. The assessee clarified that it ran medical colleges and incorporation of medical object in the trust deed was also a part of the educational object.

The Tribunal made the following observations:

- The assessee had submitted clarification regarding its medical objects but remained silent on other non- educational objects such as organizing family planning centres, activities for upbringing and training for self-reliance of orphans and destitute women etc. This proved that it was not existing ‘solely’ for educational purposes.

- The assessee had not submitted any documentary evidence to establish that the scholarships had been used only for educational purposes

- In view of the judgement of Supreme Court in New Noble Educational Society, (2022), the term ‘solely’ had been interpreted to ‘exclusively’, that is, all objects of the assessee had to be educational or relating to education in order to claim exemption under section 10(23C) (vi).

Hence, it was held that, the CIT(E) was justified to reject the application since the assessee had objects unrelated to education.

[Parul Arogya Seva Mandal Trust, C/O. Ahmedabad Homeo Medical College v. CIT(E), 2023 (8) TMI 32 – ITAT Ahmedabad]

Strength is life; weakness is death.

– Swami Vivekananda

LIGHT THE LAMP OF FINANCIAL FREEDOMCompiled By By Mr. Tushar P. Joshi |

|

At the outset let me Convey My best wishes for the Happy 2024.

This New Year, light the lamp of financial freedom.

Here are some simple yet powerful steps to get started:

*Plan for Your Medium and Long Term Goals*

we all have different financial goals and dreams like planning for children’s marriage or education, foreign trip, buying a house or vehicle, retirement etc. However, without a proper plan, many of these goals remain a distant dream. A small but regular saving can help in creating a huge corpus due to the power of compounding with time. If you are not sure about how to create a financial plan, it is best to seek the help of an expert for financial planning.

*Get Rid of Your Loans and Liabilities*

Just like our home cleansing ritual before Diwali, one should get rid of all their loans and liabilities at the earliest as they put an unnecessary burden on our finances thus leaving very less scope for saving and investing.

*Plan for Retirement*

Retirement is a period when your income stops but expenses won’t. Besides due to increasing life expectancy people are now living longer than before. By planning for your retirement when you are young and earning, you can not only have adequate income but also live comfortably without depending on others.

*Buy Adequate Health Insurance*

Health is the real wealth. Medical issues can crop up anytime putting a huge burden on one’s finances. Lack of adequate money in such circumstances can result in a compromise. Health insurance can ensure there that one can avail the best treatment without breaking their hard-earned savings.

*Need to Do Estate Planning*

Estate planning can be defined as the process of designating who will receive your assets after your lifetime. The basic objective of estate planning is to ensure that your chosen beneficiaries receive your assets in a hassle-free manner while minimizing their tax liability.

Life insurance is one of the best options for estate planning in the world which ensures there is no legal dispute after your lifetime and helps your chosen one to receive your wealth smoothly.

I request everyone to start implementing above points without any further delay.

| Members Name | Date of Birth |

| Abad Prafulla S. | 10 – January |

| Agarwal Rakesh Omprakash | 10 – January |

| Agrawal Tarun Ratan | 10 – January |

| Agrawal Vishnu Bansilal | 10 – January |

| Ahmedabadi Dawood A | 10 – January |

| Amate Sanjay B. | 10 – January |

| Anajwala S. A. | 10 – January |

| Ansari Afzal Imam Serajiddin | 10 – January |

| Ashar Yogesh Hansraj | 10 – January |

| Badekar Gaurav Jaising | 10 – January |

| Badhani Hemendra Dayachand | 11 – January |

| Baig Naushad Vaish | 11 – January |

| Bane Rajesh G. | 12 – January |

| Bangad Laxminarayan R | 12 – January |

| Barchha Prital M. | 12 – January |

| Barchha Prital Mathuradas | 12 – January |

| Bedarkar Shripad Shankar | 12 – January |

| Bedmutha Shailesh Ashok | 12 – January |

| Begari Balram Bheemappa | 12 – January |

| Bhadane Ravindra Vedu | 12 – January |

| Bhandary Ananda Challa | 13 – January |

| Bhanushali Chandresh Khimji | 13 – January |

| Bhosale Kiran Anandrao | 13 – January |

| Bohade Mohan H | 14 – January |

| Bohra Deendayal Jeetlal | 14 – January |

| Bosamia Jagdish J. | 14 – January |

| Bothra Pranav Praveen | 14 – January |

| Chaddva Mitesh Shantilal | 15 – January |

| Chandratre Rajendra P. | 15 – January |

| Chaudhari Sunil Devram | 15 – January |

| Chavan Kumar Balaso | 15 – January |

| Chavan Swapnil Nimba | 15 – January |

| Chhallani Mahavirchand L. | 15 – January |

| Chheda Kalpesh Nagji | 15 – January |

| Chheda Rajesh | 16 – January |

| Chheda Rajesh Raichand | 16 – January |

| Chopra Sushil Jasraj | 16 – January |

| Chordia Arvind B | 17 – January |

| Choudhary Suresh Akharam | 17 – January |

| Chudasama Rakesh Naresh | 18 – January |

| Chudiwal Mukesh B | 18 – January |

| D’souza Pius Maxim | 18 – January |

| Dalvi Sunil Vithoba | 18 – January |

| Damle Surendra Gopal | 19 – January |

| Dave N. M | 19 – January |

| Dave Rashmikant K. | 19 – January |

| Dedhia Avani Navinchandra | 19 – January |

| Dedhia Monik Laxmichand | 19 – January |

| Desai Yashvant R. | 19 – January |

| Deshmukh Arun Gopalrao | 19 – January |

| Deshpande Ratnakar Dattatraya | 19 – January |

| Jadhav Dayaram Lashkar | 20 – January |

| Jadhav Govind T. | 20- January |

| Jadhav Sandeep Appaso | 20- January |

| Jain Anil Hiralal | 20- January |

| Jain Mahendra Kumar | 20- January |

| Jain Mukeshkumar Jaswantraj | 20- January |

| Jambotkar Rajendra Pandurang | 21- January |

| Jeswani Satish Rameshlal | 21- January |

| Jhaveri Rajnikant Sevantilal | 21- January |

| Jogani Mitul Sudhirkumar | 21- January |

| Kadam Sudarshan Sadashiv | 22- January |

| Kajave Atul Anant | 22- January |

| Kalantri Sanket Narayan | 22- January |

| Kanbhar Vijay Tulsidas | 22- January |

| Kapadia Harsh Arun | 23- January |

| Kapadia Pradip R | 23- January |

| Kapadia Vinod P. | 23- January |

| Kawale Nagesh Chandrashekhar | 23- January |

| Khandelwal S.K.S. | 23- January |

| Khandelwal Vijay | 23- January |

| Khanna Rajiv D. | 23- January |

| Khan Shaukatali Nazeer | 24- January |

| Kochrekar Girish Gajanan | 24- January |

| Kothari Dipesh Balchand | 24- January |

| Kotwal Deepak Vasant | 24- January |

| Kubadia Bhavik A | 24- January |

| Kukreja Rajesh Gulabsingh | 24- January |

| Kulkarni Abhay Bapurao | 24- January |

| Kulkarni Jayesh Vikas | 24- January |

| Kulkarni Nitin V. | 24- January |

| Lahoti Ramakant Rampratap | 25- January |

| Lokhandwala Moiz Fakhruddin | 25- January |

| Madhyani Harmesh Shyamlal | 25- January |

| Maity Bipul Bishnupada | 25- January |

| Mehta Bhavin Jatin | 26- January |

| Mehta Ritesh Rajesh | 26- January |

| Mohite Umesh Mohanrao | 26- January |

| Munot Swapnil M. | 26- January |

| Nayak Deepak Padmanabh | 26- January |

| Nayak Ranjit Kumar | 26- January |

| Nikam Rajendra K | 26- January |

| Nimankar Rekha Rahul | 26- January |

| Paithankar Bhushan Bhagwan | 26- January |

| Palde Prakash Ambadas | 26- January |

| Pandey Santosh Lalmani | 26- January |

| Parikh Pankaj Fatechand | 27- January |

| Patel Vikram Rameshchandra | 27- January |

| Patil Chandrakant T | 27- January |

| Patkar Mahadev Satyawan | 27- January |

| Phulsundar Aarambhi Gangadhar | 27- January |

| Rangani Rasiklal Devji | 27- January |

| Rathi Ashikumar Gowardhandasji | 27- January |

| Rathi Girish Jethalalr | 28- January |

| Rawal J D. | 28- January |

| Rohida Purshotham R | 28- January |

| Sahane Prakash P. | 28- January |

| Sakala Pramod H. | 28- January |

| Sakate Vishal Vilas | 29- January |

| Salgaonkar Tushar Yeshwant | 29- January |

| Salot R C | 29- January |

| Saluja Rajesh Gurdasmal | 29- January |

| Shaikh Moizahmed Noorahmed | 29- January |

| Sanghavi Rakesh Bhanvarlal | 29- January |

| Shah Arvind Jivraj | 30- January |

| Shah Chandresh Chhabildas | 30- January |

| Shah Chirag Pravin | 30- January |

| Shah Dhanesh Chandrakant | 30- January |

| Shah Dhaval Yogesh | 30- January |

| Shah Harshad Zaverchand | 30- January |

| Shah Ketan Chandrakant | 31- January |

| Shah Kivant I | 31- January |

| Shah Piyush Dinesh | 31- January |

| Shah Praful L | 31- January |

| Shah Rajendra Mansukhilal | 31- January |

| Shah Rajendra Natwarlal | 31- January |

| Gundesha Girish Bherumal | 01- February |

| Hindivali Prakash Shivappa | 01- February |

| Hussain Mazhar Musharraf | 01- February |

| Ingale Nilesh Vitthal | 01- February |

| Jadhav Mahesh Bhagwan | 01- February |

| Porania Mansi Bharat | 02- February |

| Rathod Bhavesh Somchand | 02- February |

| Ruparelia Ashish Damodardas | 02- February |

| Saboo Kamlesh Ramprasd | 02- February |

| Savani A G | 02- February |

| Sawant Shantaram R. | 02- February |

| Sawarkar Amol Prabhakar | 03- February |

| Shah Alpesh B. | 03- February |

| Shah Atulkumar V. | 03- February |

| Shah Hemal Pravinchandra | 03- February |

| Shah Jignesh Kishorkumar | 04- February |

| Shah Pranav Ashokkumar | 04- February |

| Shah Rajesh Chimanlal | 04- February |

| Shah Vipul Jitendra | 04- February |

| Shah Vipul Manaharlal | 04- February |

| Shaikh Abdul Rashid | 04- February |

| Shaikh Sardar Mohammed-Yusuf | 05- February |

| Shaikh Shakeel Ahmed | 05- February |

| Sharma Deepak Mahaveer | 05- February |

| Solanki Jagdish Ratanlal | 05- February |

| Sonawane Sanjay Madhavrao | 06- February |

| Soni Mahendrakumar Murarilal | 06- February |

| Surte Pramod Prabhakar | 06- February |

| Suryavanshi Arjun Pandurang | 06- February |

| Taparia Jitendra Shankarlal | 06- February |