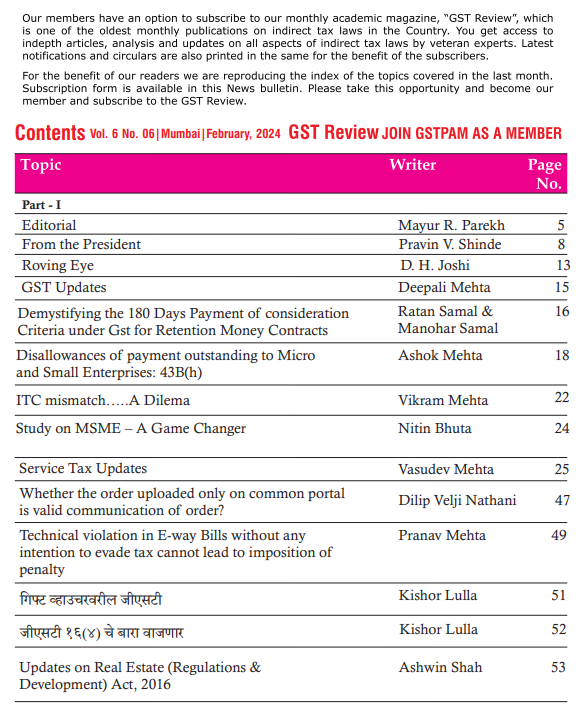

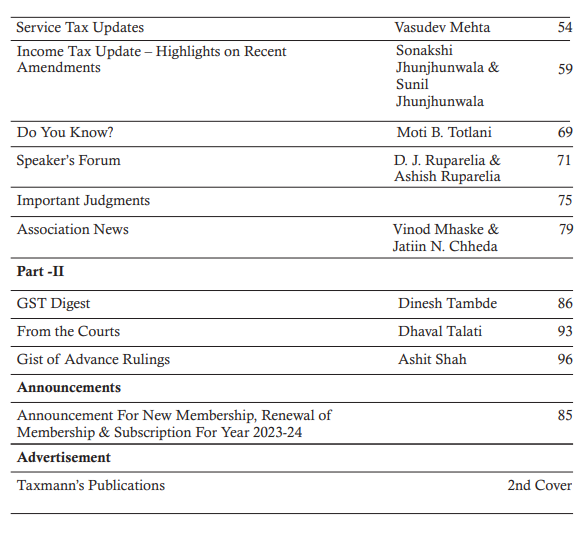

GSTPAM News Bulletin March 2024

CIRCULAR FOR RENEWAL OF MEMBERSHIP/SUBSCRIPTION CHARGES FOR THE F.Y. 2023-24

Dear Members,

RENEWAL OF MEMBERSHIP FOR F.Y. 2023-24

The Membership Fees for the year 2023-24 are due for renewal on 01.04.2023. We appreciate your Continuing support and participation in the activities of our Association.

The timely Renewal of Membership will enable the members to continuously receive the updates on various activities of GSTPAM along with the GSTReview, News Bulletin, Circulars, Messages, Webinars and online access to the website www.gstpam.org. The Life Members only need to renew the subscription charges for the GST Review. The members can also avail the benefit of discount by paying advance for subsequent two years membership fees /subscriptioncharges.

The Membership Renewal Fees received after 30th April, 2023 will be subject to approval of the Managing Committee. If the Renewal fees for a particular year are not paid, then the member is liable to pay Admission Fees again for Renewal in the subsequent year.

Delayed Renewal Members will be provided Pre Renewal GST Review subject to availability upon payment of such additional courier charges.

The details of Membership/Subscription Fees are given below for your ready reference

| Type of Membership | Membership Fees incl. GST | Admission Fees Incl.GST | Subscription Charges for GST Review | Total |

|

New Membership Application |

||||

| Donor Member | 24,780.00 | 600.00 | 25,380.00 | |

| Patron Member | 17,700.00 | 600.00 | 18,300.00 | |

| Life Member | 11,800.00 | 944.00 | 600.00 | 13,344.00 |

| Life Member (Conversion from Ordinary) | 11,800.00 | 590.00 | 600.00 | 12,990.00 |

| Ordinary Local Member | 1,770.00 | 590.00 | 2,365.00 | |

| Ordinary Outstation Member | 1,475.00 | 590.00 | 2,065.00 | |

New Membership Application (Firm/LLP)

| Ordinary Local Member | 1,770.00 | 944.00 | 0 | 2,174.00 |

| Ordinary Outstation Member | 1,475.00 | 944.00 | 0 | 2,419.00 |

| Patron Member | 17,700.00 | 0 | 600.00 | 18,300.00 |

| Donor Member | 24,780.00 | 0 | 600.00 | 25,380.00 |

Advance Membership/ Subscription charges for subsequent two years 2024-25& 2025-26 (Non-Refundable)

| Ordinary Local Member | 3,186.00 | 3,186.00 | ||

| Ordinary Outstation Member | 2,665.00 | 2,665.00 | ||

| Life Member (Individual/Firm/LLP) | 0 | 1200.00 | 1,200.00 | |

| Patron Member | 0 | 1200.00 | 1,200.00 | |

| Donor Member | 0 | 1200.00 | 1,200.00 |

Subscription for GST Review for F.Y. 2023-24 by Non-Members

| Subscription fees for GSTR | 1000.00 | 1,000.00 |

Advance Membership / Subscription charges for subsequent two years 2024-25& 2025-26 (Non-Refundable)

| Subscription Fees -GSTR | 0 | 2000.00 2,000.00 |

Modes of Payment:-

| Cheque | A/c Payee Cheque drawn in favor of “The Goods & Services Tax Practitioners’ Association of Maharashtra” payable at Mumbai. |

| NEFT Details | The Goods & Services Tax Practitioners’ Association of Maharashtra

Bank of India, Mazgaon Branch Current Account No. 007020100001816, IFSC Code – BKID0000070. Online generated transaction Acknowledgement should be sent by email on [email protected] along with membership and payment details Members are requested to send their physical form to the association for Approval, Issuance and Office record. |

| Cash | Renewal form along with requisite amount will be accepted between 10.30 a.m. and 5.30 p.m. on all working days except Saturday at our Office at

Mazgaon Library – Mazgoan: 1 st Floor, 104, GST Bhavan, Mazgaon, Mumbai – 400 010 Or |

| Identity

(New Members) |

New Members should provide the following as Identity Proof : PAN, Aadhar Card, Constitution Document.

Address Proof(any one) : Electricity Bill / Passport/ Aadhar Card / Driving License/ Voter id/ Ration Card along with Membership Form |

| Identity Card (For Renewals) | Ordinary Local/Outstation Members should provide Two Photographs along with the Renewal Form for issue of I- cards. |

| Online Payment Link | Members can make online payment on our website www.gstpam.org. are requested to download Members Renewal form from website. Update the latest details in the form, scan it and mail at email [email protected]

Payment Link : https://www.gstpam.org/online/renew-membership.php If you are login first time? Click here for create your password |

We value your continuation of the membership and look forward to your renewal to this effect.

Dated:- 21.07.2023

Vinod Mhaske

Jatin Chheda

Hon. Jt.Secretary

ORDER FORM FOR GSTPAM REFERENCER 2023-24

(Members are requested to take out the photocopy of the Order Form for booking)

To

The Convenor,

GSTPAM Referencer Committee

The Goods & Services Tax Practitioners’ Association of Maharashtra

Room No. 8 & 9, Mazgaon Tower, Mhatar Pakhadi Road,

Mazgaon,

Mumbai

Dear Sir,

Please book my/our order of GSTPAM Referencer for the year 2023-24 as given below.

| Sr. | Particulars | Price per copy if booked prior to 15th July 2023 | Price per copy if booked afterto 15th July 2023 | Qty | Total RS. |

| 1 | GSTPAM Referencer 2023-24 Part I & II

(GST, VAT & Allied Law Referencer & Updated GST Rate schedules). |

700 | 750 | ||

| 2 | Courier Charges (For Outstation members only) (per set) | 130 | 130 | ||

| 3 | Courier Charges (For Local members only) (per set) | 100 | 100 |

Note :

- Referencer will be published in Part I & II (for GST, VAT & Allied Laws Referencer & Updated GST rate schedules).

- Applicants requiring more than 5 copies of the Referencer are required to give a request on their letter head along with the order form. Tax Practitioner’s Associations can place order in bulk quantity by making request on their letterhead signed by the Association’s President and Secretary.

- Applicants will be issued receipt at the time of placing of their order. Applicants are requested to bring receipt at the time of taking the delivery of the Referencer. No delivery of the Referencer shall be given, unless the receipt for payment is submitted at the counter. If the receipt for payment is lost, than no delivery of the Referencer shall be given.

The payment for the above order of……………………………………………………………………….… (Rupees in words) is made herewith by Cash /Card /Cheque /Demand Draft No. ………….……dated ……….……. drawn on……………………………………………… Bank Branch, Mumbai.

Signature …………………………….

Membership Number………………………….. Address.………………………………………………… Name ……………………………………… ………………………………………………………………………………………………………………… ………………………………………………………………… Office Tel No…………………………………… Residence Tel No……………………………………… E-mail: …………………………………………. Mobile No.…………………………………………….

PROVISIONAL RECEIPT

Received with thanks payment of. ………………… from………………… vide Cash /Card /Cheque /NEFT/Demand Draft No. …………………………. Date ………………. drawn on…………………………………………………Bank………………………………… Branch, Mumbai.

Signature ……………………………

Date…………………………………. Name of staff of GSTPAM……………………

Note:

- * Please fill in all the details in the above form and send the same to the GSTPAM’s office at Tower or at Mazgaon library along with requisite payment. For Direct Deposit / NEFT payment –

- * Bank of India, Mazgaon – Account No. 007020100001817, IFSC Code – BKID0000070. Acknowledgement of the same should be sent by email: [email protected] along with duly filled form.

- * Please mention your name and membership number on the reverse side of the Cheque / Demand Draft.

- * The counter timings are from 10.30 a.m. to 5.30 p.m. on Monday to Friday.

- * The Cheque / DD should be drawn in the name of “THE GOODS AND SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA

INTENSIVE STUDY COURSE CIRCULAR FOR THE YEAR 2023-24

Respected Members,

It is 7 th year of the GST act is implemented. After implementation of GST, whole fraternity of Indirect Tax Practitioners and Trade are facing various challenges with regard to implementation, transition, interpretation, practical aspects, prescribed schedule rates, AAR, Department Audit, various notices related to ITC mismatch and so on.

We all are aware about the practical difficulties we are facing while applying the rules and procedures of the GST law and the frequent amendments to the law especially due to frequent lockdown. With the view to update our fellow members on the latest development in law and to discuss the practical issues arising there from, our association has been regularly conducting Intensive Study Course. This year the Intensive Study Course is designed to enable the members to study and discuss various issues on Indirect Tax Laws mainly on GST Law, as well as on profession tax, etc.

With the same enthusiasm to discuss mainly on various aspects of GST Law, We are starting our hybrid mode Intensive Study Course for the year 2023-24 from Friday, 15-12-2023 onwards.

The Intensive Study Course is such an academic activity of our association which is designed to facilitate the members to study and discuss various issues in group. At the intensive study Course, one of the members acts as a group leader and leads the discussion on issues of the relevant subject / topic and one of the seniors in the profession monitors the discussion. The meetings are generally arranged ON Hybrid mode on 1st, 3rd and 5th Friday of the month during 3.30 p.m. to 6.00 p.m. There are around 15-16 meetings will be arranged for the Intensive Study Circle.

1 st The inaugural meeting of the Intensive Study Course is scheduled to be held on Friday, 15-12-2023 between 3.30 p.m. & 6.00 p.m. on hybrid mode on the subject “Issues and Intricacies in GSTR 9 / 9C along with implications on Notices by GST Department”. The topic will be lead by Group Leader CA Dharmen Shah and the Monitor of CA Mayur Parekh.

The group strength is restricted to a limited number of members to facilitate better interaction within the group. The Intensive Study Course Fee is fixed at Rs. 1,650/- including GST for Members and Rs. 1,850/- including GST for Non members. You are requested to enroll at the earliest to avoid disappointment. Kindly use photocopy of the Enrolment form printed here in below. Also write your email address and mobile number for better communication.

Member interested to act as group leader should inform by filling up the option in the Form of “I wish to be a group leader for the subject” and are requested to contact the Convener on the mobile numbers mentioned- on Cell No. 9224386682/9821441740 / 9892512345/9870008752

Note :

- The First Meeting of the ISC is proposed to be a HYBRID meeting. The members joining the ISC are requested to fill the attached form for selection of Only Physical Mode or Only Virtual Mode. The Physical mode will be continued only if majority participants opt for the Physical Mode. (Else only Virtual meetings shall be held no Hybrid Meeting shall be held)

- GST lectures will be in form of group discussion, which will be helpful to study the GST law.

- If the materials are received 3 days earlier to the date of meeting, the same will be circulated through mails to the participants.

- Participants are requested to discuss only the points related to the particular topic of the meeting and to come prepared for the subject, which will be helpful for the discussion.

| Pranav Kapadia

Chairman |

Hiral Shah

Convenor |

Sanjay Gajra

Jt.Convenor |

Sujoy Mehta

Jt.Convenor |

Bhavin Mehta

Jt.Convenor |

| 9224386682 | 9821441740 | 9892512345 | 9870008752 |

THE GOODS & SERVICES TAX PRACTITIONERS’ ASSOCIATION OF MAHARASHTRA ENROLMENT FORM FOR INTENSIVE STUDY COURSE CIRCULAR FOR THE YEAR 2023-24

To,

Convener,

Intensive Study Course

The GSTPAM, Mazgaon, Mumbai – 400 010.

Dear Sir,

Please enroll me as a participant for the Intensive Study Course for the year 2023-24. The Registration fees of Rs.1,650/- (for members) / and Rs.1,850/- (for non-members) 18% Including GST is enclosed herewith by Cash /DD / Cheque No.____________________________ dated ____________________________drawn on__________________________

Particulars of Member/Participant :

Name: ___________________________________

Educational Qualification:___________________________________

Address for Communication:___________________________________

Telephone No. Office :___________________________________ Res____________________

Email ID :__________________________ Mob. No, _______________________________

GSTPAM Membership No:_____________________________________

GSTIN (if Applicable):_____________________________________

I also wish to be a group leader for the subject of________________________________and suitable available date will be :____________________________________

I would like to attend the Meeting (Please Tick only one option)

Only Physical Mode

Only Virtual ModeThe Physical mode will be continued only if majority participants opt for the Physical Mode

Signature_________________________

Note :-

- Please issue the Cheque in favour of ”The Goods & Services Tax Practitioners’ Association of Maharashtra” (FULL NAME IS REQUIRED TO BE STATED ON THE CHEQUE AS PER RBI DIRECTION).

- For NEFT payment – Bank of India, Mazgaon- Account No. 007020100001816, IFSC – BKID0000070. Acknowledgement generated through online transaction should be emailed on [email protected] along with Enrolment Form and payment details.

- Online Payment Link: https://www.gstpam.org/online/event-registration.php

- Outstation members are requested to make payment online payment.

- The enrollment form along with payment proof should be submitted at Room No. 104, Vikrikar Bhavan, Mazgaon, Mumbai – 400010.

- Kindly carry the receipt of payment to attend the Lecture.

- The Association reserves the right to change and alter the schedule if required.

GST, MVAT & ALLIED LAW UPDATESCompiled by Adv. Pravin Shinde |

|

|

Notification under Central Tax |

||

| Notification No. | Date of Issue | Subject |

| 05/2024 -Central Tax | 31.01.2024 | Amendment in Notification No. 02/2017-CT dated 19th June, 2017 |

| 06/2024 -Central Tax | 22.02.2024 | Seeks to notify “Public Tech Platform for Frictionless Credit” as the system with which information may be shared by the common portal based on consent under sub-section (2) of Section 158A of the Central Goods and Services Tax Act, 2017. |

|

Notification / Circular Under Maharashtra Goods and Services Tax Act, 2017 (MGST) |

||

| Notification No./

Trade Circular No |

Date of Issue | Subject |

| Notification No. 52 of 2023 dated 23.11.2023. | 17.01.2024 | MGST Rules updated up to Notification No. 52 of 2023 dated 23.11.2023. |

| 01T of 2024 | 29.01.2024 | Reimbersment of SGST application on tickets of movies. |

| 01/2024-State Tax (Rate) | 29.01.2024 | Seeks to amend Notification No 1/2027 – State Tax (Rate) dated 29th June, 2017 |

| 1T of 2024 (MSTT) | 13.02.2024 | Procedure for e-hearing of appeals before the Maharashtra Sales Tax Tribunal. |

| Notification No. 03/2024- State Tax Dt.21.02.2024 | 22.02.2024 | Seeks to rescind Notification No. 30/2023-CT dated 31st July, 2023 |

| Notification No. 04/2024- State Tax Dt.21.02.2024 | 22.02.2024 | Seeks to notify special procedure to be followed by a registered person engaged in manufacturing of certain goods. |

|

Notification Under The Maharashtra Value Added Tax Act, 2002. |

||

| Notification No./

Trade Circular No |

Date of Issue | Subject |

| VAT-1523/CR-64/

Taxation-1 |

15.01.2024 | Notification regarding Refund to Diplomatic Authorities (Taipei Economic and Cultural Center) TECC |

|

Circular Under Maharashtra Goods and Services Tax Act, 2017 (MGST) |

||

| Notification No./

Trade Circular No |

Date of Issue | Subject |

| 1T of 2024 (MSTT) | 13.02.2024 | Procedure for e-Hearing of appeals before the Maharashtra State Tax Tribunal. |

Life is not a solo but a chorus. We live in relationships from cradle to grave.

– Anonymous

INCOME TAX UPDATESCompiled By By Adv. Ajay Talreja |

|

Home Loans in India: Strategies to Save on Interest & Secure Financial Well-being

Introduction:

In India, the dream of owning a home unites individuals across diverse backgrounds. To realize this aspiration, many turn to the option of home loans, a financial tool that often entails paying a considerable sum in interest over the principal amount. This financial commitment not only demands a significant portion of one’s income but can also stretch over extended periods, impacting overall financial well-being. In this article, we delve into the subtle ways in which banks may mislead borrowers on home loans, leading to increased interest payments. Furthermore, we explore effective strategies to save on home loan interest, providing a roadmap to financial security.

Real Problem: When obtaining a home loan, banks typically offer two types of interest rates: floating and fixed.

Fixed Interest Rate: In a fixed-rate loan, the interest rate is set at the time of taking the home loan. This means that regardless of future fluctuations in interest rates, your rate remains constant. However, it’s important to note that the rate quoted by the bank for a fixed-rate loan is generally 2-3% higher than a standard home loan.

Floating Interest Rate: In a floating-rate loan, the interest rate is not fixed at the time of acquiring the home loan. This implies that if home loan interest rates increase in the future, your interest rate will also rise, and vice versa.

Here’s where the issue arises, and it’s crucial to understand this through an example: Let’s say Mr. A has secured a home loan at a fixed rate of 9% for ₹ 50,00,000 over 20 years, with an EMI of ₹ 44,986. In this scenario, he will end up paying an interest amount of ₹ 57,96,711, with ₹ 4,46,200 being paid as interest in the first year alone. Now, let’s assume that the home loan interest rate increases to 9.5%, but the bank fails to inform Mr. A about this change. If he continues to pay the same EMI, the loan tenure will automatically extend from 20 years to 22 years, and the interest amount will rise from ₹ 57,96,711 to ₹ 71,30,361. This situation creates a cycle where individuals end up paying only the interest amount and struggle to repay their home loan principal. To address this concern, it is advisable to suggest to your bank that they inform customers about any changes in the home loan interest rate. This way, borrowers can adjust their EMI amounts accordingly and avoid unintentionally extending their loan tenure.

Solution: To address the challenge of home loan interest, this article proposes the following strategies: Regular Repayments:

- Regular Repayments: Implement a practice of repaying an amount equivalent to one installment to the bank every year. This approach can result in a reduction in the overall interest amount paid and concurrently lead to a decrease in the loan tenure. By consistently contributing an additional installment each year, borrowers can make meaningful strides in reducing their debt burden. Example: Mr. A takes a home loan of ₹ 50,00,000 for 20 years at 9% interest. With a regular installment of ₹ 44,986, he pays an interest of ₹ 57,96,711, exceeding the principal amount. By paying an extra installment of ₹ 44,986 annually, his interest amount reduces to ₹ 46,38,784, resulting in a significant 20% (₹ 11,57,927) reduction in interest. Additionally, his loan tenure decreases from 20 years to 16 years. Adjust the additional amount based on your capacity and evaluate the potential savings from interest.

- Investment in Mutual Funds: Explore the option of investing an amount equivalent to one EMI in mutual funds on an annual basis. Assuming a conservative return of 10-11%, this investment strategy has the potential to yield returns that surpass the amount saved in interest payments. The power of compounding is a crucial factor, emphasizing how continued investment can significantly augment returns over an extended period. Continuing the example, if Mr. A invests ₹ 44,986 annually in a mutual fund with an assumed 11% return (based on historical returns), his investment after 16 years would be ₹ 19,56,929. The return of ₹ 12,37,153 is 7% more than the amount saved in interest. Exploit the power of compounding; for instance, continuing the annual investment till 20 years would yield ₹ 32,05,934, resulting in a substantial return of ₹ 23,06,214. The accelerated growth showcases the compounding effect.

- Tax Considerations: While saving taxes on home loan interest is important, it should not lead to paying more interest. Understand that tax-saving strategies should align with wealth creation. Rather than paying excess interest for tax benefits, consider optimizing investments to generate higher returns.

- Tax Considerations: While saving taxes on home loan interest is important, it should not lead to paying more interest. Understand that tax-saving strategies should align with wealth creation. Rather than paying excess interest for tax benefits, consider optimizing investments to generate higher returns.

- Expanding on the Investment Strategy: Diving deeper into the investment strategy, it’s imperative to recognize the transformative impact of mutual fund investments on long-term financial goals. Mutual funds offer a diversified and professionally managed portfolio of stocks, bonds, and other securities. The potential for higher returns compared to traditional savings instruments makes them an attractive option for those seeking to maximize their investment gains. Moreover, the disciplined approach of investing an amount equivalent to one EMI annually ensures a systematic and structured investment pattern. This not only aids in capitalizing on market opportunities but also instills financial discipline, encouraging individuals to prioritize savings and investment amid the ebb and flow of everyday expenses.

- In Conclusion: In conclusion, whether through the implementation of regular repayments or the strategic allocation of funds into mutual funds, individuals possess the capacity to save a substantial amount that would otherwise be disbursed as interest on home loans. These approaches not only contribute to immediate financial savings but also underscore the significance of informed financial planning in achieving long-term goals. As individuals navigate the intricate landscape of home loans, it is crucial to remain vigilant and proactive in managing their financial commitments. By understanding the nuances of interest rate structures, exploring strategic investment avenues, and embracing disciplined financial practices, borrowers can not only mitigate the burden of home loan interest but also pave the way for a more secure and prosperous financial future.

Property Allotment Date is acquisition date for Capital Gain Computation: ITAT Mumbai

D. K. Brothers Vs ITO (ITAT Mumbai)

Introduction: In a significant ruling, the Income Tax Appellate Tribunal (ITAT) Mumbai, in the case of D.K. Brothers vs. ITO, has set aside the order passed by the National Faceless Appeal Centre (NFAC) regarding the assessment year 2011-12. The dispute revolves around the computation of capital gains, with the key contention being the date of acquisition. This article delves into the details of the case and the implications of the ITAT Mumbai order. Detailed Analysis: The appellant, M/s. D.K. Brothers, challenged the assessment order passed by the Assessing Officer (AO), who determined the total income at Rs. 45,49,200 under short- term capital gains. The AO considered the date of registration of the property on 15.09.2010 as the acquisition date, contrary to the appellant’s claim of using the property allotment date, 28.01.1992, for computing long- term capital loss.

The dispute centers around the correct date of acquisition for capital gain calculation. The AO’s decision was upheld by the Commissioner of Income Tax (Appeals) [CIT(A)], leading the appellant to appeal to the ITAT Mumbai. The ITAT Mumbai, after considering the facts and legal aspects, concluded that the date of property allotment, 28.01.1992, should be considered as the acquisition date for computing capital gains. This decision is in line with established principles and precedents, emphasizing the importance of the allotment date in such cases. Conclusion: The ITAT Mumbai’s order in the case of D.K. Brothers vs. ITO clarifiesthe determination of the acquisition date for capital gain computation. By setting aside the earlier decision and deleting the addition made by the AO, the ITAT reaffirms the significance of the property allotment date in such scenarios. This ruling carries implications for similar cases and reinforces the adherence to established principles in computing capital gains.

Assessment Order Without DIN/DN Quashed by ITAT Delhi

Smt. Sharda Devi Bajaj Vs DCIT (ITAT Delhi)

Introduction: Delve into the recent ITAT Delhi ruling in the case of Smt. Sharda Devi Bajaj vs. DCIT, where the assessment order faced scrutiny for lacking the Document Identification Number (DIN/DN). The article unfolds the intricacies of the case, highlighting the importance of compliance with the CBDT Circular No. 19 / 2019 dated 14 . 08 . 2019 and i t s impact on the validity of the assessment order.

A search operation in the Bajaj Group led to the assessment of income for various assessees. The challenge arose concerning the absence of Document Identification Number (DIN/DN) in the assessment order. CBDT Circular and Legal Mandate: CBDT Circular No. 19/2019 dated 14.08.2019 mandates the generation and quoting of DIN in communications and orders. Exceptions for manual issuance are permitted under specific circumstances, with recorded reasons and prior approval. Assessment Order Deficiency: The assessment order, in this case, lacked the essential DIN, raising concerns about its validity. CBDT Circular explicitly deems communications without DIN as invalid.

Legal Precedents: Citing legal precedents, the article underscores that subsequent generation of DIN does not suffice. Recent decisions by Hon’ble Courts emphasize strict adherence to DIN requirements.

Communication dated 17.9.2019: The Revenue relies on a communication about the roll-out of the facility for System-generated Document (Intimation Letter) containing DIN. However, it is clarified that this communication pertains to exceptional circumstances under Circular Para 3 and does not apply in this case. ITAT Ruling and Additional Ground: The ITAT allows the introduction of an additional ground based on the CBDT Circular, emphasizing its foundation in existing facts. The ruling aligns with the principles upheld by various coordinate Benches and jurisdictional High Courts.

Conclusion of ITAT Ruling:

The ITAT ruling sets aside the assessment orders, considering the absence of DIN/DN as a fatal flaw. The decision reiterates the significance of compliance with CBDT Circular No. 19/2019 dated 14.08.2019 for the validity of assessment orders. Conclusion: The ITAT Delhi’s recent ruling in Smt. Sharda Devi Bajaj vs. DCIT serves as a noteworthy reminder of the criticality of adhering to procedural mandates, particularly the CBDT Circular No. 19/2019 dated 14.08.2019. The absence of Document Identification Number (DIN/DN) in the assessment order proved detrimental, leading to the quashing of the order. This case underscores the courts’ commitment to upholding procedural integrity and reinforcing the legal consequences of non-compliance with essential requirements, ensuring a fair and just taxation system.

Granting Condonation for Appeal Delay: Consider Senior Citizens Unfamiliar with Digital Systems & Faceless Scheme

Marate Venkateshkumar Vs ITO (ITAT Bangalore)

Condonation of delay in filing of appeal by Senior Citizen assessee should be allowed if he was unfamiliar with digital systems and faceless scheme

Conclusion: Assessee had shown sufficient cause for the delay in filing the appeals before the Tribunal as he was old and not well acquainted and conversant with the digital system in order to follow up with the income tax notices, which were posted in IT portal. Accordingly, the delay in filing appeal was condoned. Held: Assessee had deposited a sum of Rs.27,87,500/- into his bank account during demonetization period. Same had been considered as income u/s 69A. Against this assessee went in appeal before NFAC, who had confirmed it. Against this, assessee was once again in appeal. There was a delay of 424 days in filing the appeal before this Tribunal. Assessee had explained that assessee was of 74 years old and not well acquainted and conversant with the digital system in order to follow up with the income tax notices, which were posted in IT portal. Assessee was not aware about any faceless scheme of assessment followed by the department. Assessee had not seen the NFAC’s order in its portal and the same had been came to knowledge of assessee when it received a message about penalty notice issued u/s 270A & 270AAC directing him to file reply in response to the notice issued. Consequent to this, assessee consulted his advocate and taken steps to file the appeal before this Tribunal. Thus, it caused 424 days delay in filing the appeal before the Tribunal and prayed to condone the delay. Department strongly opposed the admission of appeal and submitted that assessee was habitual in filing appeal belatedly as the appeal before NFAC also filed belatedly. Hence, no liberal view to be taken on this case and appeals should not be admitted for adjudication. It was held that the courts were empowered to condone the delay, provided the litigant was able to demonstrate that there was “sufficient cause” in preferring appeal beyond the limitation period. The Courts had also held that the expression “sufficient cause” should receive liberal construction so as to advance substantial justice. Hence, the question of condonation of delay was a factual matter and the result would depend upon the facts of the case and the cause shown by the assessee for the delay. It had also been opined that generally delays in preferring appeals were required to be condoned in the interest of justice, where no gross negligence or deliberate inaction or lack of bona fides was imputable to the party seeking condonation of the delay. Therefore, assessee had shown sufficient cause for the delay in filing the appeals before the Tribunal. Accordingly, the delay in filing appeal was condoned.

DCIT Vs Vimal Kanubhai Patel (ITAT Ahmedabad)

Introduction: In the recent case of DCIT vs. Vimal Kanubhai Patel, the Income Tax Appellate Tribunal (ITAT) in Ahmedabad addressed a significant dispute concerning the addition of INR 3,45,90,531/- on account of unexplained credits in the Citibank NA Singapore account for the Assessment Year 2004-05. The Revenue, dissatisfied with the order of the Commissioner of Income-tax (Appeals) [CIT(A)], appealed against the decision.

Background:

Vimal Kanubhai Patel, an individual and non-resident for the relevant assessment year, was a director in various companies, including Banco Product (India) Ltd. The investigation revealed undisclosed foreign assets, including bank accounts, investments, and properties. Patel admitted to non-disclosure before the investigation team and expressed the intention to determine taxable income related to these undisclosed foreign assets.

one of the undisclosed foreign bank accounts was with Citibank NA Singapore, jointly held with Patel’s brothers. The dispute primarily revolved around the credit entry in the Citibank NA Singapore USD account, amounting to US $7,87,939.73 during the assessment year 2004-05.

Revenue’s Grounds of Appeal: The Revenue raised two key grounds of appeal: The CIT(A) erred in deleting the addition of INR 3,45,90,531/- on account of unexplained credits in the Citibank NA Singapore account The assessee failed toprove that the deposits in the undisclosed foreign bank account were income accrued outside India.

Assessee’s Defense: Patel contended that he was a non-resident during the assessment year and, as per Section 5(2) of the Income-tax Act, only income received or deemed to be received, or accruing or arising or deemed to accrue or arise in India is taxable. The undisclosed foreign bank account’s deposits were linked to his family’s business in Tanzania, with no connection to income in India.

CIT(A)’s Decision: The CIT(A) emphasized Patel’s non-resident status for the assessment year and highlighted the onus on the Revenue to establish that the deposits in the foreign account were linked to income falling under Section 5(2) of the Act. The CIT(A) concluded that since the deposits had no connection with income falling under Section 5(2), the addition of INR 3,45,90,531/- was unjustified and deleted the same. ITAT’s Verdict: The ITAT upheld the CIT(A)’s decision, emphasizing that the Revenue failed to provide evidence linking the deposits to income accrued or arising in India. It was noted that Patel, being a non-resident, was only liable to pay tax on income with an Indian connection. The absence of findings by the AO regarding the deposits’ connection to Indian income led to the dismissal of the Revenue’s appeal. Conclusion: The DCIT vs. Vimal Kanubhai Patel case underscores the importance of establishing a clear connection between foreign bank account deposits and income taxable in India, especially when dealing with non-resident individuals. The onus is on the Revenue to provide corroborative evidence to support the addition of unexplained credits. The verdict reaffirms the principle that a non-resident cannot be taxed in India unless income is proven to accrue or arise within the country’s jurisdiction.

Everything in life is a test of character.

– John Blanchard

QRMP SCHEME

An introduction:

As a trade facilitation measure and in order to further ease the process of doing business, the GST Council in its 42nd meeting held on 05th October, 2020 had recommended that registered persons having Aggregate Annual Turnover up to Rs. 5 Cr may be allowed to furnish return on quarterly basis along with monthly payment of tax, with effect from 01.01.2021. This scheme of quarterly return filing along with monthly payment of taxes is referred to as “QRMP Scheme”.

Eligibility for the Scheme:

In terms of Notification No. 84/2020- Central Tax, dated 10.11.2020, a registered person who is required to furnish a return in FORM GSTR-3B, and who has an Aggregate Annual Turnover of up to Rs. 5 Cr in the preceding financial year, is eligible for the QRMP Scheme.

The Aggregate Annual Turnover for the preceding financial year shall be calculated on the common portal taking into account the details furnished in the returns by the taxpayer for the tax periods in the preceding financial year. In case the Aggregate Annual Turnover exceeds Rs. 5 Cr during any quarter in the current financial year, the registered person shall not be eligible for the Scheme from the next quarter.

Eligibility for the Scheme:

- Facility to avail the Scheme on the common portal is available throughout the year.

- In terms of Rule 61A of the CGST Rules, a registered person can opt in for any quarter from the first day of the second month of preceding quarter to the last day of the first month of the quarter. In order to exercise this option, the registered person must have furnished the last return, as due on the date of exercising such option.For example: A registered person intending to avail the Scheme for the quarter ‘July to September’ can exercise his option during 1st of May to 31st of July. If he is exercising his option on 27th July for the quarter (July to September), in such case, he must have furnished the return for the month of June which was due on 22nd/24th July.

- Similarly, the facility for opting out of the Scheme for a quarter will be available from first day of second month of preceding quarter to the last day of the first month of the quarter.

- Registered persons are not required to exercise the option every quarter. Where such option has been exercised once, they shall continue to furnish the return as per the selected option for future tax periods, unless they revise the said option.

- All persons who have obtained registration during any quarter or the registered persons opting out from paying tax under Section 10 of the CGST Act during any quarter shall be able to opt for the Scheme for the quarter for which the opting facility is available on the date of exercising option.

- Such registered person, whose Aggregate Annual Turnover crosses Rs. 5 Cr during a quarter in current financial year, shall opt for furnishing of return on a monthly basis, electronically, on the common portal, from the succeeding quarter. In other words, in case the Aggregate Annual Turnover exceeds Rs. 5 Cr during any quarter in the current financial year, the registered person shall not be eligible for the Scheme from the next quarter.

- The option to avail the QRMP Scheme is GSTIN wise and therefore, distinct persons as defined in Section 25 of the CGST Act (different GSTINs on same PAN) have the option to avail the QRMP Scheme for one or more GSTINs. In other words, some GSTINs for that PAN can opt for the QRMP Scheme and remaining GSTINs may not opt for the Scheme.

Furnishing of details of outward supplies under Section 37 of the CGST Act:

- The registered person opting for the Scheme would be required to furnish the details of outward supply in FORM GSTR-1 quarterly as per the Rule 59 of the CGST Rules.

- For each of the first and second months of a quarter, such a registered person will have the facility (Invoice Furnishing Facility- IFF) to furnish the details of such outward supplies to a registered person, as he may consider necessary, between the 1st day of the succeeding month till the 13th day of the succeeding month. The said details of outward supplies shall, however, not exceed the value of ` 50 Lakh in each month. It may be noted that after 13th of the month, this facility for furnishing IFF for previous month would not be available. As a facilitation measure, continuous upload of invoices has also been provided for the registered persons wherein they can save the invoices in IFF from the 1st day of the month till 13th day of the succeeding month. The facility of furnishing details of invoices in IFF has been provided so as to allow details of such supplies to be duly reflected in the FORM GSTR-2A and FORM GSTR-2B of the concerned recipient. For example, a registered person who has availed the Scheme wants to declare two invoices out of the total ten invoices issued in the first month of quarter since the recipient of supplies covered by those two invoices desires to avail ITC in that month itself. Details of these two invoices may be furnished using IFF. The details of the remaining 8 invoices shall be furnished in FORM GSTR-1 of the said quarter. The two invoices furnished in IFF shall be reflected in FORM GSTR-2B of the concerned recipient of the first month of the quarter and remaining eight invoices furnished in FORM GSTR-1 shall be reflected in FORM GSTR- 2B of the concerned recipient of the last month of the quarter. The said facility would however be available, say for the month of July, from 1st August till 13th August. Similarly, for the month of August, the said facility will be available from 1st September till 13th September.

- It is re-iterated that the IFF is not mandatory and is only an optional facility made available to the registered persons under the QRMP Scheme.

- The details of invoices furnished using the IFF in the first two months are not required to be furnished again in FORM GSTR-1 Accordingly, the details of outward supplies made by such a registered person during a quarter shall consist of details of invoices furnished using IFF for each of the first two months and the details of invoices furnished in FORM GSTR-1 for the quarter. At his option, a registered person may choose to furnish the details of outward supplies made during a quarter in FORM GSTR-1 only, without using the IFF.

Monthly Payment of Tax:

- The registered person under the QRMP Scheme would be required to pay the tax due in each of the first two months of the quarter by depositing the due amount in FORM GST PMT-06, by the twenty-fifth day of the month succeeding such month. While generating the challan, taxpayers should select “Monthly payment for quarterly taxpayer” as reason for generating the challan. The said person can use any of the following two options provided below for monthly payment of tax during the first two months –Fixed Sum Method: A facility has been made available on the portal for generating a pre-filled challan in FORM GST PMT-06 for an amount equal to thirty-five per cent of the tax paid in cash in the preceding quarter where the return was furnished quarterly; or equal to the tax paid in cash in the last month of the immediately preceding quarter where the return was furnished monthly.Monthly tax payment through this method would not be available to those registered persons who have not furnished the return for a complete tax period preceding such month. A complete tax period means a tax period in which the person is registered from the first day of the tax period till the last day of the tax period.

Self-Assessment Method: The said person, in any case, can pay the tax due by considering the tax liability on inward and outward supplies and the input tax credit available, in FORM GST PMT-06. In order to fa cilitate ascertainment of the ITC available for the month, an auto-drafted input tax credit statement has been made available in FORM GSTR-2B, for every month. - The said registered person is free to avail either of the two tax payment method above in any of the two months of the quarter.

- In case the balance in the electronic cash ledger and/or electronic credit ledger is adequate for the tax due for the first month of the quarter or where there is nil tax liability, the registered person may not deposit any amount for the said month. Similarly, for the second month of the quarter, in case the balance in the electronic cash ledger and/or electronic credit ledger is adequate for the cumulative tax due for the first and the second month of the quarter or where there is nil tax liability, the registered person may not deposit any amount.

- Any claim of refund in respect of the amount deposited for the first two months of a quarter for payment of tax shall be permitted only after the return in FORM GSTR-3B for the said quarter has been furnished. Further, this deposit cannot be used by the taxpayer for any other purpose till the filing of return for the quarter.

Quarterly filing of FORM GSTR-3B:

Such registered persons would be required to furnish FORM GSTR-3B, for each quarter, on or before 22nd or 24th day of the month succeeding such quarter. In FORM GSTR-3B, they shall declare the supplies made during the quarter, ITC availed during the quarter and all other details required to be furnished therein. The amount deposited by the registered person in the first two months shall be debited solely for the purposes of offsetting the liability furnished in that quarter’s FORM GSTR-3B. However, any amount left after filing of that quarter’s FORM GSTR- 3B may either be claimed as refund or may be used for any other purpose in subsequent quarters. In case of cancellation of registration of such person during any of the first two months of the quarter, he is still required to furnish return in FORM GSTR-3B for the relevant tax period.

Applicability of Interest:

- For registered person making payment of tax by opting Fixed Sum Method:No interest would be payable in case the tax due is paid in the first two months of the quarter by way of depositing auto-calculated fixed sum by the due date. In other words, if while furnishing return in FORM GSTR-3B, it is found that in any or both of the first two months of the quarter, the tax liability net of available credit on the supplies made / received was higher than the amount paid in challan, then, no interest would be charged provided they deposit system calculated amount for each of the first two months and discharge their entire liability for the quarter in the FORM GSTR-3B of the quarter by the due date.In case such payment of tax by depositing the system calculated amount in FORM GST PMT-06 is not done by due date, interest would be payable at the applicable rate, from the due date of furnishing FORM GST PMT-06 till the date of making such payment.Further, in case FORM GSTR-3B for the quarter is furnished beyond the due date, interest would be payable as per the provisions of Section 50 of the CGST Act on the tax liability net of ITC.

- For registered person making payment of tax by opting Self- Assessment Method: Interest amount would be payable as per the provision of Section 50 of the CGST Act for tax or any part thereof (net of ITC) which remains unpaid / paid beyond the due date for the first two months of the quarter.

- Interest payable, if any, shall be paid through FORM GSTR-3B.

Applicability of Late Fee:

Late fee is applicable for delay in furnishing of return / details of outward supply as per the provision of Section 47 of the CGST Act. As per the Scheme, the requirement to furnish the return under the proviso to sub-section (1) of Section 39 of the CGST Act is quarterly. Accordingly, late fee would be the applicable for delay in furnishing of the said quarterly return / details of outward supply. It is clarified that no late fee is applicable for delay in payment of tax in first two months of the quarter.

Note: Circular No. 143/13/2020-GST along with Notifications No. 81/2020-CT, 82/2020-CT, 84/2020-CT and 85/2020-CT all dated 10.11.2020 may be referred for more details on the QRMP Scheme.

Death is not the greatest loss in life. The greatest loss is what dies inside us while we live.

– Norman Cousins

GST COMPLIANCES BEFORE THE END OF FINANCIAL

|

|

As we draw an end to the financial year 2023-24, here is a list of action points to be considered for the year 2023- 24 and the upcoming financial year 2024-25 from the perspective of compliances under GST Laws. These key matters will help in smooth transition to the next financial year 2024-25

| Sr. No. | Particulars | Form No. | Due Date |

|

Registrations and Opt-In / Opt-Out for FY 2024-25 |

|||

| 1 | File Letter of Undertaking for FY 2024-25 for export of goods and/or services without payment of IGST | RFD-11 | 31-Mar-2024 |

| 2 | Opt-In for Composition Scheme for eligible dealers | CMP-02 | 31-Mar-2024 |

| 3 | Reversal of ITC on transition from Regular to Composition Scheme. | ITC-03 | 30 -May-2024 |

| 4 | Opt-In or Opt-Out of QRMP – Quarterly Return and Monthly Payment Scheme for eligible dealers having aggregate turnover below Rs. 5 crores. | GSTN Portal | 30-April-2024 |

| 5 | Register for e-invoicing if aggregate turnover exceeds Rs. 5 crores in FY 2023-24 | E-Invoice portal | 01-April-2024 |

| 6 | Options for Goods and Transport Agency – GTA

Opting from RCM to FCM for FY 2024-25 Opting from FCM to RCM for FY 2024-25 |

Annexure V

Annexure VI |

31 March – 2024

31-March-2024 |

|

Outward Supplies |

|||

| 7 | Reconcile revenue from operations, other income and asle of fixed assets as per books of account and GSTR-1 and GSTR-3B | ||

| 8 | Reconcile Debit Notes and Credit Notes as per books of account and GSTR-1 and GSTR-3B | ||

| 9 | In case of exempt supplies ensure bill of supply has been issued and reported in GSTR-1 and GSTR-3B | ||

| 10 | In case of supplies between related parties ensure valuation rules have been followed. Sec 15 and Rule 28. | ||

| 11 | Reconcile invoices / credit notes and debit notes as per books with e-invoices portal to ensure IRN is generated for all B2B, Exports and SEZ supplies.

The non-generation of e-invoice will render the tax invoice invalid, resulting in possible loss of ITC to the purchaser. |

||

| 12 | Reconcile Tax Invoice data with E-way Bill data to identify discrepancies, if any | ||

| 13 | In case of exports of goods reconcile the shipping bill details with GSTR-1. This is necessary for the claim of refund on exports. | ||

| 14 | In case of supply of services, reconciliation of advances received and adjusted as per books with details disclosed in GSTR-1 to ensure applicable tax has been discharged / adjusted in respect of same. | ||

| 15 | Calculate the aggregate turnover of the Company as per GST law and reconcile the same with aggregate turnover generated by system on GSTN portal to ensure accuracy. | ||

| 16 | Take cognizance of the aggregate turnover for various other GST provisions such as applicability of e-invoice provisions, Composition Scheme, QRMP scheme, number of HSN / SAC codes applicability etc. | ||

|

Inward Supplies |

|||

| 17 | Reconcile ITC as per books of account, GSTR-2B and ITC claimed in GSTR-3B. For differences, if any, appropriate action shall be taken. | ||

| 18 | Communicate the vendors for supplies not reflecting in the GSTR-2B. ITC in respect of such invoices is not allowed. | ||

| 19 | In case of exempt or Non – GST supplies during the year ensure reversal of ITC, if any, is calculated as per Rule 42 and Rule 43 of CGST Rules at the end of the year. Excess ITC claimed / reversed can be adjusted in the March 2024 returns. | ||

| 20 | Verification of creditors aging report to identify invoices wherein payment is due for more than 180 days and ITC claimed in respect of supplies from such vendors shall be reversed in Table 4B of GSTR-3B. | ||

| 21 | To identify the ineligible ITC recorded in books and ensure same is expenses off or capitalised (as the case maybe). If such ineligible ITC has been availed and utilized, same shall be reversed along with interest @ 18%.

Further, it must be ensured that all ineligible ITC is correctly declared in Table 4B(1) of GSTR- 3B.. |

||

| 22 | Ensure compliance with Circular No. 170/02/2022 dated 6th July, 2022 for compliance of proper disclosure of ITC on Inter-state supplies in GSTR-3B. The exercise for the whole year can be undertaken in the GSTR-3B returns of March 2024.. | ||

|

Reverse Charge Mechanism Supplies |

|||

| 23 | Identify all expenses subject to RCM (director sitting fee and legal expenses etc.) and reconcile the same with RCM liability discharged in GSTR-3B.

The differential liability if any shall be discharged along with interest as per time of supply provisions |

||

| 24 | Reconcile the foreign expenditure as per financials with import details disclosed in the GST returns. | ||

| 25 | ITC availed in respect of RCM transactions shall be equal to or less than GST liability discharged under RCM.

Where the ITC is disallowed in respect of the RCM discharged by the taxpayer, such ITC shall be disclosed in Table 4B(1) of GSTR-3B |

||

|

Additional Points |

|||

| 26 | Reconcile the closing balance of ITC in financials with balance in electronic credit ledger on the GSTN portal. | ||

| 27 | Review the list of HSN / SAC codes used during the financial year and make necessary corrections required, if any. | ||

| 28 | Adopt new document series unique for FY 2024-25 preferably separate series for each GST registration to ensure easy identification and verification. | ||

| 29 | To ensure that place of supply provision have been complied with in respect of supplies undertaken by Company. | ||

| 30 | Identify the common expenses incurred for related or distinct persons on which ITC has been availed by the taxpayer. The taxpayer needs to cross-charge such expenses to the respective entities / GSTIN of the same entity on the basis of turnover or such other reasonable method of allocation. | ||

| 31 | In case of exports ensure that export proceeds are realized within the time limit specified by the Foreign Exchange Management Act, 1999 | ||

Make sure the thing you are living for is worth dying for.

– Charles Mayes

IMPORTANCE OF PASSIVE INCOMECompiled By By Mr. Tushar P. Joshi |

|

In continuation of the thoughts which I had expressed in the last edition, as regards family savings and Retirement Planning, I would like to continue with the same in the present issue.

Before you finalize a certain savings plan on recommendations of an investment advisor, you need to answer a few questions to yourself. First decide about HOW much money you require? WHEN would you require the money? And for WHAT purpose? Once these questions are answered see if that plan serves or provides solutions to all or majority of your questions. You need to take help of an expert while undertaking the above exercise. I strongly recommend you to have a financial planner to help you, even if it means taking his services at a cost. Don’t think the cost as an expense, but think of the benefits that would accrue to you and the peace of mind you may have thereafter.

The famous poet Robert Louis had stated “There is only one difference between a long life and a good dinner; In the dinner, the sweets come last”. This quote can be easily rephrased as, in a good dinner, the sweets come last, in life it is JEEVAN SHANTI and JEEVAN AKSHAY which are lifelong pension plan from Life Insurance Corporation of India.

The best thing about Jeevan Shanti and Jeevan Akshay is that you can savor it as long as you live. Both are pension plans accompanying with wishes for a happy, long life as the plan covers LONGEVITY RISK. If we look at the global scenario, we find that the economically advanced nations have a lower rate of interest, while the developing nations have a higher rate of interest.

On a second thought, going by the popular opinion that India is likely to join the league of super powers in future and taking a look at the current interest rate scenario, we can definitely expect a lowering of the interest rates. Economic scene and government policies are likely to change but our financial obligations and requirements shall remain the same. They may increase but never reduce.

In life it pays to have at least one source of steady income. Both the above plans seek to achieve that, it supplements your income in life. We cannot add years to our life nor to increase the life of our loved ones but we can certainly add life to the years, ours and theirs.

Jeevan Akshay & Jeevan Shanti comes with wishes, that you celebrate many anniversaries and many more birthdays with good health care.

Wishing you a happy peaceful long life ahead.

The quality of life is more important than life itself.

– Alexis Carell

What makes life dreary is absence of motive. What makes life complicated is multiplicity of motive. What makes life victorious is singleness of motive.

– George Eliot

”Wishing our members a very HAPPY BIRTHDAY!!”

| Members Name | Date of Birth |

| Gupta Rajesh J. | 11 – March |

| Channa Vyankatesh Vithal | 11 – March |

| Khan Simran Tahir | 11 – March |

| Mahidhariya Vaibhav Mukesh | 11 – March |

| Dongare Uday Vishnu | 12 – March |

| Roman Sanjay Ashok | 12 – March |

| Choudhary Dinesh Motiram | 12 – March |

| Bhosale Ashish Chandrashekhar | 12 – March |

| Doshi Ronak Balwantrai | 12 – March |

| Hasmani Altaf A. Raheman | 12 – March |

| Chouhan Raghunath Singh | 13 – March |

| Chokhani Rajendra S | 13 – March |

| Deshmukh Nalinee Sandeep | 13 – March |

| Jha Mukesh U | 13 – March |

| Tiwari Dinesh Kumar Ramapati | 13 – March |

| Bakal Anup Ashok | 13 – March |

| Maity Vikas Milan | 13 – March |

| Panchal Bharat Bhogilal | 14 – March |

| Bora Mohammad Arif | 14 – March |

| Gurav Santosh V | 14 – March |

| Zahoor Hakim | 14 – March |

| Shenoy Rajesh Vasant | 15 – March |

| Gabajiwala Huzefa Asgar | 15 – March |

| Kotecha Niraj Dinesh | 15 – March |

| Dhuri Vivek Raghoba | 15 – March |

| Khakhu Mehak Hamid | 15 – March |

| Rai Balkrishna Kanthappa | 16 – March |

| Shetty Rajesh Krishna | 16 – March |

| Karlakar Charushila Ramesh | 16 – March |

| Gadia Mahendra Chandulal | 17 – March |

| Gami Rupa Nimish | 17 – March |

| Sivaswamy N.S. | 17 – March |

| Patel Premal S. | 17 – March |

| Gholap Romesh Jeevan | 17 – March |

| Singh Omprakash A. | 17 – March |

| Lodha Chetan P | 17 – March |

| Galgale Shripad Prabhakar | 19 – March |

| Dharangaonkar Shekhar Madhukarrao | 19 – March |

| Baraskar Swati Jagannath | 19 – March |

| Shah Atul Amrutlal | 20 – March |

| Visaria Chetan Dhanjibhai | 20 – March |

| Darji Jayesh J. | 20 – March |

| Nandedkar Pushkaraj Prashant | 20 – March |

| Surti Navroz Abdulhusain | 21 – March |

| Jadhav Sanjay Kashiram | 21 – March |

| Chhatbar Chetan Pranlal | 22 – March |

| Nadar Deventhiran Arumuganainar | 22 – March |

| Shetty Prasad Dayanand | 22 – March |

| Shah Hiten Shanmukhlal | 23 – March |

| Upadhyay Hitendra Rajendra | 23 – March |

| Prajapati Narendra Thakorbhai | 23 – March |

| Jain Dinesh Kumar | 23 – March |

| Yeolekar Prashant Somnath | 23 – March |

| Goyal Suresh J. | 23 – March |

| Arote Ramesh Manohar | 23 – March |

| Dharamshi Hitesh M. | 23 – March |

| Gangwani Vidhi Girish | 23 – March |

| Dedhia Keyur Shantilal | 23 – March |

| Lale Sudhir Gopal | 24 – March |

| Zaki Hamza Tasadduqe Husain | 24 – March |

| Bhende Mangesh Sushilkumar | 24 – March |

| Salunke Sandeep Bapu | 24 – March |

| Shinde Praful Sukhdev | 24 – March |

| Chinchalikar Varun Vyankatesh | 24 – March |

| Chheda Sneha Harakchand | 24 – March |

| Tayade Shaligram Manikrao | 25 – March |

| Pawar Sachin Vilas | 25 – March |

| Khairnar Tushar D. | 25 – March |

| Thakur Ajit Ratnakant | 26 – March |

| Hirekerur Dinesh S. | 26 – March |

| Potdar Nandkumar Sheshanath | 26 – March |

| Shaikh Shafiahmed R | 27 – March |

| Gandhi Maulik H | 27 – March |

| Shah Yash Shailesh | 27 – March |

| Haria Rohan Dhiraj | 28 – March |

| Kurade Abhishek Gundu | 28 – March |

| Patil Prajakta Ganesh | 28 – March |

| Bora Navneetlal A. | 29 – March |

| Havale Siddharth Suhas | 29 – March |

| Kimbahune Prasad R | 30 – March |

| Mahajan Ram Sanjay | 30 – March |

| Nadkarni Harshal Subhash | 30 – March |

| Turakhia Viday Kunal | 30 – March |

| Nagbhidkar Shashikant Yadaorao | 31 – March |

| Kanadje Motiram Manikrao | 31 – March |

| Sabnis Nitin Mohan | 31 – March |

| Shah Priyam Rameshbhai | 31 – March |

| Aditya Seema Pradeep | 31 – March |

| Patani Vishal Ramesh | 31 – March |

| Jhavar Mishrilal Nandalal | 01 – April |

| Dhadd S. B | 01 – April |

| Bafna Hirachand Nemichand | 01 – April |

| Poojary Sadashiv Chandaya | 01 – April |

| Desai Jitesh Jayantilal | 01 – April |

| Patel Shantilal Nanjibhai | 01 – April |

| Savala Nayana Premji | 01 – April |

| Sharma B. M. | 01 – April |

| Vishwakarma Brijbhushan Parasnath | 01 – April |

| Zirange Pandurang Hari | 01 – April |

| Gadhave Nilesh Dattatraya | 01 – April |

| Tahasildar Mohamedkhalil Shamshoddin | 01 – April |

| Jain Jinendra Surajmal | 02 – April |

| Padia Shyam Sundar | 02 – April |

| Malekar Prakash Parashram | 02 – April |

| Velankar Prasad Damodar | 02 – April |

| Patil Chirag Ravindra | 02 – April |

| Vora Kush Subodh | 02 – April |

| Deshingkar M. K. | 03 – April |

| Esaf Dilawar Abubakkar | 03 – April |

| Ratate Pradip Yashwant | 03 – April |

| Shah Tejas Jitendra | 03 – April |

| Sharma Banshidhar | 04 – April |

| Kadam Jankiram Sanjaypan | 04 – April |

| Shivnani Krisha Ashwin | 04 – April |

| Basantani Choitharam C. | 04 – April |

| Dhada J. V | 05 – April |

| Bhutta Yogesh T. | 05 – April |

| Jaroli Komalsingh Madanlal | 05 – April |

| Sharma Suresh Ramashankar | 05 – April |

| Chauhan Jaiprakash R. | 05 – April |

| Tayade Nagesh Shankar | 05 – April |

| Borhade Ambadas Bhima | 05 – April |

| Gandhi Mayank M. | 06 – April |

| Kamat Shrikant S. | 06 – April |

| Ambawat Purnima Nilesh | 06 – April |

| Wandrekar Amod Arun | 06 – April |

| Uttekar Vaibhav Shantaram | 06 – April |

| Bhuta Nitin Sureshchandra | 07 – April |

| Maharugade Sanjay Keshav | 07 – April |

| Sharma Umashankar Rampramod | 07 – April |

| Toshniwal Atul Mukundlal | 07 – April |

| Bhokare Pramod Ankush | 07 – April |

| Dangat Umesh Vasantrao | 08 – April |

| Warty Gauresh D | 08 – April |

| Shah Viral Girish | 08 – April |

| Jain Ketan Nagraj | 08 – April |

| Jambhekar Vinayak Pramod | 08 – April |

| Lalwani Vidhi Avinash | 08- April |

| Patel Vinubhai Narshibhai | 09- April |

| Modi Tushar I. | 09- April |

| Hasabnis Kedar Prasad | 09- April |

| Jaiswal Shivkijmar Ramsarikh | 10- April |

| Modi Manoj Vijay | 10- April |

Life is not measured by length but by depth. Birthdays tell us how long we have been on the road, not how far we have travelled.

– Vance Havner

OUR PUBLICATIONS AVAILABLE FOR SALE

| Sr. No. | Name | Price ₹ |

| 1 | FMCG & Pharmaceutical Industry – GST Issues & Challenges | 150/- |

| 2 | Transitional Provision | 50/- |

| 3 | 46th RRC Book | 175/- |

| 4 | Referencer 2022-23 | 375/- |

| 5 | Referencer 2023-24 | 750/- |

| 6 | Mega Full Day Seminar Booklet 2.7.2022 | 130/- |

| 7 | Half Day Seminar Booklet 17.11.2022 | 100/- |

| 8 | Maharashtra Goods & Service Tax Act along with Rules (MGST Bare Act) | 850/- |

| 9 | Short Publication GST practical guides (5 Book Series) | 555/- |

| 10 | 47th RRC Book | 250/- |

| 11 | Charitable Trusts | 300/- |

| 12 | Mega Full Day Seminar Booklet 09.02.2024 | 150/- |

| 13 | 48th RRC Book | 250/- |

Payment Link for Publication on sales : https://www.gstpam.org/online/purchase-publication.php

GSTPAM News Bulletin Committee for Year 2023-24

Pradip Kapadia Chairman |

Aloke R. Singh Convenor |

Ashish Ruparelia Jt. Convenor |